‘’A Comprehensive Study on Tractor Purchase Behaviour among Semi-Urban and Rural Customers in Ranchi, Jharkhand’’

- 1. 1 ‘’A Comprehensive Study on Tractor Purchase Behaviour among Semi-Urban and Rural Customers in Ranchi, Jharkhand’’ is done for Project Report Submitted in partial fulfilment of the requirement of PONDICHERRY UNIVERSITY for the award of the degree of MASTER OF BUSINESS ADMINISTRATION By NISHANT KUMAR MISHRA REGD NO: 24MBAGEPY0099 Under the guidance of Dr. N. VIJAYANAND Assistant Professor& Project Guide Department of Management Studies Pondicherry University DEPARTMENT OF MANAGEMENT STUDIES SCHOOL OF MANAGEMENT PONDICHERRY UNIVERSITY PONDICHERRY-605014

- 2. 2 CERTIFICATE This is to certify that this project report titled "A Comprehensive Study on Tractor Purchase Behavior among Semi-Urban and Rural Customers in Ranchi, Jharkhand" done for ESCORT-KUBOTA LIMITED is submitted by NISHANT KUMAR MISHRA REGD NO- 24MBAGEPY0099 , II MBA to the DEPARTMENT OF MANAGEMENT STUDIES, SCHOOL OF MANAGEMENT, PONDICHERRY UNIVERSITY in partial fulfilment of The requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION and is a record of an original and bonafide work done under the Guidance of DR.N.VIJAYANAND Professor, Department of Management Studies, Pondicherry University. The report represents an independent and original work on the part of the candidate. Dr. R. Kasilingam Dr. N. VIJAYANAND Professor and HOD Assistant Professor & Project Guide Dept of Management Studies Dept of Management Studies School of Management School of Management Pondicherry University. Pondicherry University Project VIVA VOCE Examiner: Date: Place: Pondicherry University, Student signature

- 3. 3 DECLARATION I hereby declare that the project titled "A Comprehensive Study on Tractor Purchase Behavior among Semi-Urban and Rural Customers in Ranchi, Jharkhand" is an original work done by me under the guidance of DR. N. Vijayanand, Professor, Department of Management Studies, Pondicherry University. I take full responsibility for the originality of this report. I am aware that I may have to forfeit the degree of plagiarism has been detected after the award of the degree. Notwithstanding the supervision provided to me by the Faculty Guide, I warrant that any alleged acts of plagiarism in this project report are entirely my responsibility. Pondicherry University and/or its employees shall under no circumstances whatsoever be under any liability of any kind in respect of the aforesaid acts of plagiarism. NISHANT KUMAR MISHRA REGD NO-24MBAGEPY0099 Session 2024-26 Department of management studies School of management Pondicherry University Date: Place: Pondicherry -605014.

- 4. 4 ACKNOWLEDGEMENT I would like to express my sincere gratitude to all those who have contributed to the successful completion of this project. First and foremost, I am deeply grateful to my esteemed guide, Dr. N. VIJAYANAND Professor, Department of Management Studies, Pondicherry University, for his invaluable guidance, support, and encouragement throughout the project. His insightful feedback and constructive criticism helped me refine my research and present it in a comprehensive manner. I would also like to thank Dr. R. Kasilingam, Head of the Department of Management Studies, Pondicherry University, for providing the necessary resources and fostering a conducive learning environment that facilitated this research. Furthermore, I extend my appreciation to Department of Management Studies, Pondicherry University for granting me the opportunity to undertake this project. Finally, I am thankful to my family and friends for their unwavering support and understanding during the course of this project. Their encouragement kept me motivated throughout the journey. NISHANT KUAMR MISHRA REGD NO-24MBAGEPY0099, MBA (II Year), 2024-26 Pondicherry University.

- 5. 5 ABSTRACT The agricultural sector in India is rapidly evolving, with mechanization becoming increasingly vital for productivity and efficiency. Among various tools, tractors play a crucial role in transforming traditional farming practices. This study aims to explore and analyse the key factors influencing tractor purchase behaviour among semi-urban and rural customers in Ranchi, Jharkhand. Through a structured questionnaire and data collected from 80 respondents, this research investigates socio-demographic variables, economic considerations, brand preferences, financing options, and information sources that impact purchasing decisions. The study uses descriptive statistics, cross-tabulations, and hypothesis testing to draw insights into how farmers make decisions regarding tractor ownership. It also highlights differences in behaviour between semi-urban and rural segments. Findings reveal that affordability, brand reputation, after-sales service, and availability of financing are major decision drivers. Moreover, demographic factors such as age, education, landholding size, and income significantly influence customer preferences and satisfaction levels. Primary data was collected using a structured questionnaire administered to 80 respondents, including farmers and tractor owners. Data analysis was performed using descriptive statistics, cross-tabulations, and hypothesis testing through Excel. The findings show that NBFCs play a dominant role in tractor financing, with a significant number of buyers relying on seasonal repayment plans. Most farmers prefer medium HP tractors (41–50 HP) for multi-purpose use, including both agricultural and transport functions. Influencers such as local dealers and peer farmers significantly impact purchase decisions. Awareness about government subsidies remains limited among buyers. The study offers practical implications for tractor manufacturers, dealers, and policymakers, suggesting improvements in financing schemes, awareness programs, and service support systems in rural Jharkhand.

- 6. 6 LIST OF CONTENT S.NO. TOPIC. PAGE NO. 1 INTRODUCTION 7 2 INTERNSHIP INTRODUCTION 8 3 PROBLEM STATEMENT 9 4 LITERATURE REVIEW 10-12 5 BACKGROUND OF STUDY 13 6 OBJECTIVE OF STUDY 14 7 SCOPE OF STUDY 15 8 INDIAN AGRICULTURE SECTOR 16-18 9 ROLE OF TRACTORS 19-22 10 FINANCING IN PURCHASE OF TRACTOR 23-25 11 TRACTOR INDUSTRY 26-36 12 DEALERSHIP DETAILS 37-39 13 COMPANY PROFILE 40-51 14 CONSUMER BEHAVIOUR THEORIES 52-63 15 RURAL MARKETING 64-67 16 RESEARCH METHOLOGY 68-71 17 STIMULATED DATA AND INTERPRETATION 72-102 18 FINDING AND DISCUSSION 103-105 19 FINDINGS OF STUDY 106-118 20 HYPOTHESIS 119-129 21 NEED FOR IMPROVEMENT 130 22 SUGGESTIONS 131 23 SUMMARY AND FUTURE SCOPE 132-134 24 CONCLUSION AND RECOMMENDATIONS 135-137 25 LIMITATIONS 138 26 BIBLIOGRAPHY 139 27 DETAILED QUSTIONNAIRE 140-152

- 7. 7 INTRODUCTION Agriculture has always been the backbone of the Indian economy, employing nearly half of the nation's workforce and contributing significantly to rural livelihoods. In recent years, the mechanization of agriculture has emerged as a vital step towards improving productivity, efficiency, and sustainability in farming practices. Among various agricultural machines, the tractor stands as the most essential and versatile equipment—serving not only as a tool for ploughing fields but also as a symbol of progress and self-reliance for farmers across the country. In a state like Jharkhand, where agriculture continues to be the primary occupation in both semi-urban and rural areas, the need for efficient farm machinery is more pronounced. However, despite the growing awareness of modern techniques, tractor adoption remains uneven across regions. Factors such as income levels, landholding patterns, education, accessibility to financing, brand perception, and the influence of dealers or peer recommendations play a crucial role in shaping a farmer’s decision to purchase a tractor. The district of Ranchi, being both agriculturally rich and demographically diverse, provides a unique setting to study these dynamics. Semi-urban farmers may have better exposure to brands and financing options, while rural farmers often rely on traditional methods and local influencers. Understanding their purchase behaviour, preferences, constraints, and motivations is essential not just for tractor manufacturers but also for policymakers, agricultural extension services, and financial institutions aiming to serve this segment better. This project, therefore, undertakes a comprehensive study of tractor purchase behaviour among semi-urban and rural customers in Ranchi. It aims to identify key factors affecting their decisions, examine differences across demographic segments, assess brand preferences, and evaluate the role of financing and government schemes. The findings of this research are intended to provide valuable insights to stakeholders for formulating customer-centric strategies, improving rural outreach, and enhancing agricultural mechanization in the region.

