1 Q09 Earnings Eng Final[20090421134102809]

- 1. 2009 1Q Earnings Release April 21st 2009

- 2. All information regarding management performance and financial results of LG Electronics (the “Company”) during the 1st quarter of 2009 as contained herein has been prepared on a parent and consolidated basis in accordance with Korean Generally Accepted Accounting Principles (Korean GAAP). In addition, the information contained herein has been prepared in advance, prior to being reviewed by outside auditors, solely for the convenience of investors of the Company, and is subject to change in the process of final reviewing by outside auditors. The information contained herein includes forward-looking statements in respect to future plans, prospects, and performances of the Company as well as the Company’s projected sales plan for the 2nd quarter of 2009. These forward-looking statements also refer to the Company’s performance on both parent and consolidated base, as indicated. The aforementioned forward-looking statements are influenced by changes in the management environment and relative events, and by their nature, these statements refer to uncertain circumstances. Consequently, due to these uncertainties, the Company’s actual future results may differ materially from those expressed or implied by such statements. Please note that as the forward-looking statements contained herein are based on the current market situation and the Company’s management direction, they are subject to change according to the changes in future market environment and business strategy. The information contained herein should not be utilized for any legal purposes in regards to investors’ investment results. The Company hereby expressly disclaims any and all liability for any loss or damage resulting from the investors’ reliance on the information contained herein.

- 3. Table of Contents Ⅰ. ’09 1Q Results (Consolidated) Ⅱ. Performance and Outlook by Sector Ⅲ. ’09 1Q Results (Parent) Ⅳ. ’09 2Q Business Direction and Prospects

- 4. Ⅰ. 2009 1Q Results (Consolidated) Sales and Profit Consolidated Sales & Profits (Unit : KRW tn) Sales QoQ YoY OP(%) QoQ YoY Total 0.12 +0.25 - 1.40 15.89 - 7.5% +10.7% (Consolidated) (0.7%) 1.5%p 9.8%p 0.46 +0.35 - 0.15 LGE Global * 12.85 - 3.9% +14.6% (3.5%) 2.8%p 1.9%p - 0.41 - 0.12 - 1.29 LG Display 3.67 - 11.8% - 9.1% (△11.1%) 4.1%p 32.9%p 0.04 +0.02 0.00 Other Affiliates 1.09 +4.8% +20.6% (3.8%) 2.1%p 0.7%p Intercompany Transactions 1.72 0.02 * Consolidation based on LG Electronics Korea and overseas subsidiaries (excluding internal transactions) 1

- 5. Ⅰ. 2009 1Q Results (Consolidated) Sales and Profit by Division Sales and Profit* (Unit : KRW bn) 4Q’08 QoQ 1Q’09 YoY 1Q’08 Home Sales 4,986 13.8% 4,298 18.6% 3,622 Entertainment Op. Profit -31 14 -13 Mobile Sales 4,487 5.2% 4,253 16.8% 3,643 Communications Op. Profit 176 255 457 Sales 4,093 4.3% 3,916 22.6% 3,195 Handset Op. Profit 215 263 445 Home Sales 2,310 4.3% 2,211 16.1% 1,904 Appliance Op. Profit -50 102 84 Air Sales 684 86.2% 1,274 8.9% 1,170 Conditioning Op. Profit -11 61 61 Business Sales 1,181 7.3% 1,096 6.6% 1,173 Solution Op. Profit 20 27 27 * Consolidation based on LG Electronics Korea and overseas subsidiaries (excluding internal transactions) * Divisional sales includes internal transactions between divisions 2

- 6. Ⅱ. Performance and Outlook by Sector Home Entertainment Global* Performance 2009 1Q Performance (KRW tn) Op. Margin (%) Sales : Robust LCD TV sales led to growth YoY to 4.3 trillion KRW 0.7% 0.8% 0.3% -0.4% -0.6% even during recession and low season LCD TV Appropriate product line ups for recession and progressive sales activities led to 36% sales growth YoY PDP TV Sales growth of 0.3% YoY 4.99 3.98 4.30 Sales 3.62 3.78 PDP Module Sales declined 36% YoY from slow 32” external sales Profitability : Despite low performance of PDP modules, Media and 1Q’08 2Q’08 3Q’08 4Q’08 1Q’09 DS products, from great FPTV sales, profitability improved YoY FPTV Shipment by Region 2009 2Q Outlook (Unit: K) 3,538 Market : We expect the market growth rate to slow down QoQ, 211 Korea 40%↑ 397 CS America but growth will accelerate in emerging markets where LCD TV 2,523 205 601 N. America penetration is low, and in developed markets demand should pick 240 18%↑ 715 Asia* up (centered on 2nd TVs), so overall market demand (unit) is 509 46%↑ expected to increase slightly 491 1,614 Europe* LGE : In 2Q, EOL (End of Life) promotion for old models will unfold, 1,078 50%↑ and as many new models will be aggressively launched, we plan to 1Q’08 1Q’09 continuously expand market share * Asia - Includes MEA. Europe - Includes CIS * Pertains solely LG Electronics and its overseas subsidiaries (excluding internal transactions) 3

