Dodd-Frank Compliance and Technology Summer Meeting 2013

- 2. Presented by Daniel G. Viola Regulatory Defense and Compliance Sadis & Goldberg, LLP

- 3. Dodd-Frank • Dodd-Frank Wall Street Reform and Consumer Protection Act was signed into law on July 21, 2010. • Purpose: Create a sound economic foundation to grow jobs, protect consumers, rein in Wall Street, end bailouts, end “too big to fail” corporations and prevent another financial crisis. • Dodd-Frank Act represents a significant change in the American financial regulatory environment affecting all Federal financial regulatory agencies and affecting almost every aspect of the nation’s financial services industry. • The Dodd-Frank Act provides for new regulations affecting U.S. banks, securities, derivatives, executive compensation, consumer protection and corporate governance.

- 4. Dodd-Frank • It contains approximately 1,500 provisions, including about 398 rule-making requirements. 279 deadlines for finalized rules passed as of June 3, 2013. • Title IV and IX • Title IV – Regulation of Advisers to Hedge Funds and Others or “Private Fund Investment Advisers RegistrationAct of 2010” • Calls for Securities and ExchangeCommission (SEC) registration, reporting and record keeping obligations for investment advisers to “private funds” and limits the ability of these advisers to exclude information in reporting to the various Federal government agencies.

- 5. Dodd-Frank • Title IX – Investor Protections and Improvements to the Regulation of Securities or “Investor Protections and Improvements to the Regulation of Securities” • Revises the powers and structure for the SEC, credit rating organizations, and the relationships between customers and broker-dealers or investment advisers.

- 6. Annual Review of Compliance Procedures Books and Records Financials Registration • ADV,U4, Firm, IARs, ADV Delivery Fees Advertising • Ads,Websites, BusinessCards, Seminars, RFPs, Pitch books Privacy Policies Supervisory/Compliance • Supervisory Procedures,Compliance Procedures, Policies,Code of Ethics Investment Activities • Adherence to Investment Policy, Fairness, Conflicts Trading & Brokerage Practices Performance Reporting Custody Solicitors Pooled Investment Vehicles (Hedge Funds) Insider Trading Proxy Voting BCP AML Unethical Business Practices • Section 206 • Unsuitable Recommendations • Contracts • Unauthorized trades • Excessive Fees • Borrowing from client • Valuation

- 7. Best Practices for Investment Advisers • Review and revise Form ADV and disclosure brochure annually to reflect current and accurate information. • Review and update all contracts. • Prepare and maintain all required records, including financial records. • Prepare and maintain client profiles. • Prepare a written compliance and supervisory procedures manual relevant to the type of business. • Prepare and distribute a privacy policy initially and annually.

- 8. Best Practices for Investment Advisers • Keep accurate financials. File timely with the jurisdiction. Maintain surety bond, if required • Calculate and document fees correctly in accordance with contracts and ADV. • Review all advertisements, including website and performance advertising, for accuracy. • Implement appropriate custody safeguards, if applicable. • Review solicitor agreements, disclosure, and delivery procedures.

- 9. SEC Comments on Broker-Dealer Registration by Private Fund Advisers Davis W. Blass, Chief Counsel, Division of Trading and Markets, SEC, recently gave a speech before the American Bar Association on April 5, 2013. The topic: whether and when investment advisors to private funds are required to register with the SEC as broker-dealers. • With regard to soliciting and retaining investors, a dedicated sales force of employees carrying out a marketing function “may strongly indicate that they are in the business of effecting transactions in the private fund.”

- 10. SEC Comments on Broker-Dealer Registration by Private Fund Advisers • If employees who solicit investors have no other duties, or if they spend the great majority of their time carrying out the investors solicitation function, then the adviser might be a broker-dealer. • Compensating employees who solicit investors in any way (bonuses, etc.) that is linked to successfully investments may indicate broker- dealer status. • If a private equity fund executing a leveraged buyout strategy, collects fees other than advisory fees that are linked to an acquisition or disposition – then the transaction based compensation threshold may be triggered.

- 11. SEC Comments on Broker-Dealer Registration by Private Fund Advisers He also addressed three strands of push-back the SEC has received from private fund advisers seeking to avoid broker-dealer registration • Advisers are not engaging in broker-dealer activity when the transaction-based payments offset or reduce the amount of the advisory fee. In this instance the transaction-based compensation is merely another way of paying the advisory fee.

- 12. SEC Comments on Broker-Dealer Registration by Private Fund Advisers • When the general partner of the fund is also the adviser to the fund or an affiliate of the adviser to the fund, then the general partner should be viewed as the same person as the funds such that the advisers is not engaging in securities transactions “for the account of others.” Mr. Blass did not see this as plausible, he notes that if the general partner and the fund are the same person, then there is no need to pay the fee to any person other than the fund.

- 13. SEC Comments on Broker-Dealer Registration by Private Fund Advisers • The SEC should not spend it’s time taking on registration of private fund advisers as broker-dealers without an underlying policy objective. Mr. Blass sees the situation as dependent on the activities of the private fund advisers, rather than the SEC. If private fund advisers are not prepared to register as broker-dealers, then they should avoid in engaging in broker-dealer activity.