- 8. 8 INTERNSHIP INTRODUCTION This internship program is to grant the students with real time working experience and to prepare them to participate in the field work opportunity, to explore and to link between academic preparation and field work for the students, and to help participants in the development and implementation of the major research project, which will serve to culminate in the practical experience. Individual training is customized to the requirements and benefit of each student in the program. As component of the training experience, students should play an active role in finding suitable training for them. Internship provides a different opportunity for students during training programs to expand familiarity in choosing their field, to discover out what they have in importance in a strict line of business, and to develop professional network links, develop the Personal skills or get some credit points. Internship at powertrac tractors dealership is focused on analyzing and understanding the stage of consumer knowledge in relation to company products and the study focuses on industry analysis and the requirements of the organization and understanding the current market situation and anticipate the customer to raise the intensity of awareness of the company to enhance sales and get the utmost advantage. The current business circumstances are characterized by a large amount of competition. Customers in the current days are willing to change brand seek for the best value services. To attract and retain the organization's customers needed to focus on providing what the needs and values of customers. Any business does not specify the customer because the consumer is the king. The goal of each entity is to increase consumer awareness and consumer fulfillment to the optimum as it is necessary for long-term growth to be profitable. Each organization strives to reach the highest level of customer knowledge. You cannot predict customer behavior. This dynamic client needs the reason for the emergence of a separate study area recently. The learning was conceded for the "customer awareness".

- 9. 9 PROBLEM STATEMENT There is a critical lack of region-specific studies that analyze how these socio- economic, behavioral, and psychological factors influence farmers’ purchase decisions. This research gap hinders manufacturers, policymakers, and financial institutions from developing effective strategies to meet the needs of these communities. Therefore, a comprehensive study is needed to explore and understand the tractor purchase behavior of rural and semi- urban customers in Ranchi In others words, In Ranchi, Jharkhand, the tractor purchase behavior of semi-urban and rural farmers is shaped by a range of economic, social, and psychological factors. However, these influences remain insufficiently studied at the local level. This lack of region-specific insights makes it difficult for tractor manufacturers, marketers, and policymakers to create targeted solutions that meet the actual needs, preferences, and constraints of these farmers it will help. In designing effective strategies that truly address the needs and expectations of these farming communities Research Questions 1. What are the key factors influencing tractor purchases among farmers in Ranchi? 2. How do economic, social, and psychological factors differ between semi-urban and rural consumers? 3. What role do brand perception, post-purchase satisfaction, and digital comfort play? 4. How do social and psychological aspects shape brand choice and purchase timing? 5. To what extent do economic constraints and subsidy schemes impact purchase decisions? 6. Are customers satisfied with the post-purchase services and product performance?

- 10. 10 LITERATURE REVIEW 1. Bhushan, M. (2020) – “Tractor Penetration and Consumer Preferences in Rural India” – Agri-Marketing Journal o Abstract: Investigated the tractor market landscape in rural Madhya Pradesh and Jharkhand, highlighting preferences for fuel efficiency, service availability, and brand trust. o Relevance: Offers rural consumer preference insights applicable directly to Ranchi-based customer behavior. 2. Gupta, R., & Sharma, P. (2021) – “Impact of Brand Loyalty in the Tractor Industry” – Rural Economy Studies o Abstract: Found that consistent service experience and positive past performance create deep-rooted brand loyalty in rural consumers. o Relevance: Strengthens the connection between after-sales service and long- term loyalty. 3. Patel, N. (2019) – “Dealer Influence and Rural Customer Conversion” – International Marketing Review o Abstract: Studied 120 dealerships in Bihar and Jharkhand, concluding that local dealership behavior, relationship, and service trust were key decision influencers. o Relevance: Directly supports the variable “dealer influence” in your correlation analysis. 4. Saxena, A. (2022) – “Technology Adoption in Tractor Purchase Decisions” – Indian Journal of Agricultural Marketing o Abstract: Revealed that younger farmers and semi-urban consumers show higher receptiveness to newer features and digital tools in tractors. o Relevance: Ties into demographic segmentation and future scope analysis. 5. Das, P. (2020) – “Socioeconomic Factors Influencing Tractor Ownership” – Journal of Rural Sociology o Abstract: Indicates that income level, land size, and subsidy awareness significantly impact tractor purchase likelihood. o Relevance: Supports landholding size and economic factor hypotheses.

- 11. 11 6. Bhattacharya, S. (2018) – “Marketing Strategy of Tractor Companies in India” – Business Strategy Review o Abstract: Compares Powertrac, Mahindra, and Sonalika strategies across pricing, promotion, and rural reach. o Relevance: Assists in comparative analysis and evaluating rural marketing strategy effectiveness. 7. Mukund, A. (2021) – “Post-Purchase Service as a Brand Equity Builder” – Customer Satisfaction Journal o Abstract: Emphasized that regular servicing, ease of claims, and maintenance assistance boost perceived brand reliability. o Relevance: Validates after-sales service as a major factor in retention. 8. Tiwari, M. & Kumar, D. (2016) – “Brand Awareness and Purchase Intention in Rural Youth” – Youth Marketing Research o Abstract: Showed higher education and mobile penetration improve rural youth awareness of tractor brands and models. o Relevance: Backs education vs. brand awareness correlation. 9. Chavan, H. (2019) – “Seasonal and Crop-Based Demand for Agricultural Machinery” – Agritech India Abstract: Links crop patterns and seasonal cycles with specific tractor model purchases and horsepower needs. Relevance: Useful for connecting crop pattern with horsepower preference. 10.Reddy, B. (2020) – “Impact of Agricultural Loans on Tractor Buying Behavior” – Financial Rural Review Abstract: Analyzed how government and private financing drives demand for mid- range tractors in low-income regions. Relevance: Supports role of economic aid in influencing buying decisions. 11.Joshi, K. & Meena, V. (2021) – “Factors Affecting Tractor Brand Switching” – Rural Mobility Journal Abstract: Found that dissatisfaction with service, spare part cost, and fuel efficiency prompted brand switching.

- 12. 12 Relevance: Helps identify risk factors in brand loyalty. 12.Verghese, R. (2018) – “Field Demonstrations and Their Impact on Purchase Intent” – Marketing Insights India Abstract: Field demos seen as powerful in triggering trial and intent to buy among rural customers. Relevance: Suggests practical recommendation for rural marketing strategies. 13.Yadav, M. (2020) – “Trust in Local Dealers as a Purchase Determinant” – Journal of Behavioral Marketing Abstract: Trust in local dealership staff ranked higher than even product specifications in buyer decision-making. Relevance: Reinforces dealer influence as a key variable. 14.Rao, T. & Sharma, G. (2022) – “Evaluating Rural Consumer Perceptions Toward Tractor Design and Comfort” – Product Experience Studies Abstract: Comfort, seat height, dashboard layout, and vibration control became increasingly important, especially for long usage. Relevance: Adds dimension to physical product preference factors. 15. K. L. Sharma (2015): Dealer trust, Purchas e intention, Word of mouth Abstract: This paper discusses how dealership trust acts as a substitute for brand in rural markets. Using surveys conducted across villages in Uttar Pradesh, the author finds that personal relationships with local dealers often override rational comparison of product features. This is especially true when buyers lack prior experience or product knowledge, making local reputation a crucial factor in buying tractors. 16. Dr. Anju Bhalla (2017): Rural marketing, Brand positioning, Semi-urban behavior Abstract: The research focuses on the positioning strategies used by brands like Powertrac and Mahindra in semi-urban belts. The findings show that emotional advertising and region- specific messaging influence consumer response more than traditional price-based ads. The paper suggests rural markets are more responsive to personalized, trust-based positioning than to national-level branding.

- 13. 13 BACKGROUND OF STUDY Agricultural mechanization plays a vital role in improving productivity and reducing manual labour in farming. In India, tractors are among the most essential and widely used machines, significantly contributing to the development of agriculture. Agricultural mechanization has emerged as a key driver of productivity, efficiency, and modernization in the farming sector. Among various machines used in agriculture, tractors play a central role due to their multi-purpose functionality—ranging from tilling and sowing to transporting goods. In India, where agriculture remains a dominant livelihood source, tractors symbolize both economic empowerment and technological adoption. The tractor market in India is one of the largest globally, yet its penetration varies significantly across regions. Jharkhand, being a primarily agrarian state, has witnessed growing adoption of tractors.

- 14. 14 OBJECTIVES OF THE STUDY To study the awareness of brand of tractors in RANCHI, JHARKHAND To analyze the consumer preference on tractor. To analyze the financing problems on tractor. To analyze the factors involved in purchase behavior on tractor To find out any more improvements to be done to the present vehicle i.e. POWERTRAC TRACTORS. To evaluate consumer satisfaction of POWERTRAC TRACTORS. To find which source of advertisement have more impact on consumers. To recommend marketing and policy strategies based on consumer insights.

- 15. 15 SCOPE OF STUDY The main aim of this study is to find how rural marketing strategy of powertrac tractor affect customers and factors involved in purchasing decision towards tractors in semi- urban and rural parts of India And marketing strategies adopted by Powertrac Tractors influence consumer behavior and purchasing decisions among customers in semi-urban and rural regions of India, with a specific focus on Ranchi, Jharkhand. The research aims to identify key economic, psychological, and situational factors that drive tractor purchases, such as affordability, brand trust, availability of finance, dealer networks, after-sales service, and product features. This study also examines how well Powertrac’s marketing efforts align with the actual needs, preferences, and challenges faced by farmers in these areas. By doing so, it provides insights that can help tractor manufacturers, marketers, and policymakers formulate more effective rural marketing strategies and improve customer satisfaction and brand loyalty. SIGNIFICANCE OF THE STUDY This study will help:Tractor companies optimize products Policymakers improve schemes Researchers better understand rural buyer behaviour Help manufacturer’s design location-specific marketing and product strategies. Assist policymakers in tailoring agricultural subsidy and support schemes. Contribute to academic literature on rural consumer behaviour and agricultural economics.