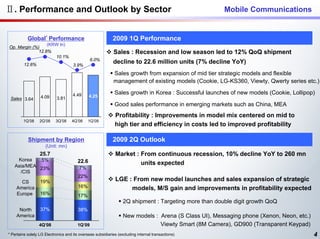

- 7. Ⅱ. Performance and Outlook by Sector Mobile Communications Global* Performance 2009 1Q Performance (KRW tn) Op. Margin (%) 12.8% Sales : Recession and low season led to 12% QoQ shipment 10.1% 6.0% 12.6% 3.9% decline to 22.6 million units (7% decline YoY) Sales growth from expansion of mid tier strategic models and flexible management of existing models (Cookie, LG-KS360, Viewty, Qwerty series etc.) 4.49 Sales growth in Korea : Successful launches of new models (Cookie, Lollipop) 4.09 3.81 4.25 Sales 3.64 Good sales performance in emerging markets such as China, MEA Profitability : Improvements in model mix centered on mid to 1Q’08 2Q’08 3Q’08 4Q’08 1Q’09 high tier and efficiency in costs led to improved profitability Shipment by Region 2009 2Q Outlook (Unit: mn) 25.7 Market : From continuous recession, 10% decline YoY to 260 mn Korea 5% 22.6 Asia/MEA units expected 23% 7% /CIS 22% CS 19% LGE : From new model launches and sales expansion of strategic America 16% models, M/S gain and improvements in profitability expected Europe 16% 17% 2Q shipment : Targeting more than double digit growth QoQ North 37% 38% America New models : Arena (S Class UI), Messaging phone (Xenon, Neon, etc.) 4Q’08 1Q’09 Viewty Smart (8M Camera), GD900 (Transparent Keypad) * Pertains solely LG Electronics and its overseas subsidiaries (excluding internal transactions) 4

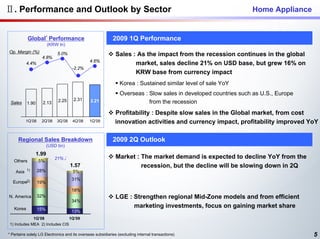

- 8. Ⅱ. Performance and Outlook by Sector Home Appliance Global* Performance 2009 1Q Performance (KRW tn) Op. Margin (%) 4.8% 5.0% Sales : As the impact from the recession continues in the global 4.6% 4.4% market, sales decline 21% on USD base, but grew 16% on -2.2% KRW base from currency impact Korea : Sustained similar level of sale YoY Overseas : Slow sales in developed countries such as U.S., Europe 2.25 2.31 2.21 Sales 1.90 2.13 from the recession Profitability : Despite slow sales in the Global market, from cost 1Q’08 2Q’08 3Q’08 4Q’08 1Q’09 innovation activities and currency impact, profitability improved YoY Regional Sales Breakdown 2009 2Q Outlook (USD bn) 1.99 21%↓ Market : The market demand is expected to decline YoY from the Others 5% 1.57 recession, but the decline will be slowing down in 2Q 1) 28% Asia 5% 31% Europe2) 19% 18% N. America 32% LGE : Strengthen regional Mid-Zone models and from efficient 34% Korea 15% marketing investments, focus on gaining market share 13% 1Q’08 1Q’09 1) Includes MEA 2) Includes CIS * Pertains solely LG Electronics and its overseas subsidiaries (excluding internal transactions) 5

