Agile auditing for financial services

1 like•874 views

The document discusses the concept of agile auditing, emphasizing the need for financial services organizations to adapt audit plans to address emerging risks more effectively. It outlines the benefits of a more flexible approach to audit planning and execution, including shorter audit cycles and real-time risk assessments. Key strategies for implementing agile auditing include using audit technology to streamline processes and engaging regularly with risk and compliance functions.

Agile auditing for financial services

- 1. 9-7-2019 1 Agile Auditing Rethinking the Audit Plan for Financial Services Organizations Steven Zapolski MAcc, CIA Senior Market Development Consultant About Jim Kaplan, CIA, CFE President and Founder of AuditNet®, the global resource for auditors (available on iOS, Android and Windows devices) Auditor, Web Site Guru, Internet for Auditors Pioneer IIA Bradford Cadmus Memorial Award Recipient Local Government Auditor’s Lifetime Award Author of “The Auditor’s Guide to Internet Resources” 2nd Edition Page 2 1 2

- 2. 9-7-2019 2 ABOUT AUDITNET® LLC • AuditNet®, the global resource for auditors, serves the global audit community as the primary resource for Web-based auditing content. As the first online audit portal, AuditNet® has been at the forefront of websites dedicated to promoting the use of audit technology. • Available on the Web, iPad, iPhone, Windows and Android devices and features: • Over 3,000 Reusable Templates, Audit Programs, Questionnaires, and Control Matrices • Webinars focusing on fraud, data analytics, IT audit, and internal audit with free CPE for subscribers and site license users. • Audit guides, manuals, and books on audit basics and using audit technology • LinkedIn Networking Groups • Monthly Newsletters with Expert Guest Columnists • Surveys on timely topics for internal auditors Introductions Page 3 HOUSEKEEPING This webinar and its material are the property of AuditNet® and its Webinar partners. Unauthorized usage or recording of this webinar or any of its material is strictly forbidden. • If you logged in with another individual’s confirmation email you will not receive CPE as the confirmation login is linked to a specific individual • This Webinar is not eligible for viewing in a group setting. You must be logged in with your unique join link. • We are recording the webinar and you will be provided access to that recording after the webinar. Downloading or otherwise duplicating the webinar recording is expressly prohibited. • If you meet the criteria for earning CPE you will receive a link via email to download your certificate. The official email for CPE will be issued via [email protected] and it is important to white list this address. It is from this email that your CPE credit will be sent. There may be a processing fee to have your CPE credit regenerated if you did not receive the first mailing. • Submit questions via the chat box on your screen and we will answer them either during or at the conclusion. • You must answer the survey questions after the Webinar or before downloading your certificate. 3 4

- 3. 9-7-2019 3 IMPORTANT INFORMATION REGARDING CPE! • ATTENDEES - If you attend the entire Webinar and meet the criteria for CPE you will receive an email with the link to download your CPE certificate. The official email for CPE will be issued via [email protected] and it is important to white list this address. It is from this email that your CPE credit will be sent. There may be a processing fee to have your CPE credit regenerated after the initial distribution. • We cannot manually generate a CPE certificate as these are handled by our 3rd party provider. We highly recommend that you work with your IT department to identify and correct any email delivery issues prior to attending the Webinar. Issues would include blocks or spam filters in your email system or a firewall that will redirect or not allow delivery of this email from Gensend.io • You must opt in for our mailing list. If you indicate you do not want to receive our emails your registration will be cancelled and you will not be able to attend the Webinar. • We are not responsible for any connection, audio or other computer related issues. You must have pop-ups enabled on you computer otherwise you will not be able to answer the polling questions which occur approximately every 20 minutes. We suggest that if you have any pressing issues to see to that you do so immediately after a polling question. The views expressed by the presenters do not necessarily represent the views, positions, or opinions of AuditNet® LLC. These materials, and the oral presentation accompanying them, are for educational purposes only and do not constitute accounting or legal advice or create an accountant-client relationship. While AuditNet® makes every effort to ensure information is accurate and complete, AuditNet® makes no representations, guarantees, or warranties as to the accuracy or completeness of the information provided via this presentation. AuditNet® specifically disclaims all liability for any claims or damages that may result from the information contained in this presentation, including any websites maintained by third parties and linked to the AuditNet® website. Any mention of commercial products is for information only; it does not imply recommendation or endorsement by AuditNet® LLC 5 6

- 4. 9-7-2019 4 Overview Internal audit is a profession that struggles against the stereotypes of our past. When we explore our current processes and methodologies, one area that needs attention is executing the audit plan. If our focus is setting a plan in motion and tracking to completion each year, then we are not able to react to changes in our organizations. Financial services organizations face additional challenges in trying to balance emerging risks with the requirements of the regulatory authorities. By embracing the concept of agile auditing, we will be able to adjust more quickly and act as a more relevant partner to our organizations. Agile Auditing Learning Objectives Understand the concept of agile auditing Identify areas for applying agile techniques Discuss a strategy for successfully implementing agile audit Learn how TeamMate supports agile auditing Agile Auditing 7 8

