Capital Budgeting decision-making in telecom sector using real option analysis

Download as PPTX, PDF6 likes2,015 views

Master thesis presentation - Dimitar Serafimov 20/05/2013 Follow FELU Macedonia on Facebook: https://www.facebook.com/FELUMacedonia Contact us: [email protected] 070-338-570

![Quantitative Different parameterizations

0,00

0,50

1,00

1,50

2,00

2,50

3,00

3,50

4,00

4,50

5,00

1 2 5 10

Project value

[millionEUR]

number of steps n

BS

CRR

RB

Trigerogis

Hull

Haahtela

=30,9%

Option to defer the investment for one year](https://image.slidesharecdn.com/dimitarserafimov-presentation-130526113523-phpapp02/85/Capital-Budgeting-decision-making-in-telecom-sector-using-real-option-analysis-28-320.jpg)

![Quantitative Different parameterizations

-1

0

1

2

3

4

5

6

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Project value

[million €]

Volatility

BS

CRR

Trigeorgis

RB

Hull

Haahtela

0

0.5

1

1.5

2

5% 10% 15% 20%

Option to Differ the Investment (Double Step) With Different

Parameterizations in Relation to Volatility](https://image.slidesharecdn.com/dimitarserafimov-presentation-130526113523-phpapp02/85/Capital-Budgeting-decision-making-in-telecom-sector-using-real-option-analysis-29-320.jpg)

Ad

More Related Content

What's hot (20)

Viewers also liked (20)

Ad

Similar to Capital Budgeting decision-making in telecom sector using real option analysis (20)

Ad

More from Faculty of Economics Ljubljana in Skopje (7)

Recently uploaded (20)

Capital Budgeting decision-making in telecom sector using real option analysis

- 1. CAPITAL BUDGETING DECISION-MAKING IN TELECOM SECTOR USING REAL OPTION ANALYSIS Master’s Thesis presentation Mentor: Prof. Aleš Berk Candidate: Dimitar Serafimov Ljubljana, May, 2013

- 2. Introduction Implementing risks techniques in capital budgeting decisions is becoming increasingly more important, as: • Recourses are getting scarcer; • Competition is becoming more intense; • The expenditures are large; • The uncertainty related to the advanced technology is higher • Regulators are increasing the requirements / constrains for the operators with significant market power • Business models are changing, etc. The need for additional information related to uncertainty is of a major importance for decision makers, as decisions made today will definitely impact the future

- 3. Problem Description The workhorse in capital decision making – Discounted Cash Flow analysis or NPV Primarily used and invented for evaluating financial assets, which are passive by their nature In contrast, Real assets are dynamic - management has options to influence the project and thus alter the outcome of the investment. The mechanic of DCF analysis involves forecasting the expected incremental net cash flows of the project and discounting them back to today with discount factor, usually the WACC.

- 4. Problem Description cont‟d. There are several problem in this technique: • Beta is an estimate from past market performance, while its application throughout WACC is intended for the future project performance • The correlation between the asset and the market is diluting the discount factor especially with low correlated, but highly volatile asset because beta is measure of both the correlation and the volatility • The third is application of constant discount rate to non constant future cash flows or non constant uncertainty • Can not accommodate the managements„ flexibility

- 5. Problem Description cont‟d. Management has the opportunity alter the passive operating strategy, hence modify the project‟s outcome This opportunity to take action is in fact an option – a right, but not an obligation. As the underlying asset is real, Stewart Myers has coined the term Real Options as to distinguish them from Financial Options

- 6. The Thesis Managements‟ flexibility brings additional value over and above the passive operating strategy – options are valuable expanded NPV= passive NPV + value of the option Not considering the embedded options leads to underinvestment strategies Thus the model for valuing future opportunities has to be amended in order to reflect its true potential.

- 7. The Research 1.Qualitative review of the related literature • Theoretical background • Specific application of ROA, with focus on the Telecommunication sector 2. Quantitative application of the models and techniques on a particular project - FTTH • Several types of Options • Option to differ the investment • Option to contract the investment • Growth option

- 8. The Research cont‟d. • Different calculation methodologies • Closed form solution • Lattices • Simulation • Application of five different parameterizations for approximation of the diffusion process

- 9. Qualitative - application of ROA Most extensive application of ROA in • Natural resources utilization – Oil and Mining sector • Pharmaceutical, specifically R & D Due to: • Capital intensity • Availability of traded assets – option • High uncertainty Application of ROA in Telecommunication sector: • With the beginning of deregulation of the sector and regulation Telecom operators with significant market power • Mostly for justification of costs and allowable investment base • Only recently for application of new technologies

- 10. Qualitative - Required assumptions - cont‟d Conditions for application of Financial assets valuation tools to valuation of Real assets ROA is considered as an extension to the DCF/NPV analysis, not as a substitute hence: • average rational investor is a risk averse • prefers more to less wealth All option pricing models are based on the concept of riskless hedge and no arbitrage opportunities hence: • The market is complete - any state of the world can be replicated by some combination of the existing securities.

- 11. Qualitative - Required assumptions - cont‟d • Complete market for Binomial - there are at least two linearly independent securities: • a twin security and a • riskless bond • Black - Scholes assumptions: • There are no transaction costs; • The investor may borrow any fraction of the purchase price at the short term risk free interest rate; • Short selling is permitted; • The call option can be exercised only on its expiration date; • Trading of securities takes place continuously; • The stock price (underlying asset) follows a geometric Brownian motion with constant drift and volatility, and • The underlying security does not pay dividends.

