National Government and Local Government Budget Process

Download as PPTX, PDF3 likes8,386 views

The document discusses the national and local government budget processes in the Philippines. For the national government budget process, it describes the four phases: budget preparation, budget authorization, budget execution, and budget accountability. It provides details on the key documents, players, and steps involved in each phase. For the local government budget process, it similarly outlines the budget preparation and budget authorization phases, identifying the legal basis, key players, and emerging roles for civil society organizations in engaging with and providing inputs to the process at the local level.

![Phase 2 – Budget Authorization

To balance the power of Congress over the purse, the

Constitution clothes the President with veto power (Article VI,

Sec. 27 [2]). The veto may apply to any of the general and

specific provisions of the General Appropriations Act (GAA) as

well as the budget re-alignments introduced by Congress.

Presidential veto, however, may be overturned by Congress by

a three-fourths vote of its members.](https://image.slidesharecdn.com/finalpptforedad304-221018132658-4d6c0c6b/85/National-Government-and-Local-Government-Budget-Process-18-320.jpg)

![Legal Basis of Budget Preparation

Upon receipt of the statements of income and expenditures from the

treasurer, the budget proposals of the heads of departments and

offices and the estimates of income and budgetary ceilings from the

local finance committee, the local chief executive shall prepare the

executive budget for the ensuing year in accordance with the

provisions of [Title V, Book II of RA No. 7160] (Section 318, RA No.

7160).](https://image.slidesharecdn.com/finalpptforedad304-221018132658-4d6c0c6b/85/National-Government-and-Local-Government-Budget-Process-30-320.jpg)

![Emerging Roles of CSOs in the Budget

Authorization Phase

ACTIVITY LGU ROLES CSO ROLES

1. DELIBERATE ON THE BUDGET The

Sanggunian shall consider the executive

budget as a priority measure which shall

take precedence over all other pending

and proposed measures. As a rule, all

Sanggunian sessions shall be open to

the public, unless otherwise provided by

law (Article 105 [b], IRR of RA No.7160).

Sanggunian to post notice of budget

deliberation schedule in three (3)

conspicuous places at least seven (7)

days before the conduct of said

activity. Invite accredited CSOs to

attend and provide inputs during the

budget deliberation sessions,

including committee hearings.

Observing the Internal Rules of

Procedure (IRP) of the

Sanggunian, the accredited CSOs

may:

a. Provide inputs on sectoral

concerns; and

b. Raise questions on changes in

the Executive Budget not

found in the approved AIP.

2. AUTHORIZE THE ANNUAL BUDGET

The Sanggunian authorizes the annual

budget through an Appropriation

Ordinance (AO).

Sanggunian may allow accredited

CSOs to observe the voting for the

enactment of the AO.

Accredited CSOs to observe the

voting conducted by the

Sanggunian.](https://image.slidesharecdn.com/finalpptforedad304-221018132658-4d6c0c6b/85/National-Government-and-Local-Government-Budget-Process-40-320.jpg)

![Emerging Roles of CSOs in the Budget

Authorization Phase

ACTIVITY LGU ROLES CSO ROLES

4. POST THE APPROPRIATION

ORDINANCE The Sanggunian is required

to post the AO, in Filipino, English and

the local dialect, in a bulletin board at the

entrance of the provincial capitol or city,

or municipal hall, as the case may be, and

in at least two (2) other conspicuous

places in the local government unit

concerned (Section 59 [a and b], RA No.

7160).

Comply with the Full Disclosure Policy

pursuant to existing DILG issuances.

Comply with the posting requirement

under Section 59 (a and b), RA No. 7160.

Monitor the posting of the

approved AO, and assist in

making this known to the

public.](https://image.slidesharecdn.com/finalpptforedad304-221018132658-4d6c0c6b/85/National-Government-and-Local-Government-Budget-Process-42-320.jpg)

![Emerging Roles of CSOs in the Budget

Execution Phase

ACTIVITY LGU ROLES CSO ROLES

3. PREPARE CASH PROGRAM AND

FINANCIAL AND PHYSICAL

PERFORMANCE TARGETS The Local

Treasurer shall prepare the Cash Program.

The [LFC] / Department Heads shall

prepare the Summary of Financial and

Physical Performance Targets for the

entire year. The detailed financial and

performance targets present the

quarterly breakdown of the financial

allocation needed to accomplish a

specific level of target.