- 9. Ⅱ. Performance and Outlook by Sector Air Conditioning Global* Performance 2009 1Q Performance (KRW tn) Op. Margin (%) 10.1% Sales : From the global recession, sales declined based on USD, 4.8% but based on KRW, sales improved slightly 2.2% 5.2% -1.6% Korea : Limited decline from new model launches and reservation sales Overseas : From recession and ’08 cool summer, overall industry’s 1.69 inventory situation is not good, leading to delayed sell-in Sales 1.17 1.27 0.98 0.68 Profitability : Despite sale decline, profitability improved from new model 1Q’08 2Q’08 3Q’08 4Q’08 1Q’09 launches, expansion of premium portion and cost innovation Regional Sales Breakdown 2009 2Q Outlook (KRW tn) Market : With the high seasonality, the demand is expected to pick 1.17 1.27 centered on the major markets MEA 22% 25% Asia 15% 17% Europe/CIS LGE : From continuous cost innovation activities and stronger 16% 10% marketing activities in strategic markets, market share N. America 23% 28% expansion will be targeted Korea 24% 21% 1Q’08 1Q’09 * Pertains solely LG Electronics and its overseas subsidiaries (excluding internal transactions) 6

- 10. Ⅱ. Performance and Outlook by Sector Business Solution Global* Performance 2009 1Q Performance (KRW tn) Op. Margin (%) Sales : Demand withdrawal impact from global recession led to 3.1% 2.5% sales decline 2.3% 1.8% 1.7% Monitor : Market demand decline and ASP drop led to YoY sales decline Commercial : Withdrawal of U.S./EU Hotel investments led to sales decline Sales 1.17 1.11 1.18 1.18 1.10 Car : Difficulties of GM business led to lower sales 1Q’08 2Q’08 3Q’08 4Q’08 1Q’09 Profitability : Improved YoY results from price competitiveness and enhanced operation efficiency Regional Sales Breakdown 2009 2Q Outlook (KRW tn) 1.17 1.10 Market : Recession continuing in developed countries such as CIS 3% 8% 7% U.S. and Europe, but stable growth in emerging countries expected MEA 11% 12% CS America 13% 14% LGE : Focus on sales improvement from new channels and models Asia 9% 20% Monitor : Sales growth from successful ‘Network Monitor’ launching N. America 20% 10% China 9% 10% Commercial : Sales growth from Pro:CentricTM Solution Hotel TV launch, Korea 8% 23% 26% discover new B2B channels Europe CAR : GM’s difficulties expected to continue, targeting 1Q’08 1Q’09 new built-in businesses * Pertains solely LG Electronics and its overseas subsidiaries (excluding internal transactions) 7

- 11. Ⅲ. 2009 1Q Results (Parent) Sales & Profit Sales Profit (Unit: KRW tn) (Unit: KRW bn) 7.07 +2.1% 6.93 4Q’08 QoQ 1Q’09 YoY 1Q’08 +7.3% 6.59 1.64 +2.2% Operating - 310 n/a 437 23% 564 Domestic 1.34 +22.1% 1.61 Profit EBITDA - 144 n/a 591 19% 732 Export 5.25 +3.6% 5.43 +2.2% 5.32 Recurring - 942 n/a - 144 n/a 498 Profit Net Profit - 671 n/a - 198 n/a 422 4Q’08 1Q’09 1Q’08 8

- 12. Ⅲ. 2009 1Q Results (Parent) Non-operating items Non-operating Items Equity Method (Unit : KRW bn) (Unit : KRW bn) Op. Profit 4Q’08 1Q’09 Others 6 Financial * 48 LG Display -214 -90 Expenses 437 Equity 211 Method Loss LGE Overseas Subsidiaries -47 -132 Recurring Profit Others -33 11 Foreign 316 Exchange - 144 Loss Equity Method Total -294 -211 * AR discount fee is included in financial expenses 9

- 13. Ⅲ. 2009 1Q Results (Parent) Cash Flow 1Q Net Cash Flow* Cash Flow (Unit : KRW bn) (Unit : KRW bn) Cash at the beginning of Quarter 1,207 Cash Out Cash In Net* Cash Flow from Operating Activities △ 136 Net Loss △ 198 Net Loss 198 Depreciation 153 △229 Equity Method Loss 211 Increase in Increase in Working Capital △ 183 Working 183 Increase in Notes Receivables, Etc. △ 319 Capital 199 Others Others 199 Cash Flow from Investing Activities △ 93 Increase CAPEX & Capital Investment △ 93 in Notes Equity Method 319 211 Receivables Loss Cash Flow from Financing Activities 376 Etc. Debt increase 376 CAPEX & 153 Depreciation Cash Increase 147 93 Capital Investment Cash at the end of Quarter 1,354 * Excludes cash flow from financing activities 10