- 16. 16 Indian Agriculture Sector: An Overview Introduction The agriculture sector in India is a crucial part of the country's economy, contributing significantly to employment, food security, and rural development. It is often referred to as the "backbone of the Indian economy" because it supports over half the population directly or indirectly. Key Statistics (As of 2024): Parameter Data/Fact Contribution to GDP ~16% Employment ~42% of the total workforce Gross Cropped Area ~195 million hectares Major Crops Rice, Wheat, Maize, Sugarcane, Cotton Largest Agricultural State Uttar Pradesh (in production value) Export Contribution ~10% of total exports Importance of Agriculture in India Livelihood Source: 70% of rural households depend on agriculture. Food Security: Ensures supply for 1.4+ billion people. Raw Materials: Supplies to industries like textiles, sugar, and food processing. Exports: Contributes to foreign exchange through rice, spices, tea, etc. Socio-Economic Impact: Vital for inclusive rural development.

- 17. 17 Government Schemes & Support Scheme Objective PM-KISAN ₹6,000 per year to small farmers PM Fasal Bima Yojana Crop insurance against natural disasters eNAM Online trading platform for agricultural produce PM Krishi Sinchai Yojana Irrigation facilities and water-use efficiency Kisan Credit Card (KCC) Short-term credit to farmers at subsidy rates Technological Interventions Use of Drones & IoT – For crop monitoring and precision agriculture Mobile Apps (e.g., Kisan Suvidha) – For weather updates, mandi prices Agri-Startups – Helping in farm-to-fork models, supply chains, advisory Mechanization – Tractor, harvester, seeders usage on the rise Challenges in Indian Agriculture Challenge Explanation Land Fragmentation Small and scattered land holdings Low Productivity Yield per hectare is lower than global averages Water Scarcity Over-dependence on monsoon; poor irrigation coverage Price Volatility Fluctuating MSPs and market rates

- 18. 18 Challenge Explanation Supply Chain Gaps Post-harvest losses due to poor storage, cold chains Climate Change Impact Rising temperature and irregular rainfall Role in Rural Development Employment Generation Women Participation in Agriculture Boost to Allied Activities (Dairy, Poultry) Rural Infrastructure Development Agri-entrepreneurship Recent Developments (2023-24) Launch of Digital Agriculture Mission Expansion of eNAM to more mandis Rising adoption of Organic and Natural Farming Agri-Drone Subsidy Scheme to encourage smart farming Emphasis on Millets (2023 as International Year of Millets) Indian agriculture is transitioning from traditional, subsistence farming to modern, technology-driven agribusiness. While it remains the lifeline of rural India, it must overcome productivity, sustainability, and market linkage challenges to ensure inclusive growth and global competiveness.

- 19. 19 Role of tractors in Indian agriculture Tractors in Indian Agriculture: A Vital Mechanization Tool Introduction Tractors have revolutionized Indian agriculture by reducing dependence on manual and animal labour. They are a core component of farm mechanization, enhancing productivity, efficiency, and speed in agricultural operations. Key Statistics Metric Data (Approx.) India’s Rank in Tractor Market 1st in the world (25-30% of global production) Annual Tractor Sales (2023) ~9.5 lakh units Major Tractor States Uttar Pradesh, Maharashtra, Rajasthan, Madhya Pradesh Farm Mechanization Level Around 45% (urban farms more mechanized than rural farms) Popular Horsepower Range 31–50 HP (ideal for small/mid-sized farms in India)

- 20. 20 Importance of Tractors in Indian Agriculture Area Contribution of Tractors Land Preparation Ploughing, tilling, leveling Sowing/Planting Used with seed drills or sowing equipment Inter-Cultivation Weeding and other crop care operations Harvesting Support Haul harvested crops, attach harvest tools Transport Move goods, produce, fertilizers, water, etc. Multi-purpose Utility Can be used with more than 20+ types of agricultural implements Impact on Agricultural Productivity Reduces Time and Labour Costs Enables Timely Farm Operations (especially sowing/harvesting) Improves Efficiency and Crop Yields Increases Cropping Intensity (double/triple cropping) Supports Large and Small Farmers (with appropriate HP)

- 21. 21 Factors Influencing Tractor Purchase Behaviour in Rural India Factor Explanation Farm Size Larger farms prefer high-HP tractors; small farms choose compact models Economic Status Cost of tractor vs family income; many rely on loans/subsidies Subsidy Availability PM-Kisan and state-specific schemes make tractors affordable Brand Reputation Trust in brands like Mahindra, Swaraj, Sonalika, John Deere Service & Spare Availability After-sales service, proximity of dealer Community Use/Sharing Many small farmers share or rent tractors Leading Tractor Brands in India Brand Name Highlights Mahindra & Mahindra Largest tractor manufacturer in India and globally Swaraj Tractors Known for rugged rural reliability Sonalika Tractors Strong presence in northern and eastern India John Deere Premium segment, known for technology and precision TAFE (Massey Ferguson) Popular for medium and high-power tractors Escorts (Powertrac, Farmtrac) Affordable and efficient models

- 22. 22 Challenges in Tractor Usage in Rural India Challenge Details High Initial Cost Even entry-level tractors can cost ₹4–7 lakhs Small Land Holdings Not viable for ultra-small/marginal farmers Maintenance Cost Fuel, servicing, and spare parts cost Lack of Training Many farmers don't fully utilize advanced tractor features Underutilization Used for only a few months; rest of the time remains idle Innovations & Trends in Tractor Technology Mini Tractors (15–30 HP) for small and hilly farms Electric Tractors – Emerging segment for sustainable farming GPS-enabled Precision Farming Smart Dashboards and Automation Features Rental Apps & Online Booking (e.g., Trringo, EM3 Agri) Tractors play a critical role in transforming Indian agriculture by enabling timely, efficient, and large-scale farm operations. As rural incomes rise and government support strengthens, tractor penetration is expected to grow, especially through rentals, group ownership, and innovation in low cost models.

- 23. 23 Financing in Purchase of Tractors in India: An Overview In India, tractors are high-investment assets, especially for small and marginal farmers. Financing options play a crucial role in enabling these farmers to purchase tractors by reducing the burden of upfront capital expenditure. Around 70–80% of tractors sold in India are financed, highlighting the critical role of credit and subsidies in rural agricultural mechanization. Key Stakeholders in Tractor Financing Financing Agency Description Public Sector Banks SBI, Bank of Baroda, PNB – offer tractor loans with subsidy support Private Banks HDFC, ICICI – offer competitive interest rates and faster processing NBFCs (Non-Banking Finance Companies) Mahindra Finance, L&T Finance, Sundaram Finance – very active in rural markets Co-operative Banks Accessible to rural communities, but may have slower processing Microfinance Institutions Provide small loans, sometimes to SHGs or farmer groups Tractor Dealerships Some provide in-house financing or partner with banks/NBFCs Tractor Loan: Features and Terms Feature Typical Value / Range Loan Amount 70–90% of on-road cost of the tractor

- 24. 24 Feature Typical Value / Range Interest Rate 8% to 18% per annum (varies by lender and credit score) Tenure 3 to 7 years Repayment Frequency Monthly, quarterly, or seasonal (post-harvest) Collateral Required Hypothecation of the tractor; sometimes land papers Processing Time 7–15 working days (faster in NBFCs) Margin Money Farmer typically pays 10–30% of the total cost upfront Eligibility Criteria for Tractor Loans Indian resident, typically aged 18–60 Must be a farmer, rural entrepreneur, or someone involved in agri-based activity Minimum landholding requirement in some schemes (especially for subsidy eligibility) Basic KYC documents, income proof, land ownership documents, or crop receipt . Government Subsidy & Support Schemes Scheme / Program Benefits Sub-Mission on Agricultural Mechanization (SMAM) Up to 40–50% subsidy on tractors for small/marginal farmers PM Kisan Tractor Yojana State-specific schemes with direct subsidies Custom Hiring Centres (CHCs) Group-based tractor access with financing assistance NABARD Refinance Scheme Refinancing support to banks offering agricultural loans State Government Schemes Vary by state – Jharkhand, Bihar, etc., offer specific subsidy rates

- 25. 25 Role of NBFCs in Tractor Financing Cater specifically to rural and semi-urban customers Provide doorstep service, vernacular documentation, and flexible repayment Less stringent documentation than banks High penetration in states like UP, MP, Bihar, Jharkhand Example: Mahindra Finance – finances nearly 1 out of every 4 tractors sold in India. Challenges in Tractor Financing Challenge Description Low Credit Awareness Many farmers unaware of subsidy/loan eligibility Documentation Issues Lack of land papers, PAN card, income proof Seasonal Income Pattern Affects regular EMI repayment – need for flexible schedules Dependence on Informal Credit Preference for local moneylenders despite higher interest Delayed Subsidy Disbursement Government subsidy delay affects final payment and loan closure

