presentationonprimarymarket-240305050959-a5c5059c.pdf

- 1. PRESENTATION ON PRIMARY MARKET Basavaraj M. Naik, M.Com, NET, KSET Teaching Assistant Department of Commerce Rani Channamma University, SRGFCC, Belagavi

- 2. WHAT IS FINANCIAL MARKET? • Any place or system that provides buyers and sellers the means to trade financial instruments, including bonds, equities, the various international currencies, and derivatives.

- 3. MEANING OF PRIMARY MARKET • In a Primary Market, securities are created for the first time for investors to purchase. New securities are issued in this market through a stock exchange, enabling the government as well as companies to raise capital.

- 4. • In other words, The primary market is where newly issued securities are sold for the first time by issuers directly to investors. • Importance: It facilitates capital formation by enabling companies to raise funds for business expansion, development, or debt repayment.

- 5. FEATURES OF PRIMARY MARKET • Market for new long term equity capital - Market place where securities are sold for the first time • Securities are issued by the company- Securities are issued by the company directly to investors • The money & issues new security certificates- The company receives the money and issues new security certificates to the investors • Setting up new business- Primary issues are used by the company for the purpose of setting up new business or for expanding or modernizing the existing business. • Capital Formation- Attractive issue to the potential investors and with this company can raise capital at lower costs

- 6. CAPITAL FORMATION • Capital formation is the net accumulation of capital goods, such as equipment, tools, transportation assets, and electricity, during an accounting period for a particular country. Generally, the higher the capital formation of an economy, the faster an economy can grow its aggregate income.

- 7. SIGNIFICANCE /ROLE OF PRIMARY MARKET • Capital growth by enabling individuals- Convert savings into investments • Issue new stocks to raise money directly • Channel for Govt. to raise funds- to raise funds from the public to finance public sector projects, like public transport etc • Capital formation • Liquidity- Securities issued in PM can be immediately sold in secondary market. • Reduction in cost- Prospectus containing all the details about the securities are given to the investors hence it helps in reducing the cost in searching and assessing the individual securities. • Business expansion- Leads growth for domestic and foreign companies.

- 9. 1. ORIGINATION Primary market deals with the origin of new issue. The proposal is analysed in terms of the nature of the security, the size of the issue, timings of the issue and floatation method of the issue. • In primary market, origination means to investigate, evaluate and procedure new project proposals. It initiates before an issue is present in the market. It is done with the help of merchant bankers. The merchant bankers can be banks, financial institutions, private investment firms, etc.

- 10. 2. UNDERWRITING • Underwriting is a kind of guarantee undertaken by an institution. It is a method whereby the guarantor makes a promise to the stock issuing company the he would purchase a certain specific number of shares in the event of their not being invested by the public.

- 11. 3. DISTRIBUTION • Distribution means the function of sale of shares and debentures to the investors. Distribution Job is given to brokers and dealers. The brokers or agents maintain direct contact with the supreme investors. They maintain regular lists of clients and directly contact them for purchase and sale of securities.

- 12. ISSUE OF CAPITAL • Issue of Share Capital is the total value of shares that a company has issued to its shareholders. The value of Issued Share Capital can fluctuate based on the market value of the shares. Issued Share Capital is an important measure of a company's financial health and its ability to raise capital.

- 13. METHODS OF ISSUING SECURITIES IN PRIMARY MARKET,

- 14. 1. Public Issue • One of the most common methods of issuing securities to the public at large is Public Issue. Generally, this process is undertaken by companies to raise funds from the capital market that can be used to expand their business, pay off debt, or any other reasons. You must note that these securities are further made available to trade on the stock exchanges. • A) Initial Public Offer(IPO): Fresh issue of shares or selling existing securities by an unlisted company for the first time is known as IPO. Listing and trading of securities of a company takes place in IPO. When a (unlisted) company makes a public issue for the first time and gets its shares listed on stock exchange, the public issue is called IPO.

- 15. B. FURTHER PUBLIC OFFER (FPO) • Also known as Follow on Offer, FPO refers to the process of issuing securities to the general public by the company which is already listed on the stock exchange. This is done with the aim to raise additional funds. In Simple, when a listed company makes another public issue to raise capital, it is called FPO. Both IPO and FPO can be undertaken by the company via 2 methods as mentioned below: a.Fresh Issue: It means the issuance of new securities in the company and selling of these new securities to the investors. b.Offer for Sale (OFS): The selling of shares by promoters/investors of the company in order to reduce their stake is known as OFS.