- 14. Ⅲ. 2009 1Q Results (Parent) Financial Structure Balance Sheet Financial Ratio (Unit : KRW tn) (Unit : %) End of ’07 End of ’08 ’09.1Q End of ’07 End of ’08 ’09.1Q Assets 14.34 17.34 18.67 126 Current Assets 2.83 4.52 6.09 Total Liab. to Equity 106 Cash 0.53 1.21 1.35 99 Inventories 0.95 0.90 0.96 Fixed Assets 11.51 12.82 12.58 38 Debt to Equity 31 Liabilities 7.13 8.93 10.40 28 Current Liabilities 4.42 5.94 6.88 Long-Term Liabilities 2.71 2.99 3.52 Net Debt to 21 22 Equity 7.21 8.41 8.27 16 Equity Debt 2.05 2.59 3.15 11

- 15. Ⅳ. 2009 2Q Business Direction & Prospects From entering high season for AC and expansion of new product Growth Growth Sales launches in major product categories, we expect market share improvement to result in over 10% sales growth TV profitability to be similar QoQ, but improved HE profitability in PDP module / Media / DS expected Improved profitability expected from stronger strategic MC model line-ups and shipment increase Profitability Profitability HA Similar level of profitability QoQ AC Improved profitability from initial high season entrance BS Similar level of profitability QoQ 12

- 17. Appendix. 2009 Business Structure Change Before Digital Digital Digital Mobile Appliance Display Media Communications 2009 Home Air Home Business Mobile Appliance Conditioning Entertainment Solution Communications - Refrigerator - Residential Air Con. - LCD/CRT TV - Monitor No Changes - Washing Machine - Commercial Air Con. - PDP Module/TV - Hotel TV - Handset - C&C - BMS (Home Net) - Home A/V - Digital Signage - PC - Healthcare - Others - STB (Set Top Box) - Security - Others - Others - DS (Digital Storage) - Car Built-in - RMC (Recording Media Chemetronics)

- 18. Appendix Financial Statement (Parent) Income Statement (Unit : KRW bn) 2008 2009 1Q 2Q 3Q 4Q Total 1Q 2Q 3Q 4Q Total Sales 6,927 100.0% 7,234 100.0% 6,887 100.0% 6,591 100.0% 27,639 100.0% 7,074 100.0% Domestic 1,606 23.2% 1,760 24.3% 1,739 25.2% 1,341 20.3% 6,445 23.3% 1,637 23.1% Exports 5,321 76.8% 5,474 75.7% 5,148 74.8% 5,250 79.7% 21,193 76.7% 5,437 76.9% COGS 5,142 74.2% 5,264 72.8% 5,166 75.0% 5,250 79.7% 20,822 75.3% 5,402 76.4% Gross Profit 1,786 25.8% 1,970 27.2% 1,720 25.0% 1,341 20.3% 6,816 24.7% 1,672 23.6% SG&A 1,221 17.6% 1,335 18.5% 1,383 20.1% 1,650 25.0% 5,589 20.2% 1,235 17.5% Op. Profit 564 8.1% 635 8.8% 338 4.9% -310 -4.7% 1,227 4.4% 437 6.2% Non OP Income 582 8.4% 688 9.5% 386 5.6% 804 12.2% 2,459 8.9% 607 8.6% Non OP Expense 648 9.4% 398 5.5% 689 10.0% 1,435 21.8% 3,170 11.5% 1,187 16.8% Rec. Profit 498 7.2% 925 12.8% 34 0.5% -942 -14.3% 515 1.9% -144 -2.0% Tax 76 1.1% 218 3.0% 9 0.1% -270 -4.1% 32 0.1% 54 0.8% Net Profit 422 6.1% 707 9.8% 25 0.4% -671 -10.2% 483 1.7% -198 -2.8% * Recurring profit is equal to pre-tax profit from continuous operation. Balance Sheet (Unit : KRW bn) 2008 2009 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q Assets 16,306 17,314 18,444 17,338 18,670 Current Asset 4,394 4,533 5,415 4,518 6,088 Quick Asset 3,138 3,354 4,257 3,617 5,129 Inventories 1,256 1,179 1,157 901 959 Fized Asset 11,912 12,781 13,030 12,820 12,582 Investment 7,553 8,464 8,820 8,639 8,487 Tangible 3,962 3,852 3,737 3,711 3,633 Intangible 397 465 473 471 463 Liabilities 8,514 8,553 9,497 8,931 10,402 Current Liabilities 5,733 5,544 6,446 5,942 6,875 LT Liabilities 2,781 3,009 3,051 2,989 3,527 Capital 7,791 8,761 8,948 8,407 8,268

