Healthcare Reform Legislation and the Impacts on HR - a Pearson Partners HR Roundtable Presentation

1 like479 views

The document provides an overview of health care reform timelines and key changes effective from 2011 through 2020 due to the Patient Protection and Affordable Care Act (PPACA). It details regulations regarding coverage limits, pre-existing conditions, employer responsibilities, and the establishment of health insurance exchanges. Additionally, it highlights the importance of improving health through better diet and exercise while addressing the financial implications of various health care reforms.

Healthcare Reform Legislation and the Impacts on HR - a Pearson Partners HR Roundtable Presentation

- 1. Health Care Reform Here It Is May 11, 2010 DFW HR Roundtable

- 2. Health C are R eform Timeline (as of Marc h 30, 2010)* *Timeline indicates changes for mid to large employers’ calendar year, grandfathered plans Summary of Selected Changes Jan. 1, 2011 • Lifetime dollar limits prohibited • Annual dollar limits restricted • Dependent child coverage expanded (up to age 26) • Pre-existing condition exclusions prohibited for dependents (under 19 years of age) • Uniform explanation of coverage effective • Cost reporting and rebates effective • Phase out of Part D “donut hole” begins • Long-term care program (CLASS Act) • W-2 reporting for 2011 begins • OTC drugs ineligible for FSA, HSA, HRA • Medicare Advantage funding reduced Jan. 1, 2014 • Annual dollar limits prohibited • Pre-existing condition exclusions prohibited for all enrollees • Auto enrollment required • Waiting periods over 90 days no longer permitted • Health insurance exchanges established • Individual and employer mandates effective • Low income premium subsidy in the exchange • Employee vouchers for exchange Jan. 1, 2020 1st Qtr, 2010 Part D “donut hole” filled Jan. 1, 2012 Accounting charge – RDS Comparative effectiveness research tax Jan. 1, 2018 High-cost insurance excise tax is established June 21, 2010 Temporary reinsurance program for early retirees (ages 55-64) established 2010 1 Jan. 1, 2013 • Health Care FSA contributions capped • Medicare Hospital Insurance tax 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

- 3. Status • Patient Protection and Affordable Care Act (PPACA) – Signed into law on March 23, 2010 • Health Care and Education Tax Credit Reconciliation Act of 2010 – Signed into law on March 30, 2010 2

- 4. Health Care Reform Overview Market Reform Individual Responsibility Insurance Exchanges Employer Responsibility Financing Retiree Issues Beyond Reform: Improving Health 3

- 5. Market Reform Health Care Reform Crosses the Finish Line

- 6. Market Reform • Effective First Plan Year Six Months After Enactment – – – – – No lifetime limits Only allow restricted annual dollar limits on essential benefits Prohibition on rescission No pre-existing conditions on dependents below age 19 Development and utilization of uniform explanation of coverage and standard definitions – Extension of dependent coverage for married and unmarried adult children to age 26 – Medical loss ratio (MLR) requirements (85 large employer/80 small employer and individual) and rebates 5

- 7. Market Reform • Effective First Plan Year Six Months After Enactment (continued) – Coverage of preventive health services (GF*) – Prohibition on discrimination in favor of highly compensated employees for insured plans (GF*) – Required to implement various activities such as case management, reduction in hospital readmission and wellness programs and report the status of the activities to the Secretary of HHS and participants; Secretary may implement penalties for noncompliance – Mandated appeals process, including external review (GF*) – Require certain choice of providers for pediatric and ob/gyn care and require in-network coverage for emergency room visits to non-network providers (GF*) – Federal annual premium review (coordinated with each State) *provisions do not apply to grandfathered employer plans 6

- 8. Market Reform • Effective January 1, 2014 – Prohibit pre-existing conditions exclusions – Premiums may only vary based on: • • • • Individual or family coverage Rating area (as established by the each state) Age: 3 to 1 Tobacco use: 1.5 to 1 – Guaranteed issue and renewability – Coverage of certain clinical trial treatment (GF*) – Prohibition against discrimination based on health status, but exempts certain wellness programs and allows them to increase the premium reduction for participation in a wellness program (GF*) – Limits on cost sharing (for insurers in an Exchange) – No waiting periods greater than 90 days *provisions do not apply to grandfathered employer plans 7