- 16. 2. RIGHTS ISSUE • The offer to the company’s existing shareholders to buy new shares of the company at a discounted price is known as a Rights Issue. It invites its existing shareholders to avail fresh shares in the proportion of their holding in order to raise additional capital without going to the public at large.

- 17. 3. BONUS ISSUE Bonus Issue is when a company issues fully paid additional shares to the existing shareholders in proportion to their existing holding for free. The issue is made by a company from its free reserves or securities premium.

- 18. 4. PRIVATE PLACEMENT • When a company sells its stocks or bonds directly to a group of people (private investors or institutions) instead of offering it to the general public is known as Private Placement. A company can raise funds quickly via this distribution strategy as compared to raising capital through fresh issues as the regulatory requirements are significantly less.

- 19. A. PREFERENTIAL ALLOTMENT • The process in which the securities are allotted to a group of people/investors on a preferential basis at a specific price is known as a preferential allotment. Listed as well as unlisted companies can issue shares/convertible securities to a select group of investors via this strategy. B. Qualified Institutional Placement (QIP) • A type of private placement in which a company issues shares of debentures (fully or partly convertible) or any other kind of marketable securities not including warrants (which are convertible) to Qualified Institutional Buyers (QIB) is known as Qualified Institutional Placement. Herein, QIBs are investors who have substantial financial knowledge and expertise to invest in the capital market. A few of the QIBs are mentioned here, Foreign Institutional Investors registered with SEBI, MFs, Public Financial Institutions, Insurers, Scheduled Commercial Banks, etc.

- 20. INTERMEDIARIES/PLAYERS IN NEW ISSUE MARKET 1. Merchant Bankers: Merchant bankers act as intermediaries between their clients and financial markets, helping clients to raise capital, manage risks, and invest wisely. Merchant banking services include underwriting, loan syndication, mergers and acquisitions, portfolio management, corporate restructuring, and project financing.

- 21. 2. REGISTRARS: • Registrars are intermediaries who undertake all activities connected with the new issue management such as collecting applications from investors, keeping all records with regards to applications received, money received etc., assisting the companies in the allotment of shares and helping to dispatch all letters, certificates etc., to investors.

- 22. 3. COLLECTING & CO-ORDINATING BANKERS The collecting bankers collect the subscriptions in cash, cheques etc. The coordinating bankers collect information on subscriptions and coordinate the collection work. They monitor the work and inform it to the registrars and merchant bankers then and there. 4. UNDERWRITERS: Financial institutions, such as investment banks, that act as intermediaries between issuers and investors. An underwriter's role in a primary marketplace includes purchasing unsold shares if it cannot manage to sell the required number of shares to the public. A financial institution may act as an underwriter, earning a commission on underwriting.

- 23. 5. PORTFOLIO MANAGERS: • The portfolio managers are those who advise or direct or undertake the management or administration of a portfolio of securities on behalf of client as per the agreement with client. 6. Brokers/ Transfer Agents: Transfer agents are those who maintain the record of holders of securities on their own behalf of the companies and deal with all activities connected with the transfer/redemption of such company’s securities.

- 24. PRICING OF ISSUE: • Pricing of issue can refer to the initial price at which a company's shares are offered to the public. It can also refer to the initial cost of a security when it first becomes available for purchase by the public.

- 25. BOOK BUILDING • Book building refers to the process of generating, capturing, and recording investor demand for shares during an Initial Public Offering (IPO), or other securities during their issuance process, in order to support efficient price discovery.

- 26. EXAMPLE • Book building is actually a price discovery method. In this method, the company doesn't fix up a particular price for the shares, but instead gives a price range, e.g. Rs 80- 100. When bidding for the shares, investors have to decide at which price they would like to bid for the shares, for e.g. Rs 80, Rs 90 or Rs 100. They can bid for the shares at any price within this range. Based on the demand and supply of the shares, the final price is fixed. The lowest price (Rs 80) is known as the floor price and the highest price (Rs 100) is known as cap Price.

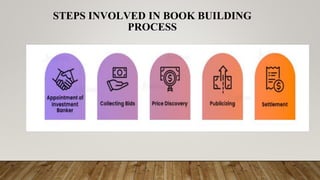

- 27. STEPS INVOLVED IN BOOK BUILDING PROCESS

- 28. Step 1: Appointment of Investment Banker: The main role of this person is to conduct due diligence. The investment banker also proposes a price band for the shares to be sold. Step 2: Collecting Bids: The market participants are asked to submit bids in the second step to purchase the shares. They are asked to submit a bid for the number of shares they are prepared to purchase at various price points. It is suggested that these bids be sent to the investment bankers together with the application fee. It should be highlighted that not a single investment banker is in charge of collecting bids. Instead, the main investment banker can designate sub-agents to use their network specifically for gathering bids from a bigger number of people.

- 29. Step 3: Price Discovery: This is the third step in which lead investment bankers aggregate all the bids, then they begin the process of price discovery. The final price chosen is simply the weighted average of all the bids that have been received by the investment banker. This price is set to be the cut-off price. Step 4: Publicizing: Stock markets all throughout the world demand that businesses disclose the specifics of the bids they received for the sake of transparency. Investment bankers are responsible for running advertising for a specified amount of time that includes information on the bids received for the purchase of shares. Several markets’ authorities also have the option of physically inspecting the bid applications.

- 30. Step 5: Settlement: Finally, shares must be distributed and the application amount that has been credited from the individual bidders must be adjusted. For instance, a call letter requesting payment of the remaining balance must be sent if a bidder offers a lower price than the cut-off price. But, if a bidder placed a bid that was higher than the cut-off, a refund check must be prepared for them. The settlement procedure makes sure that investors are only paid the cut-off amount, not the shares that were sold to them.

- 31. GREEN SHOE OPTION • In security issues, a green shoe option is an over allotment option. In the context of an IPO, it is a provision in an underwriting agreement that grants the underwriter the right to sell investors more shares than originally planned by the issuer if the demand for a security issue proves higher than explained. Over allotment options are known as green shoe options because in 1919, Green shoe manufacturing company was first to issue this type of option. A green shoe option provide additional price stability to a security issue because the underwriter has the ability to increase supply smooth out price fluctuations.

- 32. GUIDELINES FOR THE GREEN SHOE OPTION PROCESS 1. The issuing company can only lend 15% shares out of the total offer size for the green shoe option process. 2. The underwriter or the stabilizing agent can exercise the green shoe share option only within 30 days of the date of IPO. 3. The underwriter may invoke the green shoe share option either in part or in full, i.e. the underwriter can buy back either all or a part of the shares as part of the green shoe share option depending on the price action of the underlying stock relative to the offer price. Question - *list out any 5 companies they entered for Green shoe option

- 33. PROCEDURE FOR NEW ISSUE • 1. Approval from the Board of Directors. • 2. The Firm must file a Registration Statement with the SEBI. This statement contains financial information, financial history and plans for future. • 3. The SEBI studies the registration statement during a waiting period. During this time the firm may distribute copies of a preliminary prospectus of the potential investors. This is called Red Herring because bold red letters are printed on the cover. The company cannot sell the securities during the waiting period. • 4. A registration statement will become effective on the 20th day after its filing unless the SEBI sends a letter of comment suggesting changes. • 5. On the effective date of the registration, a price is determined and a full fledged selling effort starts. • 6. A final prospectus must accompany the delivery of securities or confirmation of sale whichever comes first.

- 34. SEBI GUIDELINES FOR ISSUES IN PRIMARY MARKET • 1. Initial Public Offering & Primary Market- SEBI (Disclosure& Investors Protection) Rules and Regulation, 24th Feb., 2009. • 1. IPO of issue size up to 5 times of pre-issue, shall be allowed only to those companies having consistent track record of making profit at least for 5 years. • 2. For issue above Rs. 100 crores book building route has been made compulsory for comp. making IPO. • 3. Time for finalizing the allotment of shares and refund has been reduced from 30 to 15 days. • 4. Issue shall open within 12 months from the date of issue of observation letter by SEBI. • 5. Should disclose price band at least 2 working days before opening of bid by announcement in all newspapers in which pre-issue advt. was released.

- 35. II. SEBI GUIDELINES TO MERCHANT BANKERS (SEBI MB RULES & REGULATIONS 2006.) • The SEBI has laid down the following guidelines regarding duties and obligations of the merchant bankers: • 1. Merchant bankers shall have to be compulsorily registered with the SEBI. The following conditions have to be fulfilled for registration by the SEBI: • - Merchant bankers must have a minimum net worth of 5 crore. Those acting only as portfolio managers must have a net worth of 50 lakh. Those acting only as underwriters must have a net worth of 20 lakh. • - Merchant bankers should have adequate and necessary infrastructure for effective performance of their activities. • - Merchant bankers should have expertise in the areas of finance, law and management and are not involved in any litigation relating to the securities market. • - Every merchant banker shall pay a sum of 5 lakh as registration fees within 15 days of receipt of intimation from the SEBI.

- 36. • 2. The merchant banker shall enter into agreement with the issuing company, spelling out their mutual rights, obligations and liabilities pertaining to the issue. A copy of the agreement is to be