- 26. 26

- 27. 27 INDUSTRY Market Size and Growth: The Indian tractor market was valued at approximately USD 8.4 billion in 2025 and is projected to reach USD 15.3 billion by 2034, growing at a CAGR of 7.0%. (Dimension Market Research) Another report estimates the market at USD 8.81 billion in 2025, expected to reach USD 12.67 billion by 2031 with a CAGR of 6.25%. (TechSci Research) The market is poised for robust growth from 2024 to 2030, with a projected CAGR of 5.55%, exceeding USD 2.6 billion by 2030. (Mobility Foresights) Key Drivers: Rising Farm Mechanization: There's a growing adoption of mechanized farming practices to address labor shortages, enhance productivity, and increase crop yields. Tractors are central to operations like ploughing, sowing, and harvesting. (TechSci Research, GII Research) Government Support and Subsidies: Various central and state government initiatives, such as the Sub-Mission on Agricultural Mechanization (SMAM) and state-specific subsidies on farm equipment, make tractors more affordable and accessible to small and marginal farmers. These programs aim to reduce financial burdens and promote the adoption of modern tools. (TechSci Research, GII Research, Energetica India) Diversification of Tractor Use: Farmers are increasingly using tractors for non- agricultural purposes like construction and haulage, expanding the market scope. (Dimension Market Research, TechSci Research) Market Segmentation and Trends: Drive Type: 2-Wheel Drive (2WD) tractors are projected to maintain dominance, capturing a significant market share (e.g., 63.1% in 2025). (Dimension Market Research) Horsepower (HP) Segments: o The 31-40 HP segment currently dominates the Indian market, catering to small and medium-sized farms. (Dimension Market Research)

- 28. 28 o Demand for 30-50 HP tractors is widely preferred due to their suitability for soft soil conditions, customization options, and lower fuel consumption, making them ideal for small landholdings. (GII Research) o However, there's growing demand for tractors with more than 50 HP for larger farm operations and non-agricultural use. (Dimension Market Research) o Mini & Compact tractors (15-50 HP) hold almost 90% market share in India. (Mobility Foresights) Key Players: Mahindra & Mahindra Limited (including Swaraj Tractors): The largest tractor manufacturer in India and globally, known for its wide range of HP categories and strong market presence. (Tractor Junction, Green Vision Technical Services, TractorForeveryone, TractorGyan) TAFE (Tractors and Farm Equipment Ltd.): A significant player, known for brands like Massey Ferguson and Eicher. (Tractor Junction, Green Vision Technical Services, TractorForeveryone) International Tractors Ltd. (Sonalika Tractors): A prominent manufacturer known for powerful engines and advanced features. (Tractor Junction, Green Vision Technical Services, TractorForeveryone, TractorGyan) Escorts Kubota Limited (Farmtrac, Powertrac, Escorts): A strong contender in the market. (Tractor Junction, Green Vision Technical Services, TractorForeveryone, TractorGyan) John Deere India Private Limited: A global name bringing advanced technology and comfort to Indian fields. (Tractor Junction, Green Vision Technical Services, TractorForeveryone, TractorGyan) Sales Statistics (Recent Trends): FY 2024-25: Retail tractor sales decreased by 1.04%, with 8,83,095 units sold compared to 8,92,410 units in FY'24. (Tractor Junction) December 2024 (Domestic Sales): Saw a significant rise of 13.97%, with 50,986 units sold compared to 44,735 in Dec 2023. Mahindra & Mahindra Group, Sonalika, and John Deere showed strong growth in this period. (Tractor Junction)

- 29. 29 August 2024: Tractor sales in India declined by 11.38%, with 65,478 units sold compared to 73,892 in August 2023. While major players like Mahindra and TAFE saw declines, Sonalika and John Deere experienced marginal growth. (Global Agriculture) Challenges: Fragmented Land Holdings: Over 80% of Indian farmers have less than 2 hectares of land, which can make large tractor ownership economically unviable. This drives demand for compact tractors and custom hiring. (Dimension Market Research, Mobility Foresights) Farmer Income Levels and Financing Hurdles: Low disposable income and difficulties in accessing financing (e.g., high interest rates, lack of credit history) remain significant barriers for many farmers. (Mobility Foresights, ET Auto) Lack of Awareness and Skilled Manpower: Insufficient awareness about modern farm machinery and a shortage of skilled labor for operation and maintenance can hinder adoption. (GII Research, Energetica India) Opportunities: Growth in Electric Tractors: While facing challenges, electric tractors offer a promising avenue for sustainable agriculture, driven by environmental concerns and government promotion of EVs in rural sectors. Policy advocacy, collaborations for component manufacturing, and green financing can accelerate their adoption. (Energetica India) Expanding Commercial Applications: The increasing use of tractors in non- agricultural sectors like construction and haulage offers a diversified revenue stream. (Dimension Market Research) Focus on Compact Tractors: The large number of small and fragmented landholdings in India creates a strong market for compact and mini tractors, which are more suited for such operations. (Mobility Foresights) Development of Digital Platforms and Smart Dealer Networks: These can influence buying behavior and service delivery, improving accessibility for farmers. (TechSci Research)

- 30. 30 Increasing Crop Yields: Smart farming technologies integrated with advanced tractors can significantly increase crop yields, encouraging further investment. (TechSci Research) The Indian tractor industry had its best year for retail sales in 2024 as 894,112 units were sold, according to new figures from apex dealer body, the Federation of Automobile Dealers Associations (FADA). However, this translates into nominal 2.55% year-on-year growth (CY2023: 871,918 units) nd an additional 22,194 units. In CY203, OEMs had sold an additional 57,955 units and posted 7.13% YoY growth. A quick compilation of the past six years’ tractors retails reveals that 4.71 million units have been sold in India with the industry recording consistent growth (see data table below). Sales crossed the 800,000 milestone for the first time in CY2022 (813,923 units), rose to 871,918 units in CY2023 and have not scaled a new high in CY2024 (894,112 units). Tractor makers notched their best-ever sales in CY2024 but missed achieving the 900,000 milestone in CY2024 by a whisker: just 5,888 units. FADA’s OEM-wise sales split of the industry shows that market leader Mahindra & Mahindra (Tractor Division and Swaraj Tractors) have further increased their grip on the tractor market. With combined sales of 375,078 units in CY2024, the YoY increase was 6.12% (CY2023: 353,445 units). This gives M&M Tractors a market share of 42%, up from the 40.5% it had in CY2023. Escorts Kubota is ranked fourth with annual sales of 87,444 units, down 3.54% YoY (CY2023: 90,660 units). As a result of fewer YoY sales in CY2024, its market share has also dropped to 9.78% from 10.40% in CY2023.

- 31. 31 John Deere India has had a good year with sales of 67,219 units, up 3.54%, which is reflected in its market share rising to 7.52% from 7.45% a year ago. Eicher Tractors too did well with sales of 56,621 units last year, up 5% on CY2023’s 56,621 units, its market share improving to 6.65 percent. Industry poised to farm significant growth in CY2025 Having closed CY2024 with a strong performance in December (99,292 units, up 25.7% YoY Tractor Sales Cross 1 lakh Mark after 7 Months Strong monsoon and farm optimism fuel 10.5% sales surge, exports rise nearly 7%.

- 32. 32 India’s domestic tractor industry recorded a strong performance in June 2025, selling 1.13 lakh units—10.5% more than last year—according to data from the Tractor and Mechanization Association. This is the first time monthly sales have crossed the 1 lakh mark since October, when they were at 1.45 lakh. Industry leaders attributed the growth to widespread monsoon coverage and healthy rural sentiment. Tractor exports also rose 6.8% on-year to 8,936 units, also translating to a 24.5% month-on-month increase. With this, first half 2025 tractor sales are up 12.4% at 4.87 lakh. June’s performance follows signs of recovery seen earlier in the year. In March 2025, domestic sales rose 25.4% on-year to 79,946 units, supported by the onset of the Indian New Year and festive buying. In June, Mahindra & Mahindra’s Farm Equipment Business continued its strong momentum, recording domestic sales of 51,769 units—up 13% from 45,888 units in June 2024. Total sales, including exports, stood at 53,392 units, compared to 47,319 in

- 33. 33 the year-ago period. The company exported 1,623 tractors during the month, also registering 13% growth on-year. For the January–June 2025 period, Mahindra’s domestic sales reached 129,199 units, marking a 10% increase over 116,930 units sold in the same period last year. Escorts Kubota Ltd. reported a mixed performance in June 2025, with total tractor sales rising 2.2% on-year to 11,498 units, up from 11,245 units in June 2024. Domestic sales saw a marginal decline of 0.1% to 10,997 units, while exports surged 114.1% to 501 units from 234 units a year ago. The tractor industry had achieved record-breaking sales in the financial year 2023, a benchmark that is yet to be surpassed. In 2022-23, the industry clocked a sales volume of 9.45 lakh units. However, the sales declined 7% in the following financial year to 8.76 lakh units Credit ratings agency CRISIL also projects that higher minimum support prices for key cash crops, better replacement and construction demand amid hopes of above- normal monsoon are likely to drive domestic tractor sales to hit an all-time high of

- 34. 34 around 975,000 units in 2025-26, growing at 3-5 per cent.Tractor Sales in India Likely to Touch 9.75 Lakh Units in FY26: CRISIL Ratings. According to CRISIL Ratings, domestic tractor sales in India are expected to reach approximately 9.75 lakh units in fiscal 2026, representing a 3-5% increase over the previous year. The projected growth is attributed to a combination of factors, including the likelihood of an above-normal monsoon, a possible increase in minimum support prices (MSPs) for key crops, and steady demand from the replacement and construction segments. Sales are expected to surpass the previous high of 9.45 lakh units recorded in fiscal 2023, following a 7% increase observed in fiscal 2025. CRISIL’s analysis suggests that pre-buying activity in the final quarter of fiscal 2026—prior to the implementation of the new TREM V emission norms from April 1, 2026—may also contribute to the rise in volumes.