- 5. 9-7-2019 5 POLLING QUESTION 1 Understanding the Concept 9 10

- 6. 9-7-2019 6 Process Review Pick applications to review Submit list for approval Review application every third year Cut scope due to timing Report results Annual risk assessment Develop 1- 3 year audit plan Present for approval Cut scope due to timing Report results Agile Auditing Application Audit Audit Planning Understanding Agile Processes Originated from a software development technique Alternative to traditional project management Agile approaches help teams respond to unpredictability Agile Auditing 11 12

- 7. 9-7-2019 7 Audit Planning Our audit planning process is antiquated and is in desperate need of updating Audit planning should be nimble We should tackle emerging risk areas Audit departments should add value! Agile Auditing POLLING QUESTION 2 13 14

- 8. 9-7-2019 8 Audit Planning 57% conduct an annual audit plan with some periodic updates 40% are updating their audit plans either monthly or as audit work is completed 28% anticipate moving to a rolling audit plan over the next two years 5% are already conducting totally rolling audits Agile Auditing Applying Agile Techniques 15 16

- 9. 9-7-2019 9 Agile Audit Process Diagram Risk Assessment Plan Development Plan Execution Reporting Agile Auditing Audit Planning Audit Execution Review Reporting Milestone Planning Milestone Execution Milestone Review Milestone Reporting Quarterly QuarterlyQuarterlyQuarterly Defining an Agile Audit Planning Process Opt for a shorter plan, no more than the next quarter Quarterly plan should go through testing, review, and presentation within the allotted time By the quarter end, start planning the next quarter, considering the outcome of prior testing and emerging risks Assessment • Perform risk assessment PlanPlan Development • Develop the risk based plan • Communicate the plan to the audit committee Execution • Execute the audit plan Reporting • Report results Agile Auditing 17 18

- 10. 9-7-2019 10 Defining an Agile Audit Execution Process Overall audit process is the same Fieldwork is segmented into smaller milestones Fieldwork milestones contain: Milestone planning Milestone execution Milestone review Milestone reporting Planning • Overall audit planning Fieldwork • Milestone planning, execution, review and reporting Review • Overall quality review Reporting • Overall audit reporting Agile Auditing Successful Implementation of Agile Audit 19 20

- 11. 9-7-2019 11 Applying Agile Techniques More frequent risk assessment Shorter audit plan Structure fieldwork into shorter activities Audit results feed back into the next quarterly assessment Audit software provides real time review and automated reporting Audit Software Software should support continuous risk assessment with shorter audit plan periods Score risk in the assessment to build plan (can be quarterly or real time) Risks carry to the audit and updated scores feed back into the assessment in real time Software should include real time test review Software should provide historical insights, like showing past audit issues in the risk assessment Reporting should be automated or produced quickly for frequent management updates Agile Auditing 21 22

- 12. 9-7-2019 12 POLLING QUESTION 3 Traits of Successful Agile Departments Maintain an Internal Audit Strategic Plan Clearly link risk to business objectives Assess risk more frequently Leverage consistent risk terms and definitions as other risk functions Meet regularly with other risk and compliance functions Promote unified messaging, understanding of risk drivers Leverage industry and professional thought leadership sources Perform formal skills assessments with a longer-term view of needs and actionable development plans Define and track learning roadmaps and continuing education requirements Agile Auditing 23 24

- 13. 9-7-2019 13 Practical Application More frequent risk assessment Create audit from the assessment and include the risks from the assessment The risks are now in the audit and can be modified wih results flowing back to the assessment Agile Auditing 25 26

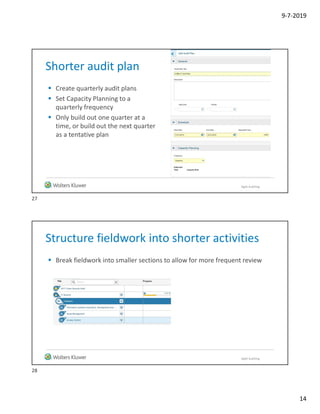

- 14. 9-7-2019 14 Shorter audit plan Create quarterly audit plans Set Capacity Planning to a quarterly frequency Only build out one quarter at a time, or build out the next quarter as a tentative plan Agile Auditing Structure fieldwork into shorter activities Break fieldwork into smaller sections to allow for more frequent review Agile Auditing 27 28

- 15. 9-7-2019 15 Audit results feed back to the next assessment Roll quarterly assessments forward and include Scores in the settings Updated scores and Historical Insights feed back into your assessment Agile Auditing Real time review and automated reporting Don’t wait until the end of the audit to start reviewing Set your dashboard and notifications to alert you when individual tests are ready for review Reports can be configured to pull specific data and to automatically run Agile Auditing 29 30

- 16. 9-7-2019 16 POLLING QUESTION 4 Agile Auditing Rethinking the Audit Plan for Financial Services Organizations Steven Zapolski Macc, CIA Senior Market Development Consultant 31 32