Post information on the following: a.

Cash Program b. Financial and Physical

Performance Targets in three (3)

conspicuous places in the LGU within

twenty (20) days after the end of each

quarter.

Monitor the LGU compliance

on the preparation of cash

program and financial and

physical performance targets.

Inform beneficiaries and

communities concerned of the

information through tri-media

or conduct meetings with the

beneficiaries and communities

concerned](https://image.slidesharecdn.com/finalpptforedad304-221018132658-4d6c0c6b/85/National-Government-and-Local-Government-Budget-Process-55-320.jpg)

National Government and Local Government Budget Process

- 1. National Government Budget Process and Local Government Budget Process Prepared by: Guiller A. Ellomer Western Mindanao State University College of Teacher Education Webinar Series - 4

- 2. ACTIVITY: “NAME THE PICTURE” CATEGORY: Philippine Government Seal =

- 3. ACTIVITY: “NAME THE PICTURE” CATEGORY: Philippine Government Seal =

- 4. ACTIVITY: “NAME THE PICTURE” CATEGORY: Philippine Government Seal =

- 5. ACTIVITY: “NAME THE PICTURE” CATEGORY: Philippine Government Seal =

- 6. The National Government Budget Process National government budgeting is a continuing cycle – that is, while the current year’s budget is being spent (and accounted for) by implementing agencies, the budget for the ensuing year is simultaneously being prepared by the Executive then passed on to Congress for review and approval.

- 8. Phase 1 - Budget Preparation The Executive through the Development Budget Coordination Committee (DBCC) determines the government priorities and sets macroeconomic and fiscal targets. After deciding on the macroeconomic parameters, the Department of Budget and Management (DBM) issues the Budget Call. This document contains the policy guidelines and procedures in preparing budget proposals i.e., budget priorities, agency budget ceilings, budget forms/annexes and budget calendar.

- 9. Budget of Expenditures and Sources of Financing (BESF) reflects three-year budgets (i.e. previous, current and immediately succeeding year) broken down by sector, item of expenditure, agency allocation and regional distribution. It presents the sources of financing consisting of revenues from tax and non-tax sources, loans and grants.

- 10. National Expenditure Program (NEP) presents the proposed budget allocation by agency, and spells out the General and Special Provisions1 or the rules that shall apply in the implementation of the Appropriations Law. In line with current reforms in the budgeting system, the NEP for 2014 incorporates data previously contained in the Organizational Performance Indicator Framework (OPIF)—e.g., the agency mandates, key result areas, major final outputs (MFOs), performance targets and indicators.

- 11. Details of the Budget is an accompanying document to the National Expenditure Program (NEP) that presents the specific allocations by agency, by program/activities/projects (PAPs), and by expense class (i.e., personal services (PS), maintenance and other operating expenses (MOOE), and capital outlay (CO).

- 12. Staffing Summary gives information on the personnel complement (permanent and filled positions) of every national government agency covering a three-year period, and the corresponding budget for such positions. This book also shows the distribution of permanent positions by salary grade.

- 13. President’s Budget Message provides an overview of the administration’s budget policy thrusts, and the dimensions of the proposed budget.

- 14. Phase 2 – Budget Authorization The budget authorization phase is the primary avenue where the legislature exercises its power of the purse—i.e., Congress determines the appropriateness of budgetary allocation and decides whether a particular program should be continued or discontinued.

- 15. In the exercise of its Constitutional mandate, Congress must ensure that: (i) the government has the capacity to raise its set revenue targets, (ii) the budget deficit will be kept at a level that is not detrimental to the economy and the society as a whole, and (iii) every peso spent will produce the intended outcomes. Hence, agency officials are called upon to justify their budget requests on the basis of past spending decisions and to present results of operations/service delivery.

- 16. Phase 2 – Budget Authorization The arduous task of scrutinizing the budget is initially done at the House of Representatives as stipulated in Article VI, Section 24 of the Constitution. Upon receipt of the six (6) budget books, the Committee on Appropriations and its subcommittees conduct marathon hearings on the proposed budget. Thereafter, the Committee endorses a General Appropriations Bill for plenary deliberation. Congressional debates over the national budget are made accessible to interested parties.

