How the NPP can help you win the war for customer relationships

1 like465 views

The New Payments Platform (NPP) promises to transform payments in Australia by enabling real-time funds transfers 24/7/365. This will address several trends impacting banks, including rising digital disruption, growing non-cash transactions, increasing fintech competition, and an emphasis on customer-centric product design. The NPP offers solutions to back office challenges while unlocking opportunities to strengthen customer relationships through improved payment experiences. Embracing the NPP will be essential for financial institutions to remain competitive and retain customers in the evolving financial services landscape.

How the NPP can help you win the war for customer relationships

- 1. New Payments Platform How the NPP can help you win the war for customer relationships Authors: Nathan Churchward and Natalie Yan-Chatonsky 17 September 2015

- 2. Contents 02 How the NPP can help you win the war for customer relationships 04 Four trends impacting your payments business 08 Although challenges abound, the NPP offers solutions 09 Unlocking stronger customer relationships with the NPP 10 Better experiences mean stronger relationships 13 How to start getting ready for the NPP 15 The way forward 16 About Cuscal 16 About the New Payments Platform 17 About the co-authors

- 3. 2 / How the NPP can help you win the war for customer relationships Rapid innovation has made it an exciting time in the Australian banking industry. At the centre of that excitement is the forthcoming New Payments Platform (NPP), an important initiative that promises to not only position Australia as a global leader in real-time payments, but also help the banking industry address some of its greatest challenges. In the process, it will bring numerous benefits to financial institutions and other organisations, as well as to the customers they serve. How the NPP can help you win the war for customer relationships Moving money around in Australia has historically been a slow process fraught with pain points. Yet with the arrival of the NPP in 2017, many of the inefficiencies that encumber the current system will be removed. In their wake, Australians will be able to transfer funds quickly and easily, 24 hours a day, 7 days a week, for the very first time — even to accounts at other banks. 24/7, Real-time.

- 4. For consumers, the NPP is important not only because it will make sending and receiving payments simple and easy, but also because they’ll be able to enjoy the convenience of doing so from their mobile phones, tablets, or computers in just a matter of seconds. For the banking industry, the NPP represents an opportunity to create the back-office efficiencies necessary to deliver these and other services. Even more importantly, it will be essential ammunition in the war for retaining and acquiring new customers. In the pages that follow, we outline four trends that are currently creating challenges in the banking industry and are therefore central to many companies’ strategies. We also describe what the NPP is and how it will help address those challenges, demonstrating the return on investment (ROI) it will generate along the way. In addition, we explain why the NPP will become critically important to customer relationships and why, to reap all of its benefits, financial institutions need to start getting ready for it right away. The paper concludes with some practical advice about what financial institutions need to do now to start preparing for the NPP. 3 / How the NPP can help you win the war for customer relationships

- 5. 4 / How the NPP can help you win the war for customer relationships Four trends impacting your payments business Source: “Strategic choices for banks in the digital age”, McKinsey & Company, January 2015. These include: 1. The digital transformation of banking Every industry either already has or soon will be disrupted by the rise of digital technologies. Banking is no exception. In fact, digitisation is fundamentally changing the industry by automating previously manual processes, creating opportunities for new products and services, and enhancing customer experiences. For the banking industry, this digital transformation has the potential to either be the next big opportunity or one of its greatest threats. For those organisations that embrace digital innovation and get it right, the upside potential could be significant. Increased revenue from new offers, business models, and products, combined with the greater efficiencies and lower operational costs that digital technologies enable, have the potential to increase profits by 40 percent or more (See Figure 1). Figure 1: A comparison of the potential threats and opportunities of digitisation Potential threats Innovative new offers by competitors Increased revenues from innovative new offers and business models Margin compression Increased revenues from new products, distinctive digital sales, and using data to cross-sell Increased operational risk Lower operational costs from automation/digitalization and transaction migration Potential opportunities +5 +10 +45-35 -6 -16 -13 +30 Up to 35% of net profit eroded for digital laggards. Over 40% of net profit upside for winners. A number of exciting innovations are currently reshaping banking in Australia. When it comes to payments, four main trends are converging that promise deep and lasting change to the financial services industry. TOTAL