- 19. Appendix Divisional Sales (Parent) (Unit :KRW bn) 1Q'08 2Q'08 3Q'08 4Q'08 FY08 1Q'09 2Q'09 3Q'09 4Q'09 FY09 QoQ YoY Sales 1,538 1,485 1,688 1,324 6,035 1,512 14.2% -1.6% HE Op. Profit -89 -92 -72 -198 -451 -74 (%) -5.8% -6.2% -4.3% -14.9% -7.5% -4.9% Sales 3,423 3,710 3,393 3,668 14,193 3,682 0.4% 7.6% MC Op. Profit 479 531 368 46 1,424 311 (%) 14.0% 14.3% 10.8% 1.3% 10.0% 8.4% Sales 2,955 3,360 3,089 3,209 12,612 3,350 4.4% 13.4% Handset Op. Profit 468 547 384 75 1,475 311 (%) 15.9% 16.3% 12.4% 2.3% 11.7% 9.3% Sales 924 989 1,030 962 3,905 995 3.4% 7.6% HA Op. Profit 79 90 69 -67 171 143 (%) 8.5% 9.1% 6.7% -6.9% 4.4% 14.3% Sales 721 756 456 357 2,288 633 77.5% -12.2% AC Op. Profit 107 117 2 -56 170 96 (%) 14.9% 15.5% 0.4% -15.8% 7.4% 15.2% Sales 252 210 225 209 895 215 3.0% -14.5% BS Op. Profit -5 -13 -19 -36 -74 -34 (%) -2.1% -6.0% -8.6% -17.4% -8.2% -16.0% Sales 71 84 95 72 321 37 Others Op. Profit -7 2 -10 1 -14 -4 Sales 6,927 7,234 6,887 6,591 27,639 7,074 7.3% 2.1% Total Op. Profit 564 635 338 -310 1,227 437 (%) 8.1% 8.8% 4.9% -4.7% 4.4% 6.2% * Divisional sales includes internal transaction between divisions * Adjustments were made for apple to apple comparison based on 2009 business structure change.

- 20. Appendix Divisional Sales (Global*) (Unit :KRW bn) 1Q'08 2Q'08 3Q'08 4Q'08 FY08 1Q'09 2Q'09 3Q'09 4Q'09 FY09 QoQ YoY Sales 3,622 3,780 3,979 4,986 16,368 4,298 -13.8% 18.6% HE Op. Profit -13 27 33 -31 16 14 (%) -0.4% 0.7% 0.8% -0.6% 0.1% 0.3% Sales 3,643 4,086 3,815 4,487 16,030 4,253 -5.2% 16.8% MC Op. Profit 457 525 386 176 1,544 255 (%) 12.6% 12.8% 10.1% 3.9% 9.6% 6.0% Sales 3,195 3,754 3,514 4,093 14,556 3,916 -4.3% 22.6% Handset Op. Profit 445 541 405 215 1,606 263 (%) 13.9% 14.4% 11.5% 5.2% 11.0% 6.7% Sales 1,904 2,131 2,255 2,310 8,600 2,211 -4.3% 16.1% HA Op. Profit 84 103 112 -50 248 102 (%) 4.4% 4.8% 5.0% -2.2% 2.9% 4.6% Sales 1,170 1,690 983 684 4,527 1,274 86.2% 8.9% AC Op. Profit 61 170 22 -11 241 61 (%) 5.2% 10.1% 2.2% -1.6% 5.3% 4.8% Sales 1,173 1,113 1,177 1,181 4,645 1,096 -7.3% -6.6% BS Op. Profit 27 35 22 20 103 27 (%) 2.3% 3.1% 1.8% 1.7% 2.2% 2.5% Sales -295 -65 -199 -277 -837 -279 Others Op. Profit -10 -2 -4 -3 -20 -4 Sales 11,218 12,735 12,009 13,371 49,333 12,853 -3.9% 14.6% Total Op. Profit 605 856 570 101 2,133 456 (%) 5.4% 6.7% 4.8% 0.8% 4.3% 3.5% * Divisional sales pertains solely LG Electronics Korea and its overseas subsidiaries and includes internal transactions * Adjustments were made for apple to apple comparison based on 2009 business structure change.