- 14. Presented by Sean Owens Consultant, Capital Markets Research and Consulting Woodbine Associates

- 16. Fragmentation • Multiple SEFs/DCMs for each product and asset class (overcapacity likely to abate over time) • MultipleCCPs for each product and asset class (will further segregate liquidity on each platform) Connectivity • SEFs via API or web interface, direct or sponsored access • Aggregation platforms (dealer or third-party, ex: SwapsHub) and OMS systems • Middleware needs for trade affirmation with CCP, block allocations Market Structure Related Issues Woodbine Associates, Inc.

- 17. Relationships • FCMs are key relationship - multiple relationships needed • CCPs, Prime Brokers, Outsourced providers Credit line management • Initial credit lines and intra-day updates will determine trading limits Post-trade margin and collateral management • Intra-day calls, IM acceptable collateral Market Structure Related Issues Woodbine Associates, Inc.

- 18. Incremental costs will impact pricing and trading • IM, capital, netting, clearing cost • Vary by CCP & FCM Product selection • Swap, future, cash, ETF, unwind/novation Liquidity • Vary by venue, product, destination CCP Pre-tradeAnalysis / Post-trade Processing are Key Woodbine Associates, Inc.

- 19. Credit allocation • Intra-day management of credit, risk and margin Risk position with FCM , CCP and dealer Dealer risk position (outright market risk and cleared position with CCP) Collateral and margin management Pre-tradeAnalysis / Post-trade Processing are Key Woodbine Associates, Inc.

- 20. Integration across functional areas (operations, risk management and trading) Real time capabilities • Intra-day data and capabilities • Positions, risk, margin, credit, collateral Scalable systems and STP for increased ticket volume Middleware for connectivity, communications, workflow management Capabilities &Technology Needed Woodbine Associates, Inc.

- 21. Internally manage or mirror outsourced solutions for collateral management and credit allocation Pre-trade: • Analytics, credit allocation, aggregation Post-trade: • Collateral and margin management, automated processing Funding, securities financing and liquidity management Capabilities &Technology Needed Woodbine Associates, Inc.

- 24. FederalAgencies and Financial Firms • SEC • FINRA • Treasury • FDIC • FIO* • OFR* • BCFP* • Federal Reserve • CFTC • GAO • OCC * Formed by The Dodd Frank Act • Hedge Funds • Asset Managers • RIA’s • Prime Brokers • Broker/Dealers • Banks • InsuranceCompanies • Insurance Brokers • CommodityTraders

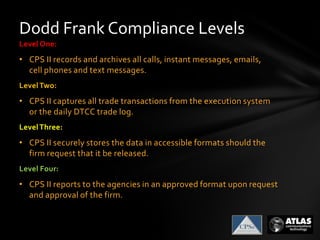

- 25. Dodd Frank Compliance Levels Level One: • CPS II records and archives all calls, instant messages, emails, cell phones and text messages. LevelTwo: • CPS II captures all trade transactions from the execution system or the daily DTCC trade log. LevelThree: • CPS II securely stores the data in accessible formats should the firm request that it be released. Level Four: • CPS II reports to the agencies in an approved format upon request and approval of the firm.

- 26. Compliance Processing Compliance Discovery Discovery provides an assessment of the network, technology and applications at the start of an engagement.The status of compliance is documented throughout the process. Compliance Planning Planning covers the design and architecture of a solution that meets compliance requirements.Timeframes and milestones are developed by CPS II and the company. Compliance Processing Processing can include any customized work necessary to do the actual storing, archiving, auditing and reporting of transactions to the government agencies.

- 27. Dodd Frank Critical Success Factors • Learn the Dodd Frank requirements • Identify government agency reporting requirements • Identify mandatory dates for compliance • Initiate a compliance discovery process • Set a date for completing compliance preparation • Determine budget requirements • Get senior management approval • Apply for necessary agency extensions

- 28. Presented by Phil Hunter, Chairman CPSII

- 29. Dodd-Frank’s particulars are still in flux, but it can’t be ignored. All financial institutions fall under its provisions. Compliance is impossible without appropriate technology • Technology budgets will increase by 35% • Data collection will require new systems architecture • Small / medium financial firms will struggle • New technology solutions will be needed Penalties for non-compliance are severe • Maximum jail terms • Maximum fine of $25 Million • CEOs and CCOs are held responsible Compliance resources will be limited as deadlines approach • Mandatory compliance by 2015 • Applications for three 1-year extensions are allowed • Technology providers will contract early with premiere firms • Firms that are unprepared will not be excused Consequences and Actions: Dodd-Frank is the Law of the Land

- 31. • Be sure to sign up for The Dodd-Frank Compliance andTechnology Fall Meeting in September • Features an expanded, more in-depth agenda • Speakers will include Congressman Jim Himes, co-author of the Dodd-FrankWall Street Reform andConsumer Protection Act • Call 1-855-Dodd Frank (1-855-363-3372) for any questions, or if you wish to talk to one of our presenters today to talk about taking the next steps towards Dodd-Frank compliance Sign up for the Fall Meeting