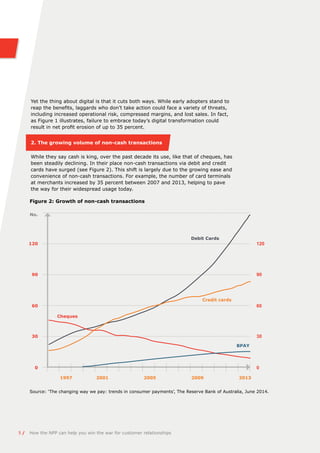

- 6. No. Debit Cards Credit cards Cheques BPAY 120 120 90 90 60 60 30 30 0 0 1997 2001 2005 2009 2013 Figure 2: Growth of non-cash transactions Source: ‘The changing way we pay: trends in consumer payments’, The Reserve Bank of Australia, June 2014. Yet the thing about digital is that it cuts both ways. While early adopters stand to reap the benefits, laggards who don’t take action could face a variety of threats, including increased operational risk, compressed margins, and lost sales. In fact, as Figure 1 illustrates, failure to embrace today’s digital transformation could result in net profit erosion of up to 35 percent. 2. The growing volume of non-cash transactions While they say cash is king, over the past decade its use, like that of cheques, has been steadily declining. In their place non-cash transactions via debit and credit cards have surged (see Figure 2). This shift is largely due to the growing ease and convenience of non-cash transactions. For example, the number of card terminals at merchants increased by 35 percent between 2007 and 2013, helping to pave the way for their widespread usage today. 5 / How the NPP can help you win the war for customer relationships

- 7. 6 / How the NPP can help you win the war for customer relationships Meanwhile innovations in card acceptance technology such as the adoption of contactless card payments, combined with advances in mobile banking and tap and go technology, have made non-cash transactions fast, easy, and convenient. What the data clearly shows is that when those conditions exist, Australians are happy to use non-cash transactions, particularly if they’re tied back to their own funds rather than a line of credit. This has been particularly true for millennials and small businesses, though it’s rapidly spreading across a much greater portion of Australian society. 3. Fintech companies are increasingly disrupting the industry Financial technology (fintech) companies are not only proliferating, they’re also playing a key role in reshaping the financial services industry. For proof of their growing presence, just look at the explosion of global fintech financing activity in recent years. Consider, for example, that in October 2014 alone, more than $1 billion flowed into fintech start-ups around the world, more capital than was deployed for the same purpose in all 12 months of 2008 combined.1 Of course it’s not just that we’re in the middle of a fintech boom, both globally and in Australia. Far more important is the way that these start-ups are disrupting financial services by building niche products that are better suited to meet the needs of specific segments than anything most incumbent providers are capable of producing. 4. Major banks are adopting customer-centric approaches to product design All of that fintech activity is putting the rest of the industry under pressure. As a result, many organisations are adopting more customer-centric approaches to product design, focusing on the needs of their target markets and how to create value for them. That in turn has meant embracing agile development practices, which all four of the major Australian banks have implemented. By doing so, they have been able to test and learn from their target markets, respond quickly to changes in requirements, and reduce the risk of launching products that don’t meet the needs of their target market. Simply put, the big banks are starting to behave more like start-ups. They’re using agile methodologies to get to market faster and to ensure that the products they’re crafting will appeal to the specific needs of their target audience. The result is that better customer experiences are getting out to market faster, putting even greater pressure on the rest of the industry to keep up. 1 “50 Best Fintech Innovators”, AWI, KPMG Australia, and the Financial Services Council, December 2014.

- 8. Analysing what the competition is doing can go a long way toward helping shape future plans. What could this mean for you? All four of these trends are signs of the dramatic shift that the banking system has undergone in recent years, and bring considerable challenges with them for the industry. For example, consumers’ expectations have changed. Today they not only want, but also expect, their interactions with financial services providers to be fast and easy. And they want to be able to make payments in new ways, typically through mobile phone apps. As if that weren’t enough, competition is heating up, with fintechs and big banks bringing new innovations to market. For today’s financial institutions, all of this means that adaptation is crucial. They not only need to figure out how to give their customers what they want, but also how to quickly upgrade their back offices so that they’re capable of dealing with today’s faster, digital world. Any prolonged hesitation in adapting their businesses to digital is the equivalent of allowing their competitors to eat their lunch. 7 / How the NPP can help you win the war for customer relationships