- 17. Phase 2 – Budget Authorization The approved House version of the General Appropriations Bill (GAB) is then submitted to the Senate for review/scrutiny.3 Just like any other legislative measure, the GAB passes through a bicameral conference committee which reconciles the differences between the House and Senate versions. The bicameral committee report is then ratified by both houses and sent to the President for signature.

- 18. Phase 2 – Budget Authorization To balance the power of Congress over the purse, the Constitution clothes the President with veto power (Article VI, Sec. 27 [2]). The veto may apply to any of the general and specific provisions of the General Appropriations Act (GAA) as well as the budget re-alignments introduced by Congress. Presidential veto, however, may be overturned by Congress by a three-fourths vote of its members.

- 19. Phase 2 – Budget Authorization Should Congress fail to pass the budget law before the end the year, the government is authorized to operate under a reenacted budget until a new appropriations law is approved (Article VI, Sec. 25).

- 20. Phase 2 – Budget Authorization (Automatic and Continuing Appropriations) Automatic appropriations are appropriations programmed annually or for some other period prescribed by law, by virtue of outstanding legislation that does not require periodic action by Congress. This type of appropriations includes expenditures authorized under the following laws: (a) Presidential Decree (PD) 1967, RA 4860 and RA 245 as amended for the servicing of domestic and foreign debts; (b) Commonwealth Act 168 and RA 660, for the retirement and insurance premiums of government employees; (c) PD 1177 and EO 292, for net lending to government corporations; and (d) PD 1234, for various special accounts and funds.

- 21. Phase 2 – Budget Authorization (Automatic and Continuing Appropriations) Continuing Appropriations, on the other hand, are appropriations available to support obligations for a specified purpose or project such as multi-year construction of projects requiring the incurrence of obligations even beyond the budget year—e.g., RA 8150 or the Public Works Act of 1995, and RA 6657 and RA 8532 which set funds specifically for the Agrarian Reform Program (ARP).

- 22. Phase 3 – Budget Execution The fiscal year covered by the budget execution phase starts on 1 January of any given year and ends on the last day (31 December) of the same year. To be effective, budget execution must embrace the following principles: (a) implementation of the approved budget with as little distortion as possible, (b) utilization of resources with frugality, efficiency and transparency, and (c) realization of developmental goals set in the Medium-Term Development Plan.

- 23. Phase 3 – Budget Execution Previously, releases of allotment were programmed and prioritized by the DBM in consultation with agencies concerned. Agency Budget Matrix (ABM) and Allotment Release Program (ARP) would have to be authorized before agencies could enter into contracts with suppliers of goods and services. Effective 2014, the DBM adopts a Budget-as Release-Document policy wherein budgets of agencies are considered “released” as soon as the GAA is passed. However, a Special Allotment Release Order (SARO) will still be required for transactions that need prior clearance such as lump- sum budget items (Budget Message 2014).

- 24. Phase 3 – Budget Execution In order to make payments for valid obligations, Notices of Cash Allocation (NCAs) are issued by the DBM to implementing agencies/departments. Unsettled obligations during the year are reported as accounts payable for the ensuing year. Meanwhile, paid vouchers and their supporting documents are sent to the Commission on Audit for review.

- 25. Phase 4 – Budget Accountability Budget Accountability may be the last but is definitely not the least important segment of the budget process. Sharing this responsibility are the oversight bodies— DBM, COA and Congress.

- 26. Phase 4 – Budget Accountability Budget oversight is undertaken by DBM in relation to the periodic release of allotments and notices of cash allocations. Meanwhile, the COA examines all government transactions and use of public resources to ensure that all disbursements are duly authorized and beneficial to government. Audit findings are expected to feed into the other phases of the budget, particularly budget preparation and authorization phases.

- 27. Phase 4 – Budget Accountability Congressional budget oversight is usually done alongside budget authorization. During budget hearings, agencies report on their accomplishments and are made to explain any questions on program implementation or use of agency resources.

- 28. Local Government Budget Process

- 29. Budget Preparation Phase Budget preparation is the first phase of the local budget process. It involves cost estimation per PPA, preparation of budget proposals, executive review of budget proposals, and preparation of the LEP and the Budget Message. This phase starts with the issuance of the Budget Call, and ends with submission of the Executive Budget to the Sanggunian on or before October 16 of each year.

