Chapter10final 111017231701-phpapp02

- 2. CostFunctions A cost function is a mathematical representation of how a cost changes with changes in the level of an activity relating to that cost

- 3. CostTerminology Variable Costs –costs that change in total in relation to some chosen activity or output Fixed Costs – costs that do not change in total in relation to some chosen activity or output Mixed Costs –costs that have both fixed and variable components; also called semivariable costs

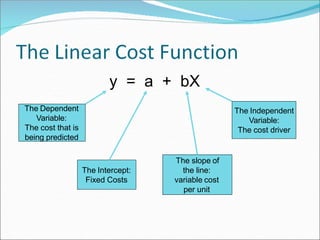

- 4. y = a + bX The Dependent Variable: The cost that is being predicted The Independent Variable: The cost driver The Intercept: Fixed Costs The slope of the line: variable cost per unit

- 6. CostEstimation Methods 1. Industrial Engineering Method 2. Conference Method 3. Account Analysis Method 4. Quantitative Analysis Methods 1. High-Low Method 2. Regression Analysis

- 7. Industrial EngineeringMethod Estimates cost functions by analyzing the relationship between inputs and outputs in physical terms Includes time-and-motion studies Very thorough and detailed, but also costly and time- consuming Also called the Work-Measurement Method

- 8. Conference Method Estimates cost functions on the basis of analysis and opinions about costs and their drivers gathered from various departments of a company Pools expert knowledge Reliance on opinions still make this method subjective

- 9. Account AnalysisMethod Estimates cost functions by classifying various cost accounts as variable, fixed or mixed with respect to the identified level of activity Is reasonably accurate, cost-effective, and easy to use, but is subjective

- 10. Quantitative Analysis Uses a formal mathematical method to fit cost functions to past data observations Advantage: results are objective

- 11. Stepsin Estimating aCostFunction Using Quantitative Analysis 1. Choose the dependent variable (the cost to be predicted) 2. Identify the independent variable or cost driver 3. Collect data on the dependent variable and the cost driver 4. Plot the data 5. Estimate the cost function using the High-Low Method or Regression Analysis 6. Evaluate the cost driver of the estimated cost function

- 13. High-Low Method Simplest method of quantitative analysis Uses only the highest and lowest observed values

- 14. High – Low Method Plot

- 15. Stepsin the High-LowMethod 2. Calculate variable cost per unit ofactivity Variable { Cost associated with - Cost associated with }Cost per = highest activity level lowest activity level Unit of Activity Highest activity level - Lowest activitylevel

- 16. Stepsin the High-LowMethod 1. Calculate Total Fixed Costs Total Cost from either the highest or lowest activity level - (Variable Cost per unit of activity X Activity associated with above totalcost) Fixed Costs 5. Summarize by writing a linearequation Y = Fixed Costs + ( Variable cost per unit of Activity * Activity ) Y = FC + (VCu * X)

- 17. RegressionAnalysis Regression analysis is a statistical method that measures the average amount of change in the dependent variable associated with a unit change in one or more independent variables Is more accurate than the High-Low method because the regression equation estimates costs using information from all observations; the High- Low method uses only two observations

- 18. Typesof Regression Simple – estimates the relationship between the dependent variable and one independent variable Multiple – estimates the relationship between the dependent variable and two or more independent variables

- 21. Terminology Goodness of Fit –indicates the strength of the relationship between the cost driver and costs Residual Term –measures the distance between actual cost and estimated cost for each observation