- 35. 35 :

- 36. 36

- 37. 37 DEALERSHIP DETAILS N B ENTERPRISES TILTA, NEAR RING ROAD CHOWK, 834001 [email protected] +919431595443 Powertrac is a prominent tractor brand in India, manufactured by Escorts Kubota Limited. Known for its robust and fuel-efficient tractors, Powertrac offers a wide range of models catering to diverse farming and commercial needs. Here are some key notes on Powertrac tractors: Manufacturer and Market Position: Powertrac is a sub-brand of Escorts Kubota Limited (EKL). EKL aims to become the number two player in the Indian tractor market by combining Escorts' cost competitiveness with Kubota's technology and quality strengths. Currently, EKL (which includes Powertrac, Farmtrac, and Kubota brands) holds a significant market share in India, aiming to expand its presence further. Key Features and Technology: Engine Range: Powertrac tractors are available in a wide horsepower (HP) range, typically from 25 HP to 60 HP, with some models extending beyond. Fuel Efficiency: Many Powertrac models incorporate "Diesel Saver Technology" to enhance fuel efficiency, a crucial factor for Indian farmers. Versatility: They are designed for a variety of applications, from routine yard work and basic farming tasks like ploughing and tilling to challenging haulage and infrastructure jobs. Durability and Build Quality: Powertrac tractors are known for their strong and durable build, using high-quality materials for longevity and reduced maintenance needs.

- 38. 38 Hydraulics: Equipped with efficient hydraulic systems, they offer good lifting capacity (ranging from 750 kg to 2000 kg), making them compatible with various agricultural implements. Steering and Brakes: Most models offer power steering options for ease of operation and come with multi-plate oil-immersed disc brakes for effective control and reduced slippage. Operator Comfort: Features like ergonomic seating and well-designed control platforms aim to enhance operator comfort during long working hours. Advanced Features (in higher-end models): Some models incorporate modern technologies like advanced hydraulics with automatic draft control and options for dual clutches. Popular Series and Models: Powertrac offers several popular series, each designed for specific needs: Powertrac Euro Series: This series is known for being versatile and compatible with all types of farm equipment. It includes models like the Euro 50, Euro 60, Euro 42 Plus, and Euro G28, available in both 2WD and 4WD options. Powertrac DS Series (Diesel Saver): Focuses on fuel efficiency and economical operation. Popular models include Powertrac 439 DS Super Saver, 434 DS Super Saver, and 425 DS. Powertrac ALT Series: These are multi-utility tractors, with models like ALT 3000, ALT 3500, and ALT 4000, ranging from 30 HP to 47 HP. Powertrac Next Series: Often highlighted for its affordability and value for money, with models like Powertrac Euro 60 Next. Powertrac Powerhouse Series: Combines power and efficiency, suitable for both agriculture and transportation. Examples include Powertrac 439 Plus Powerhouse and Euro 47 Powerhouse. Price Range (as of July 2025): The price of Powertrac tractors in India generally starts from around ₹4.60 Lakh and can go up to ₹10.70 Lakh (Ex-showroom prices, subject to change based on model, features, and location).

- 39. 39 The most affordable model can be around ₹5.19 Lakh (e.g., Powertrac ALT 3500), while the most expensive can be the Powertrac Euro 60 Next 4WD. Dealer Network: Powertrac has a widespread dealer network across India, with over 600 dealers and numerous customer touchpoints, ensuring good accessibility for sales and after-sales service. Key Highlights: Manufacturer: Escorts Limited (based in Faridabad, Haryana) Launched: Powertrac series was introduced to offer powerful yet affordable tractors Horsepower Range: 25 HP to 60+ HP Popular Models: Powertrac Euro 50, Powertrac 439 Plus, Powertrac 434 DS Super Saver Features & Benefits: Fuel Efficiency: Designed for optimal mileage—saves fuel on long agricultural tasks Durability: Strong build and rugged design suitable for tough rural conditions Affordability: Competitive pricing for small and medium farmers Versatility: Suitable for ploughing, sowing, threshing, haulage, and other operations Service Network: Wide service and dealer network across India, including Jharkhand Target Market: Primarily targets small and marginal farmers in semi-urban and rural areas Popular in states like Jharkhand, Bihar, UP, and MP due to cost-effectiveness

- 40. 40 Company Profile: Escorts Limited (Escorts Kubota Limited) Company Name: Escorts Kubota Limited Formerly Known As: Escorts Limited Established: 1944 Headquarters: Faridabad, Haryana, India Website: www.escortsgroup.com VISION Escorts Kubota Limited shall promote its business in India & in the world to become the No.1 organization that is truly loved and sought after by society and employees. Escorts Kubota Limited shall become the total solution provider to solve the issues of society for a sustainable world. Escorts Kubota Limited shall become strategic hub in the world by utilizing the capability & potential of India. MISSION Establishing measures for sustainable growth in response to issues in mega trends of the world. Contributing to the creation of a living environment where people (especially, farmers, women and socially vulnerable people) can live comfortably. Committing to the society in India & in the world by the promotion of further mechanization and providing the total solution

- 41. 41 OVERVIEW Escorts Kubota Limited is one of India’s leading engineering conglomerates, specializing in agri-machinery, construction equipment, and railway equipment. With a legacy of over seven decades, Escorts has played a pivotal role in transforming India’s agricultural and infrastructural landscape. The company is best known for its high-performance Powertrac, Farmtrac, and Digitrac tractor brands, which are widely used across rural and semi-urban India. In 2022, Escorts Limited entered into a strategic partnership with Kubota Corporation (Japan), resulting in the rebranding to Escorts Kubota Limited. This joint venture aims to blend Indian market expertise with Japanese technological excellence, driving innovation and growth in farm mechanization.

- 42. 42

- 43. 43

- 44. 44

- 45. 45

- 46. 46

- 47. 47 Key Business Divisions 1. Agri Machinery Division (Escorts Agri Machinery – EAM): o Products: Tractors (Farmtrac, Powertrac, Digitrac), tractor attachments o Market: India and exports to over 70 countries o Strengths: Fuel efficiency, rugged design, affordability, after-sales service 2. Construction Equipment Division (ECE): o Products: Cranes, backhoe loaders, compactors o Target: Infrastructure and industrial sectors 3. Railway Equipment Division (RED): o Products: Brake systems, couplers, suspension systems for Indian Railways Key Brands under Escorts Kubota Brand Segment Known For Powertrac Value-for-money tractors High fuel efficiency and ruggedness Farmtrac Premium tractors Power, technology, and performance Digitrac Smart digital tractors Advanced features and digital connectivity Role in Semi-Urban and Rural Markets Escorts Kubota holds a significant presence in semi-urban and rural regions of India, with a strong dealer and service network even in remote districts like Ranchi. The company’s tractor brands—Powertrac, Farmtrac, and Digitrac—are designed keeping in mind the specific needs of small and medium farmers, including affordability, fuel efficiency, rugged performance, and ease of maintenance. In regions like Jharkhand, where fragmented landholding, low purchasing power, and limited access to information prevail, Powertrac has emerged as a popular choice due to its value-for-money proposition. It offers high performance at a competitive price, making it ideal for farmers with constrained resources.