- 9. 8 / How the NPP can help you win the war for customer relationships Although challenges abound, the NPP offers solutions For many financial institutions the secret to long-term success will be dealing with a combination of customer experience and back-office challenges so that they’re able to not only take advantage of new opportunities, but also keep pace with the major banks. The NPP offers an obvious solution. Borne out of a 2012 mandate by the Reserve Bank of Australia, its focus is on making instantaneous payments the new normal in Australia as they already are in a growing number of countries. As a new, real-time payment stream for low-value payments, the NPP will provide Australian consumers and businesses with a fast, reliable, and data-rich mechanism for making day-to- day payments. By making the payment experience more efficient, the NPP will eliminate many of the back-office challenges currently hindering organisations, freeing them up to focus their efforts on improving customer experiences. And, by facilitating the convergence of commerce and payments, the NPP will help make those experiences better. The result will be Uber- like scenarios where payments are instantaneous, hassle free, and an increasingly integrated part of consumers’ lifestyles. Some of the NPP’s key features will include: •• A centralised addressing service that allows customers to use their mobile number or email address as an alias for their bank account details. •• The Initial Convenience Service (ICS), the industry’s first overlay service that will have its own consumer brand and industry marketing campaign, giving participating financial institutions a common solution across their banking channels. For consumers, businesses, and governments, the ICS not only fulfils the promise of immediate payments, it also eliminates the burden of education by creating a common experience. •• Transaction by transaction settlement, which means that the NPP will be a true real-time payment system capable of offering nearly instantaneous payment processing and settlement. Importantly, unlike with other faster payment schemes across the world, all of these features will be available from day one. That, plus the fact that Australians are early adopters with a track record of readily embracing new payment mechanisms, is a clear sign that unlike faster payment schemes elsewhere, Australian uptake will accelerate quickly. The question is: will your business be ready?

- 10. 9 / How the NPP can help you win the war for customer relationships Unlocking stronger customer relationships with the NPP Since it’s an industry-wide solution, choosing to ignore the NPP simply isn’t an option for financial institutions. In fact, any industry participants that fail to embrace it will quickly be viewed as behind the times, not focused on their customers, and ultimately irrelevant in the marketplace. It’s a potentially fatal blow that’s completely avoidable. The biggest potential benefit the NPP can offer is to create greater customer intimacy, helping you win the war for customer relationships. While there are costs associated with getting ready for and implementing the NPP, they’re minimal when compared to the benefits it will bring, which include: Greater economic activity When it’s fast and efficient to do so, individual consumers, small businesses, and governments will increasingly make their payments digitally from their transaction account. More opportunities The NPP will allow financial institutions to create more opportunities to attract customers and their money. In the process, they’ll also increase their ability to cross-sell other products and services. Plus, by bringing additional utility to transactional accounts, the NPP will help ensure those accounts become more important to customers’ day-to- day lives. They’ll go from being something looked at periodically (typically when they get paid), to people’s primary financial hub that they consult on a daily basis, or even more frequently. A level playing field It used to be that big banks and well-funded fintech start-ups had cornered the market on innovative new products and services. With the NPP, however, any financial institution — big or small — will be able to create innovative payment experiences for its customers.

- 11. 10 / How the NPP can help you win the war for customer relationships Better experiences mean stronger relationships In fact, the NPP will lay the groundwork for making payments very personal and central to the way that people interact with financial institutions and similar organisations. The number of transactions that customers make will increase, so the volume of interactions they have with their financial institution will also increase. Customer experience is of paramount importance in any marketplace with very similar products and services; this is particularly true in financial services. This means that the ability to offer superior payment experiences will become essential to meeting expectations and driving retention. Not only does it promise to increase customer satisfaction, it can also make customer engagement spike dramatically.

- 12. 11 / How the NPP can help you win the war for customer relationships That’s because the NPP will increase the variety of ways in which consumers can make payments, offering digital payment solutions (on top of the already available cash and cards). For the consumer, the advantage is ease and convenience. For the industry, however, transforming businesses to manage end-to-end digital payments opens up a whole raft of new opportunities to engage with and cross-sell to customers. One example of this, for consumers, is where a buyer is looking to transfer a large sum of money to a seller (for example buying a car or a house). Current payment solutions don’t service this scenario very well, making it an anxious time for both buyer and seller. For situations like these the NPP can enable financial institutions to offer their customers greater control and safety, either with straight transactional services which confirm the transfer of money or by developing overlay services which can add extra value by drawing in extra, relevant information from government bodies, or review websites for example. For business customers, there will be opportunities to optimise their inflows and outflows of money, which could create efficiencies around resource- intensive administrative tasks like the reconciliation of payments, invoices and expenses to customers, suppliers and employees.