- 30. Legal Basis of Budget Preparation Upon receipt of the statements of income and expenditures from the treasurer, the budget proposals of the heads of departments and offices and the estimates of income and budgetary ceilings from the local finance committee, the local chief executive shall prepare the executive budget for the ensuing year in accordance with the provisions of [Title V, Book II of RA No. 7160] (Section 318, RA No. 7160).

- 31. Key Players in Budget Preparation Local Chief Executive (LCE) Local Finance Committee (LFC) Local Treasurer Local Budget Officer (LBO) Local Planning and Development Coordinator (LPDC) Local Accountant Heads of Departments and Offices/Heads of LEEs/Pus CSOs and the Private Sector Group -

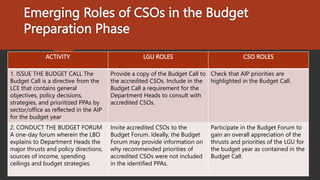

- 32. Emerging Roles of CSOs in the Budget Preparation Phase ACTIVITY LGU ROLES CSO ROLES 1. ISSUE THE BUDGET CALL The Budget Call is a directive from the LCE that contains general objectives, policy decisions, strategies, and prioritized PPAs by sector/office as reflected in the AIP for the budget year Provide a copy of the Budget Call to the accredited CSOs. Include in the Budget Call a requirement for the Department Heads to consult with accredited CSOs. Check that AIP priorities are highlighted in the Budget Call. 2. CONDUCT THE BUDGET FORUM A one-day forum wherein the LBO explains to Department Heads the major thrusts and policy directions, sources of income, spending ceilings and budget strategies. Invite accredited CSOs to the Budget Forum. Ideally, the Budget Forum may provide information on why recommended priorities of accredited CSOs were not included in the identified PPAs. Participate in the Budget Forum to gain an overall appreciation of the thrusts and priorities of the LGU for the budget year as contained in the Budget Call.

- 33. Emerging Roles of CSOs in the Budget Preparation Phase ACTIVITY LGU ROLES CSO ROLES 3. PREPARE AND SUBMIT BUDGET PROPOSALS Each Department Head prepares the budget proposals and submits these to the LBO for review and consolidation. He/ She needs to determine the expected outputs for the budget year and estimated costs. LCE to ensure that the Department Heads consulted with accredited CSOs. The Budget Call may already prescribe such requirement. The accredited CSOs sectoral representative may partner with the Department Heads concerned in determining the target beneficiaries and funding requirements for the particular sector. The CSOs may also propose projects for consideration by the Department Heads concerned. In cases where CSOs’ proposed PPAs are not included in the budget, CSOs can request information from the LGU on the reasons for non-inclusion.

- 34. Emerging Roles of CSOs in the Budget Preparation Phase ACTIVITY LGU ROLES CSO ROLES 4. CONDUCT BUDGET HEARINGS The technical budget hearings are conducted by the LFC to validate the revenue sources, PPAs, cost estimates and expected outputs for the budget year. Invite accredited CSOs to the budget hearings in relation to sectoral concerns. Participate in the budget hearings to provide inputs on sectoral concerns. 5. EVALUATE BUDGET PROPOSALS The LFC evaluates all budget proposals using the output and cost criteria. May replicate the best practices of other LGUs in engaging CSOs in LFC. May replicate the best practices of other CSOs in engaging LFC.

- 35. Emerging Roles of CSOs in the Budget Preparation Phase ACTIVITY LGU ROLES CSO ROLES 6. SUBMIT EXECUTIVE BUDGET TO SANGGUNIAN After consolidation of the budget proposal and approval thereof by the LCE, the LGU shall submit the proposed executive budget not later than October 16 16 of the current fiscal year pursuant to Section 318 of RA No. 7160. This is usually done through a State of the Province/City/ Municipality Address (SOPA/ where the LCE presents the proposed Annual Budget to the Sanggunian and other stakeholders. Invite accredited CSOs to the SOPA/SOCA/SOMA. Attend the SOPA/SOCA/ SOMA.

- 36. The Budget Preparation Flow Chart The sequence of activities in preparing the LEP should be synchronized with the mandated deadline for its submission to the Local Sanggunian.