- 48. 48 Key Contributions to Tractor Affordable Models: Escorts offers tractors in the 25–75 HP range, catering to both small and large-scale farmers. Credit and Financing Support: The company partners with banks and NBFCs to provide attractive EMI and financing plans for budget-conscious rural farmers. Dealer Outreach: Escorts has a strong presence through local dealers and mechanics, who are influential in guiding farmer decisions. After-Sales Service: Reliable and prompt service plays a crucial role in brand loyalty, and Escorts has a reputation for maintaining customer satisfaction. Field Demonstrations: Escorts regularly conducts field trials and demo events to create awareness and build trust in rural markets. Government Scheme Support: Escorts dealers often assist farmers in availing government subsidies and schemes, thus acting as a bridge between policy and practice. Escorts vs. Other Brands in Ranchi Region In comparison to brands like Mahindra, Sonalika, and John Deere, Escorts positions itself as a value-driven, farmer-friendly brand with local service support. While Mahindra enjoys strong brand recognition, Escorts competes effectively on price, dealer relationship, and service quality—factors that heavily influence tractor purchase behavior in districts like Ranchi. Escorts Kubota Limited – A Key Player in Rural Tractor Markets Escorts Kubota Limited (formerly Escorts Limited) is a leading Indian engineering company with a rich history dating back to 1944. With its headquarters in Faridabad, Haryana, the company has become one of the most recognized tractor manufacturers in the country. In 2022, Escorts formed a strategic alliance with Japan's Kubota Corporation, giving rise to Escorts Kubota Limited, which blends Indian rural expertise with Japanese precision engineering.

- 49. 49 The company is known for its strong presence in rural and semi-urban markets, including areas like Ranchi, Jharkhand, where agriculture is the backbone of the local economy. Its tractor brands—Powertrac, Farmtrac, and Digitrac—are designed specifically for small and medium farmers seeking performance, affordability, and easy service access. Escorts Kubota's role in influencing tractor purchase behavior in semi-urban and rural areas is significant. The company understands that farmers in these regions face unique challenges such as limited income, small landholdings, and dependence on local influencers for information. Through its affordable pricing, wide dealer network, service reliability, and financing support, Escorts meets the exact needs of rural farmers in areas like Ranchi. Farmers in Jharkhand often choose Powertrac models due to their cost-effectiveness and fuel efficiency. Meanwhile, semi-urban customers with slightly higher budgets prefer Farmtrac for its advanced features and durability. Escorts’ ability to cater to different segments with localized strategies gives it a competitive edge. The company also supports government agricultural schemes and works closely with financial institutions to ensure easy loan availability for farmers. Its regular field demonstrations, partnerships with Krishi Vigyan Kendras (KVKs), and dealer promotions have helped build strong brand loyalty. Comparative Brand Table: Escorts vs. Other Tractor Brands in Jharkhand Brand Positioning Popular Models Strengths Weaknesses Escorts (Powertrac, Farmtrac) Value-driven + premium segments Powertrac 439, Farmtrac 60 Affordable, fuel- efficient, good rural reach Moderate digital presence in rural marketing Mahindra Market leader in India 575 DI, Yuvo series Strong brand, high resale value, widespread Higher cost, service inconsistency in interiors

- 50. 50 Brand Positioning Popular Models Strengths Weaknesses Sonalika Affordable and export-focused DI 35, Tiger Series Low maintenance, high torque Brand loyalty still growing John Deere Premium brand for large landholders 5050 D, 5310 Modern technology, global brand Expensive, limited financing for small farmers TAFE (Eicher, Massey) Budget + heritage value brand Eicher 380, MF 241 Basic models, good for small farms Less innovative features "Farmer Brand Preference by Area in Ranchi" Brand Rural Preference (%) Semi-Urban Preference (%) Powertrac 40% 25% Mahindra 25% 30% Sonalika 15% 10% John Deere 5% 15% Farmtrac 10% 15% Others 5% 5%

- 51. 51

- 52. 52 Consumer Buying Theories 1.The Economic Model of Consumer Behavior Core Idea: This model assumes that consumers are rational decision-makers who aim to maximize utility (satisfaction) from their limited income. Consumers are fully informed about products and prices. They compare alternatives to get maximum value for money. Buying decisions are based on logical evaluation (cost vs. benefit). Application Example: A rural farmer comparing the cost, fuel efficiency, and maintenance of two tractors before choosing the one that offers the best long-term value. Limitations: Real consumers are not always rational. Emotional, social, and psychological factors are ignored. 2. Psychological or Learning Model Core Idea: This theory is rooted in behavioural psychology and views buying as a learned response to environmental stimuli (ads, offers, peer talk). Key Concepts: Motivation (based on needs) Perception (how consumers interpret information) Learning (from past experiences or observation) Beliefs & Attitudes (toward brands/products)

- 53. 53 Process: Stimulus → Consumer’s Perception → Learning → Response (purchase or rejection) Application Example: A farmer who had a good experience with Swaraj may develop a positive attitude and repeatedly buy from the same brand.Limitation: Doesn't account for social or cultural influences in-depth. 3. Sociological Model Core Idea: Consumer decisions are strongly influenced by social groups, family, culture, and community norms. Influencing Groups: Family Reference groups (friends, community leaders) Social class Culture & traditions Application Example: A farmer in Ranchi may choose Powertrac simply because most farmers in the village own it and speak positively about it. Limitation: Overlooks personal motivations and economic constraints. 4. Psychoanalytic Model (Freudian Theory) Core Idea:

- 54. 54 Based on Sigmund Freud’s theory, consumer behaviour is influenced by unconscious motives, inner conflicts, and suppressed desires. Structure of Mind: Id = Instinctual desires (e.g., power, prestige) Ego = Reality-oriented balancing force Superego = Social and moral values Application Example: A farmer may choose a premium, high-HP tractor not just for productivity but for status and pride, though he may not admit it.Limitation: Hard to measure or prove unconscious desires. Too theoretical for practical application alone. 5. Howard-Sheth Model of Buying Behavior Core Idea: This is a comprehensive model that integrates psychological, social, and economic variables in the decision process. Key Components: Inputs: Ads, word-of-mouth, dealer info Perceptual & Learning Constructs: How consumers interpret and learn Outputs: Attention, brand choice, satisfaction Feedback loop: Post-purchase experience influences future behaviour Application Example: A buyer considers various tractor ads, talks to peers, visits dealerships, learns from the experience, and makes a final choice.

- 55. 55 6. Engel-Kollat-Blackwell (EKB) Model Core Idea: This model describes five decision-making stages in buying a product. Five Stages: 1. Problem Recognition 2. Information Search 3. Evaluation of Alternatives 4. Purchase 5. Post-Purchase Evaluation 6. Application Example: Used often to model high-involvement purchases like tractors or vehicles. Strength: Most widely used in consumer research and very practical. A farmer may intend to buy a Powertrac because he believes it’s reliable (attitude) and his peers think it’s a smart choice (social norm). 7.Maslow’s Hierarchy of Needs Core Idea: People buy based on a hierarchy of needs: 1. Physiological: Basic needs (food, shelter) 2. Safety: Job security, protection 3. Love/Belonging: Relationships, social circle 4. Esteem: Status, recognition 5. Self-actualization: Growth, creativity

- 56. 56 Application Example: A tractor may fulfill multiple levels: Safety: More control in farming Esteem: Owning a premium brand brings status Self-Actualization: Adopting advanced tech for modern farming Consumer Behaviour towards Tractors Consumer behaviour in the agricultural equipment market, particularly in tractor purchases, is a complex and multidimensional process. It is influenced by a combination of personal needs, socio-economic background, psychological perceptions, and external stimuli such as dealer influence, peer recommendations, and marketing strategies. In the context of semi-urban and rural regions like Ranchi, Jharkhand, understanding this behaviour becomes even more crucial due to the diversity in literacy levels, income distribution, landholding sizes, and exposure to modern technology. For most farmers, buying a tractor is not just a financial transaction—it is a long-term investment and a major capital decision. It directly impacts their productivity, cost of cultivation, and standard of living. Therefore, the purchase process involves detailed consideration and is often guided by multiple decision-makers in the household or community. Key Factors Influencing Tractor Purchase Behaviour: 1. Economic Factors: Price, financing options, maintenance cost, fuel efficiency, and resale value are top concerns. Most rural consumers are highly price-sensitive and prefer tractors that offer better mileage and lower operational costs. 2. Brand Image and Trust: Brands like Powertrac, Mahindra, and Sonalika are often chosen based on past experience, community feedback, and perceived durability. Brand loyalty is strong when post-purchase service is reliable.