- 13. 12 / How the NPP can help you win the war for customer relationships Another ground-breaking aspect of the NPP is its centralised real-time addressing service. This will reduce the risk of mistaken payments, as the recipient’s alias will always be validated in real-time, even for scheduled payments. It’s also expected to reduce the overall volume of manual tasks that need to be performed by staff from financial institutions when customers make mistaken payments, leaving them more time for higher value tasks. It is important to highlight that because of restrictions with the NPP addressing service, customers can only use one mobile number (or email address) as an alias per bank account. Given that today most Australians’ transaction accounts are at the centre of their main banking relationship2 (See Figure 3) and customers belong to an average of four financial institutions3 , in the future, people are likely to consolidate the number of main financial institutions that they engage with. And, with the NPP, they will primarily use the transaction account that’s tied to their mobile number as their Main Financial Institution. 2 RFi Group’s Report ‘Main bank share of key products in Australia’ 3 http://www.roymorgan.com.au/findings/5542-big-four-banks-improve- main-financial-institution-consideration-february-2014-201404160451 This means that if financial institutions fail to get their customers to link their mobile number to their bank account they stand to miss out on the fees and cross- selling opportunities that the NPP will produce. For that reason, it’s essential that industry participants promote NPP use early on to help ensure that as many of their customers use them as their MFI for their transaction account. Main bank share of key products in Australia Percentage of banking customers that hold product Percentage of banking customers that hold product with main bank Percentage of products held with main bank 84% 79% 42% 59% 41% 95% 79% 75% 74% 70% 69% 39% 35% 76% 22% 32% 30% 22% 20% 14% 9% 7% 8% Life insurance 6% 5% 2% 8% 3% 18% 4% Car loan SMSF Personal loan Credit card Term deposit Home loan Online savings account Investment property loan Transaction account Source: RFi Group’s 2015 Report Figure 3: Transaction accounts are the lead product for Main Financial Institutions

- 14. How to start getting ready for the NPP First and foremost, having the right mindset is crucial. That means recognising the NPP as a commercial and customer relationship opportunity, rather than viewing it as a compliance exercise. It also means having an external focus. Financial institutions need to devote some time to developing a broader view of the market and how their peers and competitors are approaching the NPP. Given the current disruption from digital disruptors and fintech and the move to customer centricity, forming an independent market view is particularly important. Looking at how competitors are going to apply the NPP to their business and customer base, for example, will help uncover important insights into how to focus your own energy and resources. Will those competitors put all of their payments through the NPP or only certain ones? Will they provide their customers with access to the NPP as a matter of course, or position it as a premium add-on service to make money? Analysing what the competition is doing can go a long way toward helping shape future plans. And, it can be particularly useful when it comes to deciding which additional products and services to add after adopting the NPP. Along with monitoring competitors’ media channels closely, financial institutions can gather insights by attending payments industry events and fintech meetups. The key is to be proactive and to learn as much as possible to help shape your own planning and implementation. It’s not enough to simply recognise that the NPP is a critically important development for Australia’s payments industry, it’s essential for financial institutions to start getting ready for it now. 13 /

- 15. 14 / How the NPP can help you win the war for customer relationships In addition, financial institutions shouldn’t be afraid to experiment with developing new NPP products and services. In fact, all players should take a page from CommBank’s book and its development of the Kaching app. Wanting to build out and test its capabilities around person-to-person payments, CommBank launched Kaching as a stand-alone payments app in 2011. Once it was proven and understood, the capability was migrated into its main mobile banking app. This is a great example of best practice and one that can and should be mirrored by financial institutions looking to adopt the NPP. Of course getting ready for the NPP will take more than just buy-in or a shift in mindset. There are a number of more tangible steps that need to be taken as well. These include: •• Talking to core and channel banking system providers and budgeting for implementation activity in 2016 and 2017 •• Updating core banking systems so that they can integrate with NPP transactions •• Updating mobile and internet banking channels to accommodate the additional information that comes with NPP transactions and new transaction types like payment requests and payments with a linked document •• Thinking about change management within internal operations teams and training them alongside sales and customer service teams •• Talking to legal to update terms and conditions •• Planning a robust marketing launch that leverages industry activity •• Educating customers and getting them ready to use the NPP for real-time payments This will all take time. With the launch of the NPP only two years away, it’s essential to start now. Unlike in other countries where uptake of the NPP was initially slow, in Australia we expect it will be rapid because of the advanced features the NPP will have from Day 1 and Australians’ enthusiasm for digital innovations which add real value. Financial institutions that are slow to adapt are in danger of being left far behind. With the NPP, the best course of action is to get ahead of the curve and take full advantage of the benefits it will bring.