- 9. Market Reform: Grandfathered Plans • A plan in existence on March 23, 2010 would only be required to: – Effective for plan years six months after enactment • • • • • Not have lifetime limits Not impose restricted annual dollar limits from 2010-2014 Extend coverage to unmarried or married adult children to age 26 Use the standard uniform explanation of coverage (once developed) Give rebates if MLRs do not meet the applicable standards (only for insurers, not self-funded plans) • Not allow rescission – Effective January 1, 2014 • Not have waiting periods greater than 90 days • Eliminate any annual dollar limits in 2014 8

- 10. Individual Responsibility Health Care Reform Crosses the Finish Line

- 11. Individual Responsibility • Starting 2014, all individuals must obtain health care coverage or pay a penalty, which would be the greater of: – – – – – 10 2014: 0.1% of AGI or $95/person 2015: 2.0% of AGI or $325/person 2016: 2.5% of AGI or $695/person Indexed after 2016 Family flat dollar amount capped at 300% of individual penalty

- 12. Insurance Exchanges Health Care Reform Crosses the Finish Line

- 13. Exchanges • A state clearinghouse that facilitates the purchase of health insurance coverage for individuals and employers, either through private insurers or a co-op • Eligibility – Any individual – Small employers (100 or less employees) – Large employers starting in 2017 • Premium and cost-sharing subsidies available to individuals 400% below the FPL • Employees are eligible to join an Exchange if their employer coverage is unaffordable (9.5% of AGI) or the employer plan does not have at least a 60% actuarial value 12

- 14. Employer Responsibility Health Care Reform Crosses the Finish Line

- 15. Employer Responsibility • Effective 2014 • If employer does not provide coverage and at least one employee obtains low-income premium subsidy in an Exchange – Penalty of $2,000 times number of FTEs – Not deductible by employer • Employer does provide coverage, but – Employer plan fails: • 60% minimum value test, or • 9.5% AGI affordability test; and • Employee enrolls in Exchange and receives low-income subsidy – Penalty of $3,000 per employee with subsidy – Maximum of $2,000 times number of FTEs 14

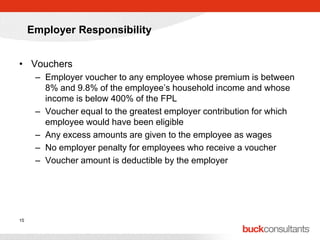

- 16. Employer Responsibility • Vouchers – Employer voucher to any employee whose premium is between 8% and 9.8% of the employee’s household income and whose income is below 400% of the FPL – Voucher equal to the greatest employer contribution for which employee would have been eligible – Any excess amounts are given to the employee as wages – No employer penalty for employees who receive a voucher – Voucher amount is deductible by the employer 15

- 17. Employer Responsibility • Automatic enrollment (2014) • Additional reporting and notice requirements – W-2 reporting of the value of health, employer HSA contributions, HRA contributions and dental and/or vision if not stand alone plans (2011 income reported in 2012) – Explanation of Exchange (3/31/2013) – Reporting of insurance coverage to the IRS and the participant (2014) – Disclosure of plan data and financials, such as enrollment, disenrollment, and claims denials (2014) (for nongrandfathered plans) – Cadillac tax calculation and reporting (health, employee health FSA, employer and employee pre-tax HSA contributions, and HRA contributions) (2018) 16

- 18. Financing Health Care Reform Crosses the Finish Line

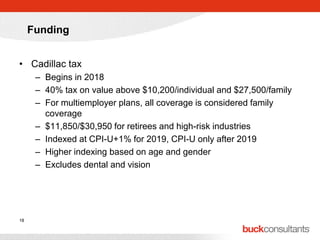

- 19. Funding • Cadillac tax – Begins in 2018 – 40% tax on value above $10,200/individual and $27,500/family – For multiemployer plans, all coverage is considered family coverage – $11,850/$30,950 for retirees and high-risk industries – Indexed at CPI-U+1% for 2019, CPI-U only after 2019 – Higher indexing based on age and gender – Excludes dental and vision 18

- 20. Funding • Provider surcharges – Pharmaceutical manufacturers ($26 billion over 9 years starting in 2011; indexed after 2019) – Medical devices (2.3% excise tax starting in 2013) – Insurers ($58.8 billion over 5 years starting in 2014; $14.3 billion/year trended after 2018) • Medicare Hospital Insurance Tax – Increases tax rate from 1.45% to 2.35% starting in 2013 for highincome earners (income in excess of $250,000 for joint filers; $200,000 for others) – 3.8% tax on net investment income (income in excess of $250,000 for joint filers; $200,000 for others) 19