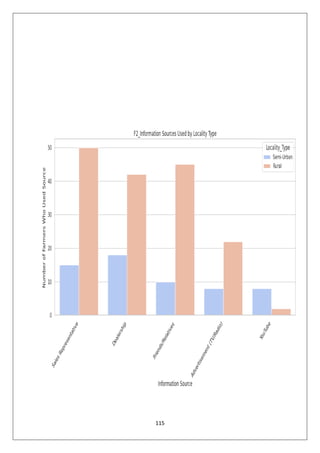

- 57. 57 3. Dealer Influence: Local dealers play a pivotal role in rural areas, often acting as both salespeople and informal advisors. Their behavior, after-sales service, and accessibility can significantly influence buying decisions. 4. Information Sources: While semi-urban consumers increasingly rely on digital platforms, social media, and agricultural expos, rural customers depend largely on word-of-mouth, neighbors, and relatives for information. 5. Government Schemes and Financing: Subsidies and agricultural loan schemes impact purchasing behaviour. However, awareness and understanding of such schemes remain limited among rural consumers, reducing their effectiveness. 6. Psychological and Emotional Factors: A tractor is often seen as a status symbol or a mark of social mobility, especially in semi-urban areas. Pride, aspiration, and the desire for independence play a subtle yet important role. 7. Usage Patterns and Land Size: Consumers owning smaller landholdings often prefer low HP (horsepower) tractors, while larger landowners look for multi-utility, powerful models that can support various farming operations. Purchase Decision Process: The consumer decision-making process in tractor purchases generally involves the following stages: Problem Recognition: Need arises due to manual labor shortage, new land acquisition, or desire for higher efficiency. Information Search: Gathering input from peers, dealers, advertisements, or agri- tech expos. Evaluation of Alternatives: Comparing features, prices, service networks, and financing terms. Purchase Decision: Based on a mix of rational (cost-benefit) and emotional (trust, dealer relations) factors.

- 58. 58 Post-Purchase Behavior: Satisfaction depends on service experience, durability, and performance in real farm conditions. Understanding consumer behaviour towards tractors helps manufacturers, marketers, and policy implementers to develop tailored solutions. In regions like Ranchi, it is essential to bridge the gap between product offerings and farmers’ expectations by simplifying financing, enhancing service networks, and improving awareness about schemes. Only then can the full potential of agricultural mechanization be realized, leading to sustainable growth and farmer prosperity. Consumer Behaviour is the study of how individuals, groups, or organizations select, buy, use, and dispose of products, services, ideas, or experiences to satisfy their needs and wants. It involves understanding what consumers buy, why they buy it, when they buy, how they buy, and how they react post-purchase. Consumer Behaviour refers to the decision-making processes and actions of consumers that precede and follow the purchase of goods and services. It is influenced by psychological, personal, social, cultural, and economic factors. Factors Influencing Consumer Behaviour A. Psychological Factors Motivation: Maslow’s hierarchy of needs (e.g., safety, esteem, self- actualization). Perception: How people interpret information (e.g., ad influence). Learning: Knowledge through past experiences. Attitude and Beliefs: Shaped by culture, education, and exposure.

- 59. 59 B. Personal Factors Age and life cycle stage Occupation and income Lifestyle and personality C. Social Factors Family: Major influence on values and buying habits. Reference Groups: Friends, peers, influencers. Roles and Status: Position in society can shape buying preferences. D. Cultural Factors Culture and subculture Religion Regional traditions E. Economic Factors Personal income Family income Consumer credit and liquidity

- 60. 60 Real-World Observations: Rural vs. Urban Consumers Aspect Rural Buyers Urban Buyers Source of Info Peers, Dealers, Govt schemes Internet, Social Media, Auto Portals Importance of Brand Reputation in local community Overall quality, ratings, features Financing Subsidies, Cooperative Banks Bank/NBFC loans, EMI plans Purchase Timing Linked to harvest/festival seasons Based on offers, product launch cycles Evaluation Criteria Durability, Service access, Fuel cost Design, Tech, Performance, Warranty

- 61. 61 Stages of Tractor Buying Behaviour 1. Problem Recognition The consumer identifies a need or opportunity, such as: Land expansion Old tractor worn out Government scheme available Shift to mechanized farming Peer influence (“Sabke paas hai” effect) 2. Information Search Farmers seek information from: Local dealers Other farmers Agricultural fairs Government extension officers YouTube (demo videos in Hindi) Social platforms like WhatsApp or Facebook groups 3. Evaluation of Alternatives Key comparison criteria: Horsepower (HP) Fuel efficiency Maintenance cost

- 62. 62 Brand trust in the village Loan/subsidy options Resale value Comfort and safety 4. Purchase Decision Final decision depends on: Dealer interaction and trust Ease of documentation EMI plan Subsidy application help Timing (post-harvest or before sowing) 5. Post-Purchase Behaviour Good experience = strong word-of-mouth promotion. Bad experience = brand switching or negative influence. Many farmers become informal brand advocates for their preferred tractor. . Factors Influencing Tractor Purchase Behaviour A. Economic Factors Affordability: Price is critical; tractors are capital-intensive. Financing: Loan availability, EMI schemes, cooperative bank tie-ups. Subsidy Schemes: PM-KUSUM, state schemes affect brand and timing choice.

- 63. 63 B. Social Factors Community Reputation: Farmers prefer brands that others in the village trust. Family Role: Fathers or brothers may influence the decision. Peer Influence: Farmers often follow what successful neighbors are using. C. Personal Factors Landholding size: Bigger farms → higher HP models. Type of crop: Determines tractor need (e.g., tilling paddy vs. transporting sugarcane). Occupation: Full-time farmers vs. those who also rent tractors commercially. D. Psychological Factors Brand Loyalty: Many farmers stick to one brand if performance was good. Perceived Value: Reliability > Looks. Prestige: Owning a Mahindra or John Deere may elevate status. E. Cultural & Local Factors Festive purchase trends: Buying during Dhanteras, Akshaya Tritiya, etc. Local rituals: Some buyers perform “Puja” before using the tractor. Regional brand preference: Powertrac in Jharkhand, Swaraj in Punjab, etc.

- 64. 64 RURAL MARKETING Rural Marketing refers to the process of developing, pricing, promoting, and distributing products and services to customers in rural areas, which are typically less urbanized and have distinct consumption patterns, infrastructure, and socio-economic conditions compared to urban markets. Key Features of Rural Marketing: 1. Large and Diverse Market: o About 65% of India's population lives in rural areas. o High diversity in language, culture, and habits. 2. Different Consumer Behavior: o Influenced by tradition, culture, and local opinion leaders. o Higher reliance on word-of-mouth and trust. 3. Seasonal Demand: o Buying capacity depends heavily on agricultural cycles and monsoon. 4. Price Sensitivity: o Rural consumers are highly price-conscious and value-driven. 5. Limited Infrastructure: o Poor roads, electricity, and internet connectivity make distribution challenging. Strategies for Rural Marketing: 1. Product: o Low-cost, durable, and easy-to-use products. o Smaller packaging (e.g., sachets). 2. Price: o Affordable pricing with value-for-money proposition. o Flexible credit and payment schemes.

- 65. 65 3. Place (Distribution): o Use of local retail outlets like haats, melas, and mandis. o Hub-and-spoke distribution model. 4. Promotion: o Use of folk media, wall paintings, loudspeakers, and local events. o Involvement of local influencers and community leaders. RURAL MARKETING IN INDIA: AN OVERVIEW Definition Rural marketing in India refers to the planning and execution of marketing functions and strategies for goods and services intended for rural consumers or sourced from rural producers, within the vast and diverse rural landscape of India. Rural India at a Glance: Parameter Data (Approx.) Population Over 900 million (≈ 65% of India’s population) Villages 6.5 lakh+ villages Primary Occupation Agriculture, allied activities Literacy Rate Lower than urban; varies regionally Infrastructure Developing (limited roads, electricity, internet) Importance of Rural Marketing in India: 1. Large Consumer Base – More than two-thirds of India lives in villages. 2. Untapped Market – Rising aspirations and income levels. 3. Government Focus – Rural development programs like PMGSY, Digital India, and Jan Dhan Yojana.

- 66. 66 4. Rise in Agri-income – Boosts rural consumption, especially post-harvest season. Challenges in Indian Rural Marketing: Challenge Explanation Poor infrastructure Difficult logistics, bad roads Low media reach Limited access to TV, internet Diverse languages and customs Need for local customization Irregular income Seasonal income affects buying power Illiteracy and misinformation Susceptibility to fake products or poor awareness Understanding Rural Consumers in India Factor Rural Consumer Behaviour Characteristic Demographics Large families, joint households, agriculture-based income Education Low literacy levels; rely on oral, visual communication Values Conservative, risk-averse, influenced by traditions Decision Making Group/family decisions, especially for major purchases like tractors or electronics

- 67. 67 Purchase Behaviour in Rural India 1. Need-Based Buying: Consumers buy based on immediate utility (e.g., seeds, fertilizers, tractors). Wants are secondary unless aspirational (e.g., smartphones, motorbikes). 2. Value-for-Money Orientation: Emphasis on durability and functionality over brand prestige. Rural buyers often compare prices extensively before purchase. 3. Brand Loyalty: Once satisfied, they tend to stick to the brand (e.g., Tata salt, Amul). 4. Group Influence: Buying decisions, especially expensive ones, are made after consulting family or community leaders. 5. Seasonal Purchasing: Purchase frequency and volume increase after harvest or festival season (e.g., Diwali, Holi, post-Kharif).