- 16. The way forward The case for the NPP is compelling. It promises to revolutionise payments in Australia for financial institutions and organisations, as well as for the customers they serve, bringing an array of benefits in the process. Yet to enjoy these benefits, financial institutions need to take immediate action to ensure that they’re ready for the NPP from day one. That’s because the NPP is truly a double-edged sword. While it’s a fantastic opportunity to drive engagement, it also has the potential to be equally damaging to financial institutions that are slow to adapt. As we’ve seen, getting customers to link their mobile number to their transaction account is likely to be crucial. Those who succeed in doing so will be the winners, while those who don’t stand to be further marginalised. The NPP offers a valuable new tool to help win the war for customer relationships. But to be able to use it effectively, financial institutions need to have a plan and strategy in place. With the clock ticking, the time to start is now. For more information about Cuscal’s NPP solution, contact your account manager or visit www.cuscal.com.au/npp. Don’t get left behind 15 / How the NPP can help you win the war for customer relationships

- 17. 16 / How the NPP can help you win the war for customer relationships About Cuscal Cuscal is one of Australia’s leading providers of end-to-end payments solutions, working with more than 100 clients across a diverse range of industries including major names like Australia Post, Bendigo Bank, CUA, ING Direct and Velocity. An authorised deposit-taking institution (ADI) supervised by the Australian Prudential Regulation Authority (APRA), we also own and operate the rediATM network and provide switching and acquiring services for roughly 1/3 of Australia’s ATMs. For more than 40 years our business has been built on a strong foundation of partnering, but never competing with clients. We are the ‘brand behind the brand’, providing dependable, yet innovative payments solutions and cost-effective transactional banking services. In recent years we have helped our clients to operate at the forefront of banking innovation. We were the first to issue a Visa Debit card in Australia and our redi2PAY app was the first HCE-based mobile payment solution in the Asia Pacific region. We are one of the architects of the New Payments Platform (NPP), working alongside Australia’s major financial institutions to design this pivotal banking infrastructure which will revolutionise Australia’s payments industry. The New Payments Platform (NPP) is new infrastructure for Australia’s low-value payments. It will provide Australian businesses and consumers with a fast, versatile, data-rich payments system for making their everyday payments. Twelve leading authorised deposit-taking institutions (ADIs) committed funding for the build and operation of the NPP. These institutions became the founding members of NPP Australia Limited – a new industry mutual company set up by APCA to steer the NPP Program going forward. The 12 founding members of NPP Australia are: •• Australia and New Zealand Banking Group Limited •• Australian Settlements Limited •• Bendigo and Adelaide Bank Limited •• Citigroup Pty Ltd •• Commonwealth Bank of Australia •• Cuscal Limited •• Indue Ltd •• ING Bank (Australia) Limited •• Macquarie Bank Limited •• National Australia Bank Limited •• Reserve Bank of Australia •• Westpac Banking Corporation About the New Payments Platform

- 18. 17 / How the NPP can help you win the war for customer relationships Nathan Churchward Nathan Churchward joined Cuscal in April 2014 as Senior Manager, Payments and is responsible for Cuscal’s payment product management and operations as well as championing product innovation and management training. Nathan brings over 25 years’ experience working in financial services and telecommunications in product design and management roles. His portfolio at Cuscal oversees the management of payment services including Direct Entry, BPAY and chequing products and responsibility for operational delivery. His team is actively working on the development of innovative new payment solutions for Australia’s New Payments Platform (NPP). Throughout his career Nathan has been passionate about successfully identifying consumer behaviour patterns and harnessing eCommerce platforms to maximise operational efficiency. Natalie is an experienced product innovation leader, creative entrepreneur and trained designer who connects the dots between ideas, businesses and people. She uses a customer-centred design approach to uncover market opportunities in the payments industry and commercialise ideas through a product development process. With the development of the New Payments Platform (NPP), and as part of Cuscal’s payments products team, Natalie is currently identifying opportunities where Cuscal can make payments simpler and more meaningful for financial institutions, businesses and their customers. About the co-authors Natalie Yan-Chatonsky

- 19. For more information about Cuscal’s NPP solution contact your account manager or visit www.cuscal.com.au/npp