- 12. Qualitative - Required assumptions - cont‟d The diffusion process – changes of the underlying asset value • Geometric Brownian motion - continuous stochastic process, with small random movements • Pure jump process, each successive asset price is almost the same as the previous price, but only occasionally with low probability of occurrence significantly different • Combination • It has to correspond to the actual asset being analyzed

- 13. Qualitative - Required assumptions - cont‟d Incomplete market - partially solved by so called the integrated – two risks type approach The additional assumptions / conditions for this so called “Partially complete market” are: • Securities depend only on market states, • The market is complete with respect to the market uncertainties and • Private events convey no information about future market events. Disaggregation of uncertainties Drawback: Private and Market uncertainties might be correlated

- 14. Qualitative – Option valuation techniques Categorized in three broader valuation techniques: 1. Partial differential equations - Black – Scholes as a closed – form solution - Analytical approximations - Numerical methods, such as finite difference method 2. Simulations - Monte Carlo 3. Lattices - Binomial - Trinomial - Quadrinomial - Multinomial

- 15. Options Strike or Exercise price Price of underlying asset Net Payoff Out-of-the-money In-the-money At-the-money Strike or Exercise price Price of underlying asset Net Payoff In-the-money Out-of-the-money At-the-money Payoff of Call Option Payoff of Put Option

- 16. Qualitative - Option valuation techniques Black – Scholes as a closed – form solution Where C is the value of the call option S0 is the current value of the underlying asset; X is the cost of investing or strike price; r risk free rate of return; T is the time to expiration or validity of the real option; N(d1) and N(d2) are values from normal standard distribution is the volatility r is the risk-free rate 𝐶 = 𝑁 𝑑1 𝑆0 − 𝑁 𝑑2 𝑋𝑒−𝑟𝑇 𝑑1 = 𝑙𝑛 𝑆𝑜 𝑋 + 𝑟 + 𝜎2 2 𝑇 𝜎 𝑇 𝑑2 = 𝑑1 − 𝜎 𝑇 0 0.2 0.4 0.6 0.8 1 1.2 -3.00 -2.50 -2.00 -1.50 -1.00 -0.50 0.00 0.50 1.00 1.50 2.00 2.50 3.00

- 17. Qualitative - Option valuation techniques Simulations is the volatility St and St-1 are the values of the underlying asset at time t and t-1 t is the time increment r is the risk free rate of return is value from normal standard distribution with mean zero and a variance of 1.0. 𝑆𝑡 = 𝑆𝑡−1 + 𝑆𝑡−1(𝑟 𝛿𝑡 + 𝜎𝜀 𝛿𝑡) 𝑚𝑎𝑥 𝑆𝑡 − 𝑋, 0 -1.50 -1.00 -0.50 0.00 0.50 1.00 1.50 0 0.2 0.4 0.6 0.8 1 1.2Time Wiener Process Z w/o Drift +STDEV(Z)= +SQRT(T) -STDEV(Z)=- SQRT(T)

- 18. Qualitative - Option valuation techniques Lattices – Binomial 𝑢 = 𝑒(𝜎 𝛿𝑡) 𝑑 = 𝑒−(𝜎 𝛿𝑡) 𝑝 = 𝑒(𝑟𝛿𝑡 ) − 𝑑 𝑢 − 𝑑 𝛿𝑡 = 𝑇 𝑛 𝐶 = 𝑛! 𝑗! 𝑛 − 𝑗 ! 𝑛 𝑗=0 𝑝 𝑗 1 − 𝑝 𝑛−𝑗 𝑚𝑎𝑥 0, 𝑢 𝑗 𝑑 𝑛−𝑗 𝑆0 − 𝑋 𝑒 𝑟𝛿𝑡 𝑝 = 𝑒(𝑟−𝑦)𝛿𝑡 −𝑑 𝑢−𝑑 S0 S0u S0d S0u2 S0ud S0d2 S0u3 1/8 S0u2d 3/8 S0du2 3/8 S0d3 1/8 0 1 2 3 Time increments

- 19. Qualitative Option valuation techniques Lattices – Qudrinomial S0 S0u1u2 S0u1d2 S0u12u2d2 S0u12u22 S0u1u2d1d2 S0u1d1u22 S0u12d22 S0u12u2d2 S0u1d1d22 S0u1u2d1d2 S0d1u2 S0d1d2 S0u1u2d1d2 S0u1d1u22 S0d12u2d2 S0d12u22 S0u1d1d22 S0u1d1u2d2 S0d12d22 S0 d12u2d2

- 20. Qualitative research – Integration of DTA S0 S0 u S0 udx1 S0 u 2 x1 S0 udy1 S0 u 2 y1 S0 d S0 d 2 x1 S0 udx1 S0 d 2 y1 S0 udy1 p p1 (1-p) p1 p(1-p1 ) (1-p)(1-p1 ) p p1 (1-p) p1 p(1-p1 ) (1-p)(1-p1 ) Where x1 and y1 are asset correction factors