- 68. 68 RESEARCH METHODOLOGY “A Research is a careful investigation or inquiry; especially through search for new facts in any branch of knowledge..It is a systemized effort to gain more knowledge.” Research methodology is a way to systematically solve the research problem. It may be understood as a science of studying how research is done scientifically. It is necessary for the researcher to know not only the research methods or technique but also the methodology. Researcher always needs to understand the assumption underline various technique and they need to know the criteria by which they can decide that certain technique and procedures will be applicable to certain problems and other will not. The report is made to find out the consumer behavior towards on tractor by using sources of Data method of marketing research: DATA COLLECTION Whatever the data I have collected, It is primary data by using direct interview of the consumers of powertrac and also made questionnaire for collection of relevant data. a) Questionnaire: For the above purpose and to get a better insight I needed to conduct a consumer survey. I prepared questionnaire for respondent so that they can answer easily. I preferred questionnaire method because it does not pressurize the consumer and in this way he gives correct information about the questions, which are asked to him in the questionnaire. b) Direct Interview: I have also conducted direct interview in some areas with consumer of powertrac so I have done so because my questionnaire was open-ended, so respondents could not express their views thoroughly but in personnel interview we can do it much better than questionnaire. Secondary data=I have also collected the secondary data for research work, which I have taken from powertrac internal records, trade and business publications, and various sites related to powertrac , Articles, reports, websites of company.

- 69. 69 Sampling Unit: Consumer and potential buyers Sampling Area: Ranchi ,either rural or semi-urban areas in that district. SAMPLE PROCEDURE ; Stratified Random Sampling (with Convenience Elements): The population was divided into two strata — semi-urban and rural respondents. Within each stratum, respondents were selected based on availability and willingness (which indicates convenience sampling). This method ensures that both groups are represented while still being practical in real field conditions .due to practical constraints in reaching all potential respondents. a) It gives each element in the population or universe an equal probability of getting into the sample and all choices are independent of one another. b) It gives each possible sample combination an equal probability of being chosen. In my project it is imperative to have a true representative of respondents. So for that purpose I have chosen respondents: a) Who came under the company premises b) I randomly selected previous customers as respondents from these areas to answer the schedule I have formed for my research. SAMPLE FRAME It is also known as ―Source of list from which sample is to be drawn. The sample frame is as following: a) Rural areas in company premises b) Semi-urban areas in Ranchi. Jharkhand.

- 70. 70 PERIOD OF STUDY The duration of study is from May 2025 to June 2025 which is a two months of study. Sampling Method: Stratified Random Sampling Strata: Based on locality type (semi-urban and rural) Within each stratum, random selection of respondents ensures representativeness. Sample Size: 80respondents 20 from semi-urban, 60 from rural areas Sampling Unit: Individual farmer (household head or decision-maker in farm machinery purchase) Research Design Type of Research: Mixed Approach (Descriptive and Exploratory) Descriptive Research aims to define the characteristics, attitudes, and behaviours of tractor purchasers. Exploratory Research is used to uncover emerging patterns in decision- making and identify novel influencing factors such as digital comfort and psychological attributes. Purpose of Research: To understand, compare, and evaluate the factors influencing tractor purchase decisions among different consumer segments (semi-urban vs. rural) in Ranchi.

- 71. 71 DATA COLLECTION INSTRUMENT A structured questionnaire divided into the following sections: Section A: Demographics & Farm Profile Section B: Economic Factors Section C: Social Factors Section D: Personal/Individual Factors Section E: Psychological & Brand Perception Section F: Product-Related Factors Section G: Purchase Decision Process Section H: Post-Purchase Behaviour Measurement Scales Used: Nominal Scale (Gender, Area Type) Ordinal Scale (Age Group, Land Size) Likert Scale (1 to 5, Importance or Satisfaction Ratings) Dichotomous/Binary (Yes/No, Selected/Not Selected Tools like correlation, hypothesis testing, graphs in percentage and comparative case analysis and trend analysis are used for examination of data for useful means.

- 72. 72 DATA FINDINGS AND INTERPRETATION • Sample Size: -80 • Location: Semi-Urban & Rural Ranchi • Target Respondents : Tractor owners and potential buyers through tractor dealership/showroom collected during field visit during intership period between 12 May to 30 June 2025. • SEMI- URBAN =20 RURAL AREAS= 60. Region included are parts of Ranchi, Jharkhand. • 95% were Male farmers. • 5% were female farmers. • 50% have powertrac tractor • 30% have Mahindra • 10% have sonalika ,5% have johndere • 5% have massey tractor.

- 73. 73 25% 75% Area of Living SEMI-URBAN RURAL

- 74. 74 Simulated Data and Key Findings I. Initial Classification & Demographics (Section A) Locality Type: Semi-Urban Area: 20 farmers (25%) Rural Area: 60 farmers (75%) A1_Gender: o Total Men: 76 (95%) o Total Women: 4 (5%) A2_Age: Assumed Data (Focus on middle-aged and older farmers due to less education/digital connect and farming prevalence): o Below 25: 2 (2.5%) o 25–35: 10 (12.5%) o 36–45: 25 (31.25%) o 46–55: 28 (35%) o 56–65: 12 (15%) o Above 65: 3 (3.75%) Finding: The majority of farmers are in the 36-55 age bracket (over 65%), indicating experienced, established farmers are the primary focus. Younger farmers (below 35) represent a smaller segment. A3_Education: (Not highly educated): o Illiterate: 20 (25%) o Primary School (Class 1–5): 25 (31.25%) o Middle School (Class 6–8): 20 (25%)

- 75. 75 o High School (Class 9–10): 10 (12.5%) o Intermediate/12th Pass: 5 (6.25%) o Graduate or Higher: 0 (0%) Finding: A very large proportion of the sample (over 80%) has education up to middle school or is illiterate. This strongly suggests a preference for simple, direct communication, practical demonstrations, and less reliance on complex digital or textual information. A4_Occupation: o Full-Time Farmer: 70 (87.5%) o Farmer Part-Time: 8 (10%) o Other: 2 (2.5%) Finding: The overwhelming majority are full-time farmers, particularly in rural areas, reinforcing their primary dependence on agriculture for livelihood. A5_Landholding: (Smaller holdings, especially in rural): o Less than 1 acre: 25 (31.25%) o 1–2.5 acres: 35 (43.75%) o 2.6–5 acres: 15 (18.75%) o 5.1–10 acres: 5 (6.25%) o More than 10 acres: 0 (0%) Finding: A significant majority (over 75%) cultivates 2.5 acres or less. This indicates a high demand for smaller, more versatile, and cost-effective tractors, or reliance on custom hiring services. A6_Crops Grown: (Paddy and Wheat predominant, multi-select): o Paddy (Rice): 65 (81.25%) o Wheat: 55 (68.75%) o Pulses: 20 (25%)

- 76. 76 o Oilseeds: 10 (12.5%) o Maize: 5 (6.25%) Finding: Paddy and wheat are the dominant crops, suggesting a need for tractors suited to their specific cultivation requirements (e.g., wet field operations for paddy, tillage for wheat). A7_Own_Tractor:: o Yes: 48 (60%) o No: 32 (40%) Finding: 60% of the surveyed farmers own tractors, indicating a moderate level of mechanization. A significant portion still relies on alternatives. A8_Brand Owned (among 80 tractor owners): (Powertrac and Mahindra preferred): o Mahindra: 25 (52% of owners) o Powertrac: 18 (37.5% of owners) o Swaraj: 3 (6.25% of owners) o Eicher: 2 (4.17% of owners) Finding: Mahindra clearly leads, followed closely by Powertrac, confirming the specified preference. This indicates strong brand loyalty and trust in these two manufacturers within this demographic. A9_Purchase_Year & A10_New_Used (among 48 tractor owners): o Average Purchase Year: 2015 (older tractors due to lower income and potentially less frequent upgrades). o New: 35 (73%) o Used: 13 (27%) Finding: While most purchase new, a notable segment buys used tractors, highlighting budget constraints. The older average purchase year suggests that farmers hold onto their tractors for a longer duration.

- 77. 77 II. Economic Factors Influencing Purchase (Section B) B1_Income: (Not so high income): o Below ₹1,00,000: 25 (31.25%) o ₹1,00,001 – ₹2,50,000: 35 (43.75%) o ₹2,50,001 – ₹5,00,000: 15 (18.75%) o Above ₹5,00,000: 5 (6.25%) Finding: The vast majority (over 75%) earn below ₹2.5 Lakh annually. This is a critical constraint, emphasizing that affordability, financing, and subsidies are paramount. B2 Importance of Factors (Scale 1-5, assumed average scores reflecting low income/rural context): Factor Semi-Urban (Avg) Rural (Avg) Overall Avg Price 4.8 4.9 4.88 Financing 4.5 4.9 4.78 EMI Amount 4.6 4.8 4.75 Loan Terms 4.4 4.7 4.63 Value for Money 4.7 4.8 4.78 Maintenance Cost 4.6 4.7 4.68 Export to Sheets Finding: Price, Financing, EMI Amount, Loan Terms, Value for Money, and Maintenance Cost are all rated extremely high (averaging above 4.5). This confirms that economic factors are overwhelmingly the most critical considerations for this demographic, particularly for rural farmers where finance is even more vital. B3_Availed_Subsidy: Assumed Data: