Essentials of IFRS 18 - Prof Oyedokun.pptx

Download as PPTX, PDF0 likes0 views

Being an Intensive Training Paper on IFRS/Internal Controls for NNPC Pension Middle Management Staff Held at Cairo, Egypt on Thursday, July 24, 2025.

Essentials of IFRS 18 - Prof Oyedokun.pptx

- 1. IFRS 18 – Presentation and Disclosure in Financial Statements Prof. Godwin Emmanuel Oyedokun Professor of Accounting and Financial Development Department of Management & Accounting Faculty of Management and Social Sciences Lead City University, Ibadan, Nigeria Principal Partner; Oyedokun Godwin Emmanuel & Co (Accountants, Tax Practitioners & Forensic Auditors) Being an Intensive Training Paper on IFRS/Internal Controls for NNPC Pension Middle Management Staff Held at Cairo, Egypt on Wednesday, July 23, 2025.

- 2. ND (Fin), HND (Acct.), BSc. (Acct. Ed), BSc (Fin.), LLB., LLM, MBA (Acct. & Fin.), MSc. (Acct.), MSc. (Bus &Econs), MSc. (Fin), MSc. (Econs), Ph.D. (Acct), Ph.D. (Fin), Ph.D. (FA), CICA, CFA, CFE, CIPFA, CPFA, CertIFR, ACS, ACIS, ACIArb, ACAMS, ABR, IPA, IFA, MNIM, FCA, FCTI, FCIB, FCNA, FCFIP, FCE, FERP, FFAR, FPD-CR, FSEAN, FNIOAIM, FCCrFA, FCCFI, FICA, FCECFI, JP Prof. Godwin Emmanuel Oyedokun Professor of Accounting and Financial Development Department of Management & Accounting Faculty of Management and Social Sciences Lead City University, Ibadan, Nigeria Principal Partner; Oyedokun Godwin Emmanuel & Co (Accountants, Tax Practitioners & Forensic Auditors)

- 3. IFRS 18 – Presentation and Disclosure in Financial Statements

- 4. Contents Introduction Objectives of IFRS 18 Major Changes Introduced by IFRS 18 Management-Defined Performance Measures (MPMs) Statement of Profit or Loss Statement of Financial Position Statement of Cash Flows Disaggregation and Materiality in IFRS 18 Implementation Considerations for Preparers Implications for Users of Financial Statements Transition Guidance and Early Adoption Potential Challenges and Mitigation MPM Sample Categories Conclusion

- 5. Introduction to IFRS 18 IFRS 18 is the International Financial Reporting Standard issued by the International Accounting Standards Board (IASB) to replace IAS 1. It introduces a revised structure for presenting financial statements and aims to improve comparability, transparency, and relevance of financial reporting globally. Why IFRS 18? Challenges Identified by IASB • Diverse income statement formats among companies. • Difficulty for investors to compare performance effectively. • Unstandardized definitions for non-IFRS measures (e.g., EBITDA). IFRS 18's Solutions • Mandatory categories and subtotals in profit or loss statements. • Required disclosure of management-defined performance measures (MPMs). • Clearer disaggregation requirements for financial data.

- 6. Objectives of IFRS 18 IFRS 18 was developed with clear objectives to enhance the utility and reliability of financial reporting. Improve Comparability Standardizing financial statement presentation across diverse companies and industries. Enhance Transparency Standardizing line items and metrics to provide clearer insights into financial performance. Clarify Non-GAAP Measures Reducing misleading presentations by providing clear guidelines for non-GAAP performance measures. Support Informed Decisions Enabling users (analysts, investors, regulators) to make better- informed decisions based on consistent, reliable data.

- 7. Major Changes Introduced by IFRS 18 IFRS 18 introduces new requirements for Management-Defined Performance Measures (MPMs), enhancing transparency and comparability of these key metrics. 1 What are MPMs? Performance metrics like Adjusted EBITDA or Core Operating Profit, which management believes better explain the entity's financial performance. 2 New Disclosure Requirements • Reconciliation to the most comparable IFRS measure. • Description of calculation methods and usefulness. • Disclosure of any changes in calculation from prior periods. Example: Telecom Company If a telecom reports "Adjusted Operating Profit" excluding restructuring costs, IFRS 18 requires disclosure of excluded items, reconciliation to IFRS Operating Profit, and justification for the adjusted figure's usefulness. Management-Defined Performance Measures (MPMs)

- 8. Statement of Profit or Loss IFRS 18 introduces a revised structure for the statement of profit or loss, mandating new categories and subtotals to enhance clarity and comparability. New Categories Introduced • Operating: Core business activities, such as sales revenue, cost of goods sold, and administrative expenses. For a pharmaceutical company, this includes drug sales, R&D, and employee costs. • Investing: Income and expenses from investments, like interest income from bonds or dividends from equity investments not held for control. Income from biotech startup investments falls here. • Financing: Items related to capital structure, including interest expense and gains/losses • on bond repurchase. Mandatory Subtotals • Operating profit: A clearly defined and standardized measure. • Profit before financing and income taxes: Provides a clear view of performance before capital structure and tax effects. • Profit before tax: The final profit figure before tax implications.

- 9. Statement of Financial Position IFRS 18 mandates greater disaggregation of line items in the Statement of Financial Position to enhance relevance and clarity for financial statement Disaggregation Requirements Entities must disaggregate line items where it adds relevance to the financial position. This provides a more detailed understanding of assets and liabilities. Example: Trade and Other Receivables Instead of a single line, "Trade and other receivables" might be split into: • Trade receivables from customers • Prepayments • Receivables from related parties

- 10. Statement of Cash Flows IFRS 18 introduces stricter requirements for the classification of cash flows, ensuring alignment with the categories presented in the profit or loss statement. 1 Operating Cash Flows Must be directly linked to the operating category in the profit or loss statement. 2 Investing Cash Flows Include items like dividends received and interest income, reflecting their classification in the income statement. 3 Financing Cash Flows Involve interest paid and repayments of borrowings, aligning with the financing category. Example: If a company presents interest income in the Investing category of its income statement, the corresponding cash inflow must now also be shown under Investing activities in the cash flow statement. This ensures consistency and clarity across financial reports.

- 11. Disaggregation and Materiality in IFRS 18 IFRS 18 strongly emphasizes "sufficient disaggregation," ensuring that financial information is presented with enough detail to be relevant without obscuring key insights. Visible Reporting Aggregate sales by region Disaggregation Rules Separate by nature & function Measurement Differences Use consistent bases per item Materiality Principles Exclude immaterial aggregation impact Example Combine sales only if similar

- 12. Implementation Considerations for Preparers Adopting IFRS 18 requires a systematic approach, involving significant updates to financial systems, processes, and internal communications. Practical Steps to Implement • Revise Chart of Accounts: Adapt to track transactions by new IFRS 18 categories. • Update Financial Reporting Software: Align reports with new subtotals and MPM reconciliations. • Train Accounting and Finance Teams: Ensure proficiency in the revised format and disclosure requirements. • Review Internal KPIs and Reports: Align key performance indicators and executive reports with IFRS 18 standards. Internal Communication Effective communication is crucial for smooth transition. • Senior Management and Audit Committees: Must fully understand disclosed MPMs and their rationale. • External Disclosures: Ensure consistency and alignment with investor presentations for clarity and credibility.

- 13. Implications for Users of Financial Statements IFRS 18 fundamentally enhances the quality of financial information, empowering users to make more insightful and comparable analyses. Greater Clarity on Operations Consistent "Operating Profit" definitions allow for clearer understanding of core business performance across entities. Enhanced Trust in MPMs Reconciliation and regulation of alternative performance measures improve their reliability and credibility. Better Decision-Making Access to disaggregated and transparent information facilitates more informed investment and analytical decisions. Before IFRS 18, different companies might report "Operating Profit" with varying inclusions, complicating comparisons. Now, adherence to a standardized format ensures consistency, significantly improving the utility of financial statements for users.

- 14. Transition Guidance and Early Adoption IFRS 18 is effective from 1 January 2027. Early adoption is permitted with appropriate disclosures, but requires retrospective application. • Entities must restate comparatives for the prior period. • This ensures year-on-year comparability from the adoption year. Restatement ensures that financial statements are consistently presented, allowing stakeholders to make informed comparisons and analyses of performance over time.

- 15. Potential Challenges and Mitigation Restructuring internal reporting Begin aligning management reports early Understanding new categorization rules Train staff and use professional IFRS consultants Defining and reconciling MPMs Establish clear policies and governance for consistency Systems upgrade Engage IT early in transition process Addressing these challenges proactively ensures a smoother transition to IFRS 18, minimizing disruption and maximizing compliance

- 16. MPM Sample Categories 1 Adjusted Operating Profit Reflects core operational performance by excluding one-off costs and impairments. 2 Core EBITDA (Earnings before Interest, Taxes, Depreciation and Amortization) Measures earnings from core operations before non-cash items and tax effects. 3 Underlying Profit After Tax Shows profit performance excluding effects of foreign exchange volatility and fair value gains.

- 17. Adjusted Operating Profit Used by: Manufacturing Company Ltd. Purpose: To reflect core operational performance, excluding one-off restructuring costs and impairment. Operating Profit (as per IFRS 18) 125000 Add: Restructuring expenses 8000 Add: Impairment loss on equipment 5000 Less: One-time insurance claim received -3000 Adjusted Operating Profit (MPM) 135000 Why Useful: Management believes this measure better reflects sustainable profit from regular operations and removes unusual or non-recurring items that distort comparison across periods.

- 18. Core EBITDA Used by: Telecoms Nigeria Plc Purpose: To measure earnings generated from core operations before non-cash items and before interest/tax effects. Operating Profit (IFRS 18) 92000 Add: Depreciation 18000 Add: Amortization 12000 Less: Gain on disposal of fibre optic cable -2000 Core EBITDA (MPM) 120000 Why Useful: Core EBITDA is widely used by investors to evaluate operational efficiency and cash-generating ability, unaffected by capital structure and non-cash expenses.

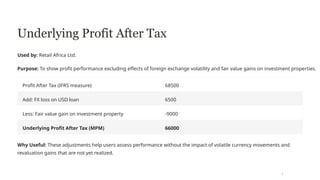

- 19. Underlying Profit After Tax Used by: Retail Africa Ltd. Purpose: To show profit performance excluding effects of foreign exchange volatility and fair value gains on investment properties. Profit After Tax (IFRS measure) 68500 Add: FX loss on USD loan 6500 Less: Fair value gain on investment property -9000 Underlying Profit After Tax (MPM) 66000 Why Useful: These adjustments help users assess performance without the impact of volatile currency movements and revaluation gains that are not yet realized.

- 20. Conclusion IFRS 18 marks a significant evolution in financial reporting: • It provides structure and discipline to financial statements. • It enhances credibility of performance measures. • It allows investors to better compare and analyze companies. Trainees are encouraged to: • Study real-life financial statements from pilot companies. • Practice mapping financial items to new IFRS 18 categories. • Prepare sample MPM reconciliations.

- 21. Prof. Godwin Emmanuel Oyedokun Professor of Accounting & Financial Development Lead City University, Ibadan, Nigeria Principal Partner; Oyedokun Godwin Emmanuel & Co (Accountants, Tax Practitioners & Forensic Auditors) [email protected]; [email protected] +2348033737184 & 2348055863944