- 21. Funding • Health FSA cap of $2,500 starting in 2013 • Prohibition on reimbursement of over-the-counter medicines from FSAs, HRAs, and HSAs effective 2011 • Taxability of RDS payments to employers in 2013 • Comparative Effectiveness Research tax on insured and selffunded plans of $1/participant/year first year (plan years ending after September 30, 2012); $2 second year; indexed thereafter 20

- 22. Reinsurance Program for Early Retirees • Subsidizes 80% of a retiree’s costs between $15,000 and $90,000 • $5 billion in funding • Effective date: – June 21, 2010 to December 31, 2013 or when funds exhausted 21

- 23. Coverage in Part D Donut Hole • Discount on brand drugs – 50% discount at point of sale – Effective date 2011 • Phases out donut hole coverage to 75% by 2020 – $250 rebate in 2010 – New Part D benefit to supplement 50% discount 22

- 24. Beyond Reform: Improving Health Health Care Reform Crosses the Finish Line

- 25. Diet (Poor), Exercise (Little), and Disease (Lots) • 75% of total health care costs are preventable • Managing diet, exercise, and smoking can reduce*: – – – – Heart disease and stroke by 80% Type-2 diabetes by 80% Cancer by 40% The 67% of adults who are obese or overweight • Changing the mindset is critical: – From treating disease (focus on sickness) – To avoiding disease (focus on health and wellness) • The challenge (and opportunity): – Changing human behavior 24 * Center for Disease Control (CDC), “Chronic Diseases ─ At a Glance 2009,” February 2009

- 26. Disease and Behavior Determinants of health status 20% 20% Genetics Environment 50% 10% Access to Care 25 Sources: Center for Disease Control and Prevention Behavior

- 27. Behavior and Cost $5,520 $3,321 Direct cost as a function of health risk 251% $3,460 $1,261 57% $2,199 $2,199 $2,199 $2,199 High Risk Medium Risk Low Risk 26 Edington – University of Michigan HMRC 2001

- 28. Cost and Comorbidity N = 1,838 Multiples Multiples of annual healthcare costs compared to someone with no health risks Number of Risks 27 Source: Yen, Louis, et al., (2004, Sept/Oct). Associations between health risk appraisal scores and employee medical claims costs in a manufacturing co., AJHP, 11(1), p. 46-54.

- 29. Changing Behavior Information, Incentives, and Infrastructure Information Information (Get attention!) • Personalize (to raise awareness) • Integrate (to lessen confusion) • Simplify (to enable understanding and action) • Inspire (to create an emotional attachment) • Actionable (so I know what to do) Education and Promotion Incentives (Encourage action!) • Personalized (specific to “me”) • Meaningful (to get attention) • Optimal (reach the “tipping point” of action) • Behavioral (to encourage positive actions) A Culture of Organizational & Individual Sustainability Incentives Infrastructure Care Management, Data & Technology Personalized Plan Design, Cost Sharing & Rewards Infrastructure (Enable action!) 28 • Biometrics/HRQs (to raise awareness) • Design components (to raise awareness and encourage action) • Enabling tools, resources and technologies (to personalize & engage)

- 30. Changing Behavior Safeway HDHP design, significant incentives, culture of wellness • Blood pressure – 43% improvement in achieving blood pressure goals • Cholesterol – 18% improvement in achieving cholesterol goals • Body Mass Index (BMI) – 17% improvement in – achieving BMI goals 29 Obesity/overweight percentage dropped 6% < 2% Health care trend from 2005-2009

- 31. Behavior, Wellness, and ROI: The Business Case is Clear Bank of America Blue Shield of CA Duke University Citibank City of Birmingham Coors DuPont General Foods General Motors GlaxoSmithKline Indiana BCBS Johnson & Johnson Life Assurance Nortel Prudential Travelers Union Pacific Washoe County Traditional Newer Programs C/B Ratio • • • • • • • • • • • • • • • • • • Outliers Study Number 30 Source: Chapman Institute, Proof Positive: An Analysis of the Cost-Effectiveness of Worksite Wellness, 2008.

- 32. What About Your Company? • 75% of total health care costs are preventable – Analyze your health care costs – What’s the history of disease progression at your company? • Are you successfully changing employee behavior? – Is participant information personalized to get attention? – Are incentives meaningful to encourage action? – Is the support infrastructure simple to enable action? • Are you measuring your success? – What analytics are you using to determine disease and health improvement? – What is the impact of improved health on business results? – How will you sustain your progress and success? 31

- 34. Additional Information Health Care Reform microsite at www.buckconsultants.com Robyn Bayne 972-628-6811 [email protected] Rex Gale 972-628-6870 [email protected] 33