- 21. Quantitative FTTH Fiber optical network

- 22. Quantitative - FTTH DCF FTTH DCF Analysis Year 0 1 2 3 4 5 6 FTTH Residential & Business Fast Internet customers - new sales100% 8700 20000 28000 44000 10000 6000 WS participation in total sales 10% 20% 20% 20% 20% Distribution of FTTH Fast Internet customers Residential 59% 50% 50% 50% 50% 50% Residential +HD TV 32% 41% 41% 41% 41% 41% Business 10% 10% 10% 10% 10% 10% FTTH incremental monthly fee Residential monthly fee - FTTH Fast Internet € 4,5 € 4,2 € 3,9 € 3,9 € 3,9 € 3,9 Residential monthly fee - FTTH Fast Internet and HD TV € 10,0 € 9,3 € 8,6 € 8,6 € 8,6 € 8,6 Business monthly fee - FTTH Fast Internet € 11,0 € 10,2 € 9,5 € 9,5 € 9,5 € 9,5 Average Rate Per User (ARPU) € 24,0 € 24,0 € 23,0 € 22,0 € 22,0 € 22,0 Revenues Residential monthly fee - FTTH Fast Internet € 137.417 € 464.861 € 781.585 € 1.149.390 € 1.126.402 € 367.805 Residential monthly fee - FTTH Fast Internet and HD TV € 164.430 € 845.203 € 1.421.064 € 2.089.800 € 2.048.004 € 668.736 Business monthly fee - FTTH Fast Internet € 57.420 € 229.561 € 385.968 € 567.600 € 556.248 € 181.632 ARPU revenues € 1.252.800 € 5.385.600 € 11.785.200 € 20.776.800 € 27.904.800 € 30.808.800 Total Revenues € 1.612.067 € 6.925.225 € 14.373.817 € 24.583.590 € 31.635.454 € 32.026.973 Cost margin as % of sales 50% 40% 39% 38% 37% 36% Total operating costs € 806.033 € 2.770.090 € 5.605.789 € 9.341.764 € 11.705.118 € 11.529.710 EBITDA € 806.033 € 4.155.135 € 8.768.028 € 15.241.826 € 19.930.336 € 20.497.263 Depreciation € 1.089.866 € 2.858.296 € 4.950.663 € 6.670.126 € 6.399.402 € 5.556.420 EBIT -€ 283.833 € 1.296.839 € 3.817.366 € 8.571.700 € 13.530.934 € 14.940.842 Tax @ 10% 10% € 0 € 129.684 € 381.737 € 857.170 € 1.353.093 € 1.494.084 Net income -€ 283.833 € 1.167.155 € 3.435.629 € 7.714.530 € 12.177.841 € 13.446.758 Operating cash flow (CF) € 806.033 € 4.025.451 € 8.386.292 € 14.384.656 € 18.577.243 € 19.003.178 Present value (PV) CF @ 13.6% WACC € 709.536 € 3.119.305 € 5.720.513 € 8.637.462 € 9.819.505 € 8.842.117 CF PV cumulative € 709.536 € 3.828.842 € 9.549.355 € 18.186.817 € 28.006.322 € 36.848.439 Capital expenditures (CAPEX) € 7.933.494 € 10.055.587 € 12.351.415 € 8.046.443 € 3.283.084 € 2.236.696 € 0 CAPEX PV @ 13.6% WACC € 7.933.494 € 8.851.749 € 9.571.060 € 5.488.693 € 1.971.373 € 1.182.267 € 0 Total CAPEX PV € 34.998.635 CF PV cummulative - CAPEX PV cummulative -€ 34.998.635 -€ 34.289.099 -€ 31.169.793 -€ 25.449.280 -€ 16.811.818 -€ 6.992.313 € 1.849.804 Net Present Value (NPV) as of Y6 € 1.849.804 Discounted payback period (Years) 5,79 Internal rate of return (IRR) 15,79%

- 23. Quantitative FTTH input estimates Method annual volatility in % Implied volatility B-S model 27.47 Logarithmic CF from project returns 29.70 Logarithmic stock price returns 30.91 Standard deviation in firm value1 40.64 Inputs Date Stock price € 8,68 05.03.2012 Dividend € 0,70 Dividend yield 8,06% Call option value 0,9 05.03.2012 Exercise price 8 21.06.2013 Risk - free rate (annual) dis. 0,13% Risk - free rate (annual) con. 0,13% Black Scholes calculator INPUTS OUTPUTS Standard deviation (annual) 27,47% d1 0,088264 Maturity (in years) 1,30 d2 -0,22446 Risk - free rate (annual) 0,13% N(d1) 0,535167 Stock price € 8,68 N(d2) 0,4112 Exercise price € 8,00 B-S call 0,900052 Divident yield (annual) 8% B-S put 1,068341 12 23.01.2012-27.01.2012 511 -0,004 8,50322E-07 13 16.01.2012-20.01.2012 513 -0,004 8,78585E-07 14 09.01.2012-13.01.2012 515 -0,002 8,34354E-06 15 03.01.2012-05.01.2012 516 -0,008 8,37328E-06 16 26.12.2011-29.12.2011 520 0,000 2,33133E-05 17 19.12.2011-23.12.2011 520 -0,010 2,24777E-05 18 12.12.2011-16.12.2011 525 0,006 0,000111494 19 05.12.2011-09.12.2011 522 -0,015 0,000107766 20 28.11.2011-02.12.2011 530 0,019 0,000570091 21 21.11.2011-25.11.2011 520 0,016 0,000413413 22 14.11.2011-18.11.2011 512 0,010 0,000214388 23 07.11.2011-11.11.2011 507 0,002 4,6277E-05 24 31.10.2011-04.11.2011 506 0,002 4,63301E-05 25 24.10.2011-28.10.2011 505 0,000 2,33133E-05 26 17.10.2011-21.10.2011 505 0,000 2,33133E-05 27 10.10.2011-14.10.2011 505 0,000 2,33133E-05 28 03.10.2011-07.10.2011 505 -0,002 8,12332E-06 29 26.09.2011-30.09.2011 506 -0,004 7,80759E-07 30 19.09.2011-23.09.2011 508 0,006 0,000115593 31 12.09.2011-16.09.2011 505 -0,010 2,52397E-05 32 05.09.2011-09.09.2011 510 -0,004 8,36282E-07 33 29.08.2011-02.09.2011 512 0,004 7,64275E-05 34 22.08.2011-26.08.2011 510 0,016 0,000425968 35 15.08.2011-19.08.2011 502 -0,006 1,27673E-06 36 08.08.2011-12.08.2011 505 0,006 0,000116353 37 01.08.2011-05.08.2011 502 0,002 4,65452E-05 38 25.07.2011-29.07.2011 501 0,000 2,33133E-05 39 18.07.2011-22.07.2011 501 0,000 2,33133E-05 40 11.07.2011-15.07.2011 501 -0,004 7,12868E-07 41 04.07.2011-08.07.2011 503 0,006 0,000116866 42 27.06.2011-01.07.2011 500 0,000 2,33133E-05 43 20.06.2011-24.06.2011 500 -0,002 8,01106E-06 44 13.06.2011-17.06.2011 501 -0,002 8,03363E-06 45 06.06.2011-09.06.2011 502 -0,006 1,27673E-06 46 30.05.2011-03.06.2011 505 0,012 0,000281592 47 23.05.2011-27.05.2011 499 0,018 0,000530339 48 16.05.2011-20.05.2011 490 -0,002 7,78213E-06 49 09.05.2011-13.05.2011 491 -0,008 1,07929E-05 50 03.05.2011-06.05.2011 495 0,031 0,001267363 51 26.04.2011-29.04.2011 480 0,043 0,002245622 52 18.04.2011-21.04.2011 460 -0,264 0,067188126 53 11.04.2011-15.04.2011 599 / / Average -0,005 Total 0,101483 4,46% 30,91% Weekly volatility Yearly volatility

- 24. Quantitative – Option to defer Step 0 1 Factors u= 1,362 d= 0,734 p= 0,524 44,19 Sou e 32,44 8,69 So k 4,28 23,81 Sod k 0,00 Related decision e - exercise the option k- keep the option 𝑉 = 𝑝 𝑚𝑎𝑥 0, 𝑢 𝑆0 − 𝑋 + 1 − 𝑝 𝑚𝑎𝑥 0, 𝑑 𝑆0 − 𝑋 𝑒 𝑟𝛿𝑡 The input parameters (in million €) are as follows: Stock price (PV of the cash flow as of now) S0= 32.4 Exercise price (PV of the investment as of Year 1) X=35.5 Standard deviation (annual volatility of the asset) =30.9% Risk-free rate (continuous) rf=6.1% Time to expiration T=1 Year Time step t=1 BS yields 3.58 million € Simulation yields 3.98 million €

- 25. Quantitative – Option to defer Step 0 1 2 3 4 5 Factors 64,75 u= 1,148 Sou5 e d= 0,871 56,39 29,25 p= 0,510 Sou4 k 49,11 21,32 49,11 Sou3 k Sou4 d e 14,47 42,77 13,61 42,77 Sou3 d k Sou2 k 37 7,70 37,25 37,25 9,37 Sou2 d k Sou3 d2 e Sou k 4,30 1,75 32,44 5,87 32,44 32,44 So k Soud k Sou2 d2 k 3,59 28,25 2,38 0,88 Sod k 28,25 28,25 1,31 24,60 Soud2 k Sou2 d3 k Sod2 k 0,44 24,60 0,00 0 Soud3 k Related decision 21 0,00 21,43 e - exercise the option Sod3 k Soud4 k k- keep the option 0 19 0,00 Sod4 k 0,00 16,25 Sod5 k 0,00

- 26. Quantitative Method Annual volatility in Binomial 1 step Binomial 5 steps B-S model Standard deviation in firm value 40,64 5,90 4,95 4,84 Logarithmic stock price returns 30,91 4,28 3,59 3,58 Logarithmic CF from project returns 29,70 4,07 3,59 3,58 Implied volatility B-S model 27,47 3,69 3,42 3,43 Option value in 1.000.000 EUR The option value is highly sensitive to the time step and the volatility

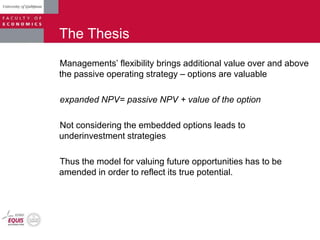

- 27. Quantitative Different parameterizations Trigeorgis 𝜇 = 𝛼 𝜎2 − 1 2 (23) 𝑘 = 𝜎 𝛿𝑡 (24) ℎ = 𝑘2 + (𝑘2 𝜇)2 (25) 𝑝 = 1 2 (1 + 𝑘2 𝜇 ℎ ) (26) 𝜇 = 𝛼 𝜎2 − 1 2 (23) 𝑘 = 𝜎 𝛿𝑡 (24) ℎ = 𝑘2 + (𝑘2 𝜇)2 (25) 𝑝 = 1 2 (1 + 𝑘2 𝜇 ℎ ) (26) 𝑢 = 𝑒 𝑟− 𝜎2 2 𝛿𝑡+𝜎 𝛿𝑡 (27) 𝑑 = 𝑒 𝑟− 𝜎2 2 𝛿𝑡−𝜎 𝛿𝑡 (28) 𝑢𝑑 = 𝑒 2 𝑟− 𝜎2 2 𝛿𝑡 (29) 𝑢 = 𝑒 𝑟− 𝜎2 2 𝛿𝑡+𝜎 𝛿𝑡 (27) 𝑑 = 𝑒 𝑟− 𝜎2 2 𝛿𝑡−𝜎 𝛿𝑡 (28) 𝑢𝑑 = 𝑒 2 𝑟− 𝜎2 2 𝛿𝑡 (29) = r- 𝑢 = 𝑒ℎ , 𝑑 = 𝑒−ℎ 𝑒 𝜎2 𝛿𝑡 − 1𝑢 = 𝑒 𝑒 𝜎2 𝛿𝑡 −1+𝑟𝛿𝑡 𝑑 = 𝑒− 𝑒 𝜎2 𝛿𝑡 −1+𝑟𝛿𝑡 𝑝 = 𝑒 𝑟𝛿𝑡 − 𝑑 𝑢 − 𝑑 Rendelmann – Bartter Hull 𝑝 = 1 2 𝜎 𝛿𝑡 Haahtela

- 28. Quantitative Different parameterizations 0,00 0,50 1,00 1,50 2,00 2,50 3,00 3,50 4,00 4,50 5,00 1 2 5 10 Project value [millionEUR] number of steps n BS CRR RB Trigerogis Hull Haahtela =30,9% Option to defer the investment for one year

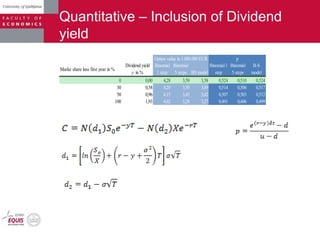

- 29. Quantitative Different parameterizations -1 0 1 2 3 4 5 6 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% Project value [million €] Volatility BS CRR Trigeorgis RB Hull Haahtela 0 0.5 1 1.5 2 5% 10% 15% 20% Option to Differ the Investment (Double Step) With Different Parameterizations in Relation to Volatility

- 30. Quantitative Different parameterizations Method Annual volatility in % BS model in 1.000.000 EUR CRR 1 step RB 1 step Trigerogis 1 step Hull 1 step Haahtela 1 step Standard deviation in firm value 40,64 4,8347 22,07 18,38 21,92 27,93 32,23 Logarithmic stock price returns 30,91 3,5818 19,47 21,86 19,17 23,05 30,92 Logarithmic CF from project returns 29,70 3,4251 18,90 22,27 18,71 22,24 30,83 Implied volatility B-S model 27,47 3,1371 17,55 22,98 17,68 20,46 30,66 Assumed volatility 20,00 2,1707 8,32 25,29 11,57 10,04 30,59 Assumed volatility 10,00 0,8889 -70,76 27,97 -30,71 -70,04 31,59 Assumed volatility 7,00 0,5184 -100,00 26,27 -94,02 -100,00 30,04 17,26 22,16 17,81 20,74 31,04 5,26 2,50 3,83 6,59 0,68Standard deviation of higher (20% and above) volatilities Average of higher (20% and above) volatilities Relative error between different parameterizations and B-S as reference in % Method Annual volatility in % BS model in 1.000.000 EUR CRR 2 steps RB 2 steps Trigerogis 2 steps Hull 2 steps Haahtela 2 steps Standard deviation in firm value 40,64 4,8347 0,00 1,70 -0,13 -2,05 5,89 Logarithmic stock price returns 30,91 3,5818 2,94 1,09 2,72 -4,19 5,54 Logarithmic CF from project returns 29,70 3,4251 3,40 1,04 3,21 -4,56 5,42 Implied volatility B-S model 27,47 3,1371 4,29 0,97 4,22 -5,31 5,16 Assumed volatility 20,00 2,1707 7,69 1,28 8,71 -8,29 3,50 Assumed volatility 10,00 0,8889 -2,82 6,41 12,45 2,56 -4,06 Assumed volatility 7,00 0,5184 -63,46 12,37 -7,57 63,23 -10,99 3,67 1,21 3,75 -4,88 5,10 2,77 0,29 3,21 2,26 0,93 Average of higher (20% and above) volatilities Standard deviation of higher (20% and above) volatilities Relative error between different parameterizations and B-S as reference in % Single step Double step