- 37. Budget Authorization Phase Budget Authorization is the second phase in the local budget process. This phase starts from the time the Sanggunian receives the Local Expenditure Program (LEP) submitted by the LCE, and ends with the enactment of the Appropriation Ordinance and approval thereof by the LCE. Authorization of the budget is done through an Appropriation Ordinance enacted by the Local Sanggunian in accordance with the fundamental principle that, “No money shall be paid out of the local treasury except in pursuance of an Appropriation Ordinance or law” (Section 305 (a), RA No. 7160).

- 38. Legal Basis of Budget Authorization On or before the end of the current fiscal year, the Sanggunian concerned shall enact, through an ordinance, the annual budget of the local government unit for the ensuing fiscal year on the basis of the estimates of income and expenditures submitted by the local chief executive (Section 319, RA No. 7160).

- 39. Key Players in Budget Authorization Local Chief Executive Sanggunian Committee on Appropriations/Finance Secretary to the Sanggunian Local Finance Committee Heads of Departments and Offices CSOs and Private Sector Groups

- 40. Emerging Roles of CSOs in the Budget Authorization Phase ACTIVITY LGU ROLES CSO ROLES 1. DELIBERATE ON THE BUDGET The Sanggunian shall consider the executive budget as a priority measure which shall take precedence over all other pending and proposed measures. As a rule, all Sanggunian sessions shall be open to the public, unless otherwise provided by law (Article 105 [b], IRR of RA No.7160). Sanggunian to post notice of budget deliberation schedule in three (3) conspicuous places at least seven (7) days before the conduct of said activity. Invite accredited CSOs to attend and provide inputs during the budget deliberation sessions, including committee hearings. Observing the Internal Rules of Procedure (IRP) of the Sanggunian, the accredited CSOs may: a. Provide inputs on sectoral concerns; and b. Raise questions on changes in the Executive Budget not found in the approved AIP. 2. AUTHORIZE THE ANNUAL BUDGET The Sanggunian authorizes the annual budget through an Appropriation Ordinance (AO). Sanggunian may allow accredited CSOs to observe the voting for the enactment of the AO. Accredited CSOs to observe the voting conducted by the Sanggunian.

- 41. Emerging Roles of CSOs in the Budget Authorization Phase ACTIVITY LGU ROLES CSO ROLES 3. APPROVE THE A P P R O P R I A T I O N ORDINANCE The AO enacted by the Sanggunian shall be presented to the LCE for approval, in which case he shall affix his signature in every page thereof. Otherwise, the LCE may exercise veto power. LCE to consider formal comments and observations of accredited CSO, if any, subject to the fifteen (15) and ten (10) days reglementary period for approval, for provinces, and cities or municipalities, respectively, per Section 54 (b), RA No. 7160. Accredited CSOs to inform the LCE in writing of their observation in the deliberation and enactment of AO, subject to the applicable reglementary period.

- 42. Emerging Roles of CSOs in the Budget Authorization Phase ACTIVITY LGU ROLES CSO ROLES 4. POST THE APPROPRIATION ORDINANCE The Sanggunian is required to post the AO, in Filipino, English and the local dialect, in a bulletin board at the entrance of the provincial capitol or city, or municipal hall, as the case may be, and in at least two (2) other conspicuous places in the local government unit concerned (Section 59 [a and b], RA No. 7160). Comply with the Full Disclosure Policy pursuant to existing DILG issuances. Comply with the posting requirement under Section 59 (a and b), RA No. 7160. Monitor the posting of the approved AO, and assist in making this known to the public.

- 44. Budget Review Phase Budget Review is the third phase in the local budget process. Its primary purpose is to determine whether the Appropriation Ordinance has complied with the budgetary requirements and general limitations set forth in the Local Government Code of 1991, as well as provisions of other applicable laws. It starts from the time the reviewing authority receives the Appropriation Ordinance for review and ends with the issuance of the review action.

- 45. Legal Bases of Budget Review The Department of Budget and Management shall review ordinances authorizing the annual or supplemental appropriations of provinces, highly-urbanized cities, independent component cities, and municipalities within the Metropolitan Manila Area in accordance with Section 327 of RA No. 7160 (Section 326 of RA No. 7160). The Sangguniang Panlalawigan shall review the ordinance authorizing annual or supplemental appropriations of component cities and municipalities in the same manner and within the same period prescribed for the review of other ordinances (Section 327, RA No.7160).