- 31. Quantitative Different parameterizations Five step Ten step Method Annual volatility in % BS model in 1.000.000 EUR CRR 5 step RB 5 step Trigerogis 5 step Hull 5 step Haahtela 5 step Standard deviation in firm value 40,64 4,8347 2,40 0,56 2,35 3,36 6,09 Logarithmic stock price returns 30,91 3,5818 0,25 1,71 0,16 0,83 5,72 Logarithmic CF from project returns 29,70 3,4251 -0,20 1,82 -0,27 0,35 5,67 Implied volatility B-S model 27,47 3,1371 -1,19 1,99 -1,21 -0,71 5,58 Assumed volatility 20,00 2,1707 -7,28 2,23 -6,98 -7,09 5,09 Assumed volatility 10,00 0,8889 0,18 -1,18 4,89 0,26 1,39 Assumed volatility 7,00 0,5184 -23,24 -8,43 -5,48 -23,17 -6,02 -1,20 1,66 -1,19 -0,65 5,63 Standard deviation of higher (20% and above) volatilities 3,64 0,65 3,49 3,90 0,36 Relative error between different parameterizations and B- S as reference in % Average of higher (20% and above) volatilities Method Annual volatility in % BS model in 1.000.000 EUR CRR 10 step RB 10 step Trigerogis 10 step Hull 10 step Haahtela 10 step Standard deviation in firm value 40,64 4,8347 2,02 2,23 1,99 2,47 -0,16 Logarithmic stock price returns 30,91 3,5818 2,46 2,29 2,42 2,74 0,23 Logarithmic CF from project returns 29,70 3,4251 2,48 2,30 2,45 2,74 0,31 Implied volatility B-S model 27,47 3,1371 2,47 2,32 2,45 2,69 0,47 Assumed volatility 20,00 2,1707 1,20 2,52 1,42 1,33 1,27 Assumed volatility 10,00 0,8889 -0,19 3,38 1,97 -0,16 3,43 Assumed volatility 7,00 0,5184 -11,94 2,53 -6,25 -11,93 3,28 2,13 2,33 2,15 2,39 0,42 Standard deviation of higher (20% and above) volatilities 0,56 0,11 0,45 0,61 0,52 Average of higher (20% and above) volatilities Relative error between different parameterizations and BS as reference in %

- 32. Quantitative – Inclusion of Dividend yield Marke share loss first year in % Dividend yield y in % Binomial 1 step Binomial 5 steps BS model Binomial 1 step Binomial 5 steps B-S model 0 0,00 4,28 3,59 3,58 0,524 0,510 0,524 30 0,58 4,20 3,50 3,49 0,514 0,506 0,517 50 0,96 4,15 3,43 3,42 0,507 0,503 0,512 100 1,93 4,02 3,28 3,27 0,491 0,496 0,499 Option value in 1.000.000 EUR p

- 33. Quantitative – Integration of DTA into ROA S0 S0 u S0 udx1 S0 u 2 x1 S0 udy1 S0 u 2 y1 S0 d S0 d 2 x1 S0 udx1 S0 d 2 y1 S0 udy1 p p1 (1-p) p1 p(1-p1 ) (1-p)(1-p1 ) p p1 (1-p) p1 p(1-p1 ) (1-p)(1-p1 ) Step 0 1 2 Factors u= 1,362 61,25 d= 0,734 Sou2 x1 e p= 0,524 25,75 p1= 0,100 x1= 1,02 33,01 y1= 1,00 Soudx1 k 44,19 0,00 Sou k 12,22 60,19 Sou2 y1 e 24,69 32,44 Soudy1 k 0,00 32,44 So k 6,02 33,01 Soudx1 k 0,00 17,79 Sod2 x1 k 23,81 0,00 Sod k 0,00 32,44 Soudy1 k 0,00 Related decision 17,48 e - exercise the option Sod2 y1 k k- keep the option 0,00

- 34. Quantitative – Option to contract The input parameters (in million €) are as follows: Stock price (PV of the cash flow as of now) S0= 36.85 Savings from contraction cs=16.24 Contraction factor cf = 50% Standard deviation (annual volatility of the asset) =30.9% Risk-free rate (continuous) rf=6.1% Time to expiration T=3 Year Time step t=1 Step 0 1 2 3 Factors u= 1,362 d= 0,734 p= 0,524 93,14 Sou3 k 93,14 68,38 Sou2 k 50 50,19 68,38 Sou2 d k Sou e 50,19 36,85 50,74 36,85 So e Soud e 38,65 27,05 38,06 Sod e 27,05 30,48 19,86 Soud2 e Sod2 e 29,76 26,17 Related decision 15 e - exercise the option Sod3 e k- keep the option 23,53 Binomial Vo=1,8 million € B-S Vo=1,45 million €

- 35. Quantitative – Sequential compound Inter-project compoudness Option on option Stock price (PV of the cash flow as of now) S0= 36.85 Exercise prices X5= 2.24 X4= 3.28 X3= 8.05 X2= 12.35 X1= 10.06 X0= 7.93 Standard deviation (annual volatility of the asset) =30.9% Risk-free rate (continuous) rf=6.1% Time to expiration T=6 Year Time step t=1

- 36. Quantitative – Sequential compound Step 0 1 2 3 4 5 6 235,43 Factors 172,83 Sou6 e u= 1,362 Sou5 e 233,19 d= 0,734 126,88 170,59 p= 0,524 Sou4 e 126,88 X5= 2,237 93,14 124,83 93,14 Sou5 d e Sou3 e Sou4 d e 124,64 91,25 68,38 91,04 68,38 Sou3 d e 68,38 Sou2 e 50 66,40 50,19 Sou4 d2 e 50,19 68,38 Sou2 d e Sou3 d2 e 66,14 Sou e 48,33 48,09 36,85 50,19 36,85 36,85 36,85 So e Soud e Sou2 d2 e Sou3 d3 36,50 27,05 36,85 34,87 34,61 Sod e 27,05 27,05 26,27 19,86 Soud2 e Sou2 d3 e 19,86 Sod2 e 25,19 19,86 24,95 Sou2 d4 e 18,11 Soud3 e 17,62 15 17,88 14,58 Sod3 e Soud4 e 10,70 13 11 12,47 Soud5 e Sod4 e 8,47 8,72 7,86 Related decision Sod5 e 5,77 e - exercise the option 5,75 Sod5 e k- keep the option 3,53

- 37. Quantitative – Sequential compound Step 0 1 2 3 4 5 Factors 170,73 u= 1,362 Sou5 e d= 0,734 124,90 167,44 p= 0,524 Sou4 e X4= 3,283 91,28 121,81 91,04 Sou3 e Sou4 d e 88,37 66,40 87,75 68,38 Sou3 d e Sou2 e 48,33 63,31 48,09 50,19 65,09 Sou2 d e Sou3 d2 e Sou e 45,43 44,81 36,50 47,11 36,85 34,87 So e Soud e Sou2 d2 e 33,99 26,27 33,57 31,78 Sod e 25,19 24,95 24,06 18,11 Soud2 e Sou2 d3 e Sod2 e 22,28 17,88 21,66 16,80 Soud3 e 12,72 14,79 12,47 Sod3 e Soud4 e 9,81 8,72 9,19 Sod4 e 5,63 5,75 Related decision Sod5 e e - exercise the option 2,47 k- keep the option Asset values are replaced by option values from previous lattice

- 38. Quantitative – Sequential compound Step 0 1 2 3 4 X3= 8,046 121,81 Sou4 e 88,37 113,76 Sou3 e 80,80 63,31 65,09 Sou3 d e Sou2 e 45,43 55,26 47,11 57,05 Sou2 d e Sou e 37,86 33,99 39,54 33,57 31,78 So e Soud e Sou2 d2 e 26,87 24,06 25,52 23,73 Sod e 22,28 16,50 16,80 Soud2 e Sod2 e 14,71 14,79 8,76 Soud3 e 9,81 6,74 Sod3 e 3,32 5,63 Sod4 k 0,00 Related decision e - exercise the option k- keep the option

- 39. Quantitative – Sequential compound Step 0 1 2 3 4 X3= 8,046 121,81 Sou4 e 88,37 113,76 Sou3 e 80,80 63,31 65,09 Sou3 d e Sou2 e 45,43 55,26 47,11 57,05 Sou2 d e Sou e 37,86 33,99 39,54 33,57 31,78 So e Soud e Sou2 d2 e 26,87 24,06 25,52 23,73 Sod e 22,28 16,50 16,80 Soud2 e Sod2 e 14,71 14,79 8,76 Soud3 e 9,81 6,74 Sod3 e 3,32 5,63 Sod4 k 0,00 Related decision e - exercise the option k- keep the option

- 40. Quantitative – Sequential compound Step 0 1 2 3 X2= 12,351 80,80 Sou3 e 68,45 57,05 Sou2 e 37,86 39,54 45,15 Sou2 d e Sou e 25,51 26,87 28,35 25,52 So e Soud e 17,20 16,50 13,62 Sod e 14,71 7,23 8,76 Soud2 e Sod2 e 2,36 1,16 Related decision 3,32 e - exercise the option Sod3 k k- keep the option 0,00

- 41. Quantitative – Sequential compound Step 0 1 2 X1= 10,056 45,15 Sou2 e 28,35 35,09 Sou e 17,20 18,89 13,62 So e Soud e 10,09 7,23 3,57 Sod e Related decision 1,76 1,16 e - exercise the option Sod2 k k- keep the option 0,00 Step 0 1 X0= 7,933 18,89 Sou e 10,09 10,95 So e 5,40 1,76 Sod k Related decision 0,00 e - exercise the option k- keep the option

- 42. Quantitative – Sequential compound Option / project values taken from related lattice Step 0 1 2 3 4 5 6 Sou6 Sou5 233,19 167,44 Sou4 113,76 Sou5 d Sou3 Sou4 d 124,64 68,45 87,75 Sou3 d Sou2 55,26 Sou4 d2 35,09 Sou2 d Sou3 d2 66,14 Sou 25,51 44,81 10,95 So Soud Sou2 d2 Sou3 d3 5,40 3,57 23,73 34,61 Sod 0,00 Soud2 Sou2 d3 Sod2 2,36 21,66 Sou2 d4 0,00 Soud3 17,62 6,74 Sod3 Soud4 0,00 9,19 Soud5 Sod4 8,47 0,00 Sod5 2,47 Sod5 3,53

- 43. Quantitative – Changing volatilities Stock price (PV of the cash flow as of now) S0= 28.55 Exercise price (PV of CAPEX as of Y2) X=43.10 Standard deviation (annual Volatility year 1) =40.64% Standard deviation (annual Volatility year 2) =30.91% Risk-free rate (continuous yearly) rf=6.1% Time to expiration T=2 Years Time step t=1 Step 0 1 2 Factors u1= 1,501 58 d1= 0,666 Sou1u2 e p1= 0,475 15,29 43 u2= 1,362 Sou1 k d2= 0,734 7,53 p2= 0,524 31 Sou1d2 k 0,00 28,55 So k 3,37 26 Sod1u2 k 0,00 19 Sod1 k 0,00 Related decision 14 e - exercise the option Sod1d2 k k- keep the option 0,00 r 2 = 2 + 2