- 46. Key Players in Budget Review Secretary to the Sanggunian Sangguniang Panlalawigan Provincial Finance Committee Department of Budget and Management Regional Office CSOs and Private Sector

- 47. Emerging Roles of CSOs in the Budget Review Phase ACTIVITY LGU ROLES CSO ROLES 1. ISSUE THE REVIEW ACTION The reviewing authority may declare the AO as: a) operative in its entirety; b) operative operative in its entirety, subject to conditions; c) inoperative in its entirety; or d) inoperative in part. If the arrangement is allowed in the terms of engagement between the LGU and CSO, the LGU may furnish copy of the review letter to the accredited CSOs. Check the LGU compliance with the review findings.

- 48. Reglementary Period of Review The Appropriation Ordinance of provinces, highly-urbanized cities, independent component cities, component cities and municipalities shall be reviewed within 90 days from receipt of copies of such ordinances (Section 327, RA No. 7160).

- 49. The Budget Review Flow Chart It shows the sequence of activities from the time the Secretary to the Sanggunian submits the approved Appropriation Ordinance to the reviewing body/office until the same is returned together with the budget review action to the Sanggunian concerned through the LCE.

- 50. The Budget Execution Phase The execution of the budget in accordance with existing rules, laws and regulations is the fourth phase of the budget process in local governments. After the usual recording of appropriations in the proper registries, the execution of the budget involves the release of allotments, the certification of available appropriations and cash, the recording of actual obligations and disbursements of funds for approved PPAs and the delivery of goods and services to target clients in the most efficient, effective, economical and ethical way. A critical aspect of this phase is the collection of funds to ensure that cash is available for payment of obligations and further ensuring that disbursements do not exceed appropriations. While seemingly a separate activity, the collection and/or receipt of revenues are considered an integral part of Budget Execution.

- 51. Legal Bases of Budget Execution The fundamental principles governing all financial transactions in local governments are covered in Section 305 of RA No. 7160. The responsibility, however, for the execution of authorized annual and supplemental budgets shall be vested upon the Local Chief Executive (Section 320 of RA No. 7160). The use of appropriated Funds pursuant to Section 336 of RA No. 7160 shall be exclusively for the specific purpose for which they have been appropriated. Another legal basis in Budget Execution is the Certification requirement before local funds are utilized. Section 344 of R.A. No.7160 provides that “No money shall be disbursed unless the local budget officer certifies to the existence of appropriation that has been legally made for the purpose, the local accountant has obligated said appropriation, and the local treasurer certifies to the availability of funds for the purpose. Finally, disbursements of local funds shall be made in accordance with the ordinance authorizing the annual or supplemental appropriations even without the prior approval of the Sanggunian concerned (Section 346 of R.A. No. 7160).

- 52. Key Players in Budget Execution Local Chief Executive (LCE) Vice Governor/ Vice Mayor Local Budget Officer (LBO) Local Treasurer Local Accountant Local Planning and Development Coordinator (LPDC) Department Head Civil Society Organizations (CSOs)/Private Sector Groups

- 53. Emerging Roles of CSOs in the Budget Execution Phase ACTIVITY LGU ROLES CSO ROLES 1. RELEASE THE ALLOTMENTS (LBM/ARO) The Local Budget Matrix (LBM) is issued to effect the comprehensive release of allotment for a Department/ Office. Release of reserve amounts shall be effected through the use of Allotment Release Order/s (ARO/s). Post information on allotment releases (LBM/SAROs) in three (3) conspicuous places in the LGU within twenty (20) days from the release of the allotment. Monitor the LGU compliance on the release of allotments. Inform beneficiaries and communities concerned of the release of allotments through tri-media or conduct meetings with the beneficiaries and communities concerned.

- 54. Emerging Roles of CSOs in the Budget Execution Phase ACTIVITY LGU ROLES CSO ROLES 2. POST THE STATEMENT OF RECEIPTS AND EXPENDITURES IN THE LGU WEBSITE The LGU shall post the monthly Statement of Receipts and Expenditures within ten (10) days after the end of the month pursuant to Section 513 of RA No. 7160 Post information on receipts and expenditures in three (3) conspicuous places in the LGU within ten (10) days after the end of the month pursuant to Section 513 of RA No. 7160; and within twenty (20) days after the approval by the LCE of the Annual Report of Receipts and Expenditures as required under the Full Disclosure Policy of the DILG. Monitor the postings as required under RA No. 7160 and the Full Disclosure Policy of the DILG. Advocate for the citizen’s awareness of posted information through trimedia.

- 55. Emerging Roles of CSOs in the Budget Execution Phase ACTIVITY LGU ROLES CSO ROLES 3. PREPARE CASH PROGRAM AND FINANCIAL AND PHYSICAL PERFORMANCE TARGETS The Local Treasurer shall prepare the Cash Program. The [LFC] / Department Heads shall prepare the Summary of Financial and Physical Performance Targets for the entire year. The detailed financial and performance targets present the quarterly breakdown of the financial allocation needed to accomplish a specific level of target. Post information on the following: a. Cash Program b. Financial and Physical Performance Targets in three (3) conspicuous places in the LGU within twenty (20) days after the end of each quarter. Monitor the LGU compliance on the preparation of cash program and financial and physical performance targets. Inform beneficiaries and communities concerned of the information through tri-media or conduct meetings with the beneficiaries and communities concerned

- 56. Emerging Roles of CSOs in the Budget Execution Phase ACTIVITY LGU ROLES CSO ROLES 4. OBLIGATE AND DISBURSE FUNDS FOR IMPLEMENTATION OF PPAS - PROCUREMENT PROCESS Procurement Process To enhance the transparency of the process, the BAC shall, in all stages of procurement process, invite, in addition to the representative of Commission on Audit, at least two (2) observers to sit in its proceedings, one (1) from a duly recognized private group in a duly recognized private group in a sector or discipline relevant to the procurement at hand. Invite accredited CSOs, if qualified as observers, in the procurement process at least three (3) calendar days before each procurement activities in compliance with the Government Procurement Reform Act, RA No. 9184. Attend as observer in the procurement process and carry out the responsibilities provided under Section 13.4 of the IRR of RA No. 9184. May use as reference the GPPBissued Procurement Observers Guide (POG).

- 57. Emerging Roles of CSOs in the Budget Execution Phase ACTIVITY LGU ROLES CSO ROLES PPA Implementation The responsibility for the execution of the annual and supplemental budget shall be vested primary in the LCE concerned. In the implementation of PPAs, the following must be ensured: • standards of service • quality of work • timelines of implementation pricing of goods, contracts and services • PPA fund release/ utilization • proper delivery to target beneficiaries Invite accredited CSOs to spot check or track implementation of ongoing projects. (This may be differentiated from the monitoring activity in the Budget Accountability Phase which is done on scheduled periods, i.e., quarterly, mid-term and annual, and aimed at comp Participate in the spot check or tracking of implementation of ongoing projects and prepare Project Monitoring Report for submission to the LCE. (Annex B)

- 58. Emerging Roles of CSOs in the Budget Execution Phase ACTIVITY LGU ROLES CSO ROLES 5. ADJUST CASH PROGRAM FOR SHORTAGES AND OVERAGES The LFC, through the Local Treasurer, shall use the results of the cash flow analysis as basis for adjusting the Cash Program and the financial and physical targets. Post information on adjusted Cash Program in three (3) conspicuous places in the LGU within twenty (20) days after the end of each quarter Monitor the LGU compliance on the preparation of adjusted cash program, and financial and physical performance targets.

- 59. Emerging Roles of CSOs in the Budget Execution Phase ACTIVITY LGU ROLES CSO ROLES 6. PROVIDE CORRECTIVE ACTIONS FOR NEGATIVE DEVIATIONS The LFC shall compare the actual performance in both the financial and physical accomplishments visà-vis the targets for the quarter. For variances, Department Heads concerned shall take corrective actions or prepare necessary adjustments to catch up with the plans for the year. Render reports on actions taken to address negative deviations. Provide copies of catch-up plans to parties concerned. Partner with accredited CSOs in addressing service gaps and acknowledge contribution of CSOs. Monitor appropriate interventions and measures taken by the LGU on negative deviations. Assist the LGU in implementing appropriate interventions on negative deviations, which may include providing possible support for service and/or resource gaps in the delivery of services.