- 44. Quantitative – Different volatilities r 2 = 2 + 2 Stock price (PV of the cash flow as of now) S0= 28.55 Exercise price (PV of CAPEX as of Y2) X=43.10 Standard deviation (annual Volatility year 1) =74.17% Standard deviation (annual Volatility year 2) =30.91% Risk-free rate (continuous yearly) rf=6.1% Time to expiration T=2 Years Time step t=1 Step 0 1 2 Factors 234 u1= 1,362 Sou1u2u1u2 d1= 0,734 190 p1= 0,524 53 82 Sou1u2u1d2 u2= 2,100 Sou1u2 10 d2= 0,476 50 50 126 p2= 0,361 Sou1u2d1u2 83 29 Sou1u2d1d2 0 53 Sou1d2u1u2 10 12 19 Sou1d2u1d2 Sou1d2 0 2 2 29 Sou1d2d1u2 0 6 Sou1d2d1d2 28,55 0 So 13 13 126 Sod1u2u1u2 83 29 44 Sod1u2u1d2 Sod1u2 0 19 19 68 Sod1u2d1u2 25 15 Sod1u2d1d2 0 29 Sod1d2u1u2 0 6 10 Sod1d2u1d2 Sod1d2 0 0 0 15 Sod1d2d1u2 0 3 Sod1d2d1d2 0 Vp=12.6 million € r=80.35% VBS = 9.96 million €

- 45. Summary of the results 1. Average Average Method Annual volatility in % Passive NPV Option Value Expanded NPV Option Value Expanded NPV Option Value Expanded NPV Option Value Expanded NPV Option value Expanded NPV Standard deviation in firm value 40,64 1,85 2,98 4,83 4,05 5,90 3,10 4,95 2,90 4,75 3,26 5,11 Logarithmic stock price returns 30,91 1,85 1,73 3,58 2,43 4,28 1,74 3,59 2,13 3,98 2,01 3,86 Logarithmic CF from project returns 29,70 1,85 1,58 3,43 2,22 4,07 1,57 3,42 1,39 3,24 1,69 3,54 Implied volatility B-S model 27,47 1,85 1,29 3,14 1,84 3,69 1,25 3,10 1,32 3,17 1,42 3,27 Logarithmic stock price returns 30,91 1,85 1,42 3,27 2,17 4,02 1,43 3,28 1,12 2,97 1,54 3,39 2. Average Method Annual volatility in % Passive NPV Option Value Expanded NPV Option value Expanded NPV Logarithmic stock price returns 30,91 1,85 4,17 6,02 4,17 6,02 3. Average Average Method Annual volatility in % Passive NPV Option Value Expanded NPV Option Value Expanded NPV Option value Expanded NPV Logarithmic stock price returns 30,91 1,85 1,45 3,30 1,80 3,65 1,63 3,48 4. Average Method Annual volatility in % Passive NPV Option Value Expanded NPV Option value Expanded NPV Logarithmic stock price returns 30,91 1,85 3,55 5,40 3,55 5,40 5. Average Method Annual volatility in % Passive NPV Option Value Expanded NPV Option value Expanded NPV Standard deviation in firm value 40,64 Logarithmic stock price returns 30,91 6. Average Average Method Annual volatility in % Passive NPV Option Value Expanded NPV Option Value Expanded NPV Option Value Expanded NPV Option value Expanded NPV Logarithmic stock price returns 74,17 Logarithmic stock price returns 30,91 r 2 = 1 2 + 2 2 80,35 1,85 8,11 9,96 8,55 10,40 8,33 10,18 CRR 1 step CRR 5 steps CRR 3 stepsB-S Sequential compound option in 1.000.000 EUR Simulation Option to differ the investment for two years with private risks in 1.000.000 EUR Option to differ the investment for one year with competition inclouded (dividend yield y=1,93%) in 1.000.000 EUR CRR 1 step + DTA Option to contract the investment in the following three years in 1.000.000 EUR B-S CRR 2 steps Calculation model Option to differ the investment for one year in 1.000.000 EUR 1,52 3,37 CRR 6 steps Option to differ the investment for two years with changing volatilities in 1.000.000 EUR CRR 2 steps B-S 3,37 12,60 1,52 10,75 Option to differ the investment for two years with differnet volatilities in 1.000.000 EUR non recomb. 2 steps 1,85 1,85 10,75 12,60

- 46. Conclusions • Future management response to altered future business environment conditions expands an investment opportunity value by improving its upside potential or by limiting its downside losses, relative to the passive operating strategy • Related to the parameterizations conclusions are twofold: • For low volatilities, combination of specifically designed parameterizations and increased number of steps must be used in order to have results that are with low margin of error and • Within higher volatilities, all parameterizations are producing fairly good estimates as long as the number of steps is greater than two.

- 47. Conclusions • The process of changes of the underlying asset value has to corresponds to the actual project being analyzed • The best approximation of the continuous process with the discrete one, as used in the binomial approach the conclusions are twofold: • For low volatilities, combination of specifically designed parameterizations and increased number of steps must be used in order to have results that are with low margin of error and • Within higher volatilities, all parameterizations are producing fairly good estimates as long as the number of steps is greater than two.

- 48. Thank You

- 49. Back up slide - Brownian motion & Jump