- 60. The Budget Execution Flow Chart The budgetary accounts to be maintained during the budget execution process include the following: l Appropriations l Allotments l Obligations

- 61. The Budget Accountability Phase Budget accountability is the last and final phase of the budget process. Budget Accountability, in simple terms, is accounting for the budget. It involves the use of a management control techniques to assist in tracking receipts of income/revenues and controlling expenditures. This mechanism provides a venue for the LCE, Local Sanggunian and stakeholders to be continuously informed of the status of implementation of PPAs being funded by public funds. It covers the monitoring and analysis of all financial transactions, the recording of budgetary accounts in the registries, recording in the books of accounts of all receipts and expenditures and financial reporting of their current status. An integral part of accountability is the evaluation of the financial and physical performance of the LGU. This review and assessment of performance is necessary to introduce improvements and reforms to make the budget more transparent to the people and stakeholders.

- 62. Legal Bases of Budget Accountability Section 340 of RA No. 7160 provides that “any officer of the LGU whose duty permits or requires the possession or custody of local government funds shall be accountable and responsible for the safekeeping thereof in conformity with the provisions of this Title. Other local officers, who, though not accountable by the nature of their duties, may likewise be held accountable and responsible for local government funds through their participation in the use or application thereof.” Section 305 of RA No. 7160 also provides that “Fiscal responsibility shall be shared by all those exercising authority over the financial affairs, transactions, and operations of the local government unit

- 63. Key Players in Budget Accountability Local Chief Executive Local Treasurer Local Accountant Local Budget Officer Planning and Development Coordinator Heads of Departments/Offices Local Finance Committee CSOs and Private Sector Organizations

- 64. Emerging Roles of CSOs in the Budget Accountability Phase ACTIVITY LGU ROLES CSO ROLES 1. MONITOR OUTPUTS AND RESULTS OF PPAs The appropriations recorded in the books shall be compared with the actual collections and disbursements for the same period. Expenditures are tracked and monitored vis-à-vis the outputs and accomplishments. Invite accredited CSOs to participate in the local project monitoring activities. Post financial information in three (3) conspicuous places in the LGU within twenty (20) days after the end of each quarter. Invite accredited CSOs in the midyear and year-end assessment of the overall performance of the LGU. Invite accredited CSO in the impact assessment of the programs and projects, and the overall performance of the LGU. Make use of available and existing monitoring tools such as the Citizens Satisfaction Report Card (from CODE-NGO) and the LGU Fiscal Sustainability Scorecard (from BLGF). Actively participate in the local project monitoring activities. Enhance CSOs own technical capability in project monitoring. Monitor PPA implementation and check on the following: • standards of service • quality of work • timeliness of implementation • pricing of goods, contracts, and services • PPA fund release/ utilization • proper delivery to target beneficiaries Provide recommendations based on monitoring results. Organize citizens’ fora with the LGU to provide feedback to the community. Actively participate in the impact assessment of programs and projects and of the overall performance of the LGU.

- 65. The Budget Accountability Flow Chart Budget accountability is accounting for the local budget, which involves three (3) steps: Monitor receipts and expenditures Submit Accountability Reports Evaluate Performance of each Department/Office

- 66. References Congressional Policy and Budget Research Department, August 2013, House of Representative, A Legislator’s Guide in Analyzing the National Budget, 2nd Edition Budget Operations Manual of Local Government Units, 2016 Edition

- 67. Thank you for Listening!

Editor's Notes

- #21: Automatic and Continuing Appropriations. Aside from new appropriations, there are two other sources of appropriations under which the government operates—i.e., automatic and continuing appropriations. Automatic appropriations are appropriations programmed annually or for some other period prescribed by law, by virtue of outstanding legislation that does not require periodic action by Congress. This type of appropriations includes expenditures authorized under the following laws: (a) Presidential Decree (PD) 1967, RA 4860 and RA 245 as amended for the servicing of domestic and foreign debts; (b) Commonwealth Act 168 and RA 660, for the retirement and insurance premiums of government employees; (c) PD 1177 and EO 292, for net lending to government corporations; and (d) PD 1234, for various special accounts and funds.

- #61: Appropriation: an authorization made by ordinance, directing the payment of goods and services from local government funds under specified conditions or purposes. Allotment: an authorization issued by the Local Chief Executive (LCE) to a Department/Office of the LGU which authorizes it to incur obligations for a specific amount within its appropriation. Obligation: the specific amount within the allotment which is committed to be paid by the LGU for any lawful expenditure made by an accountable officer for and in behalf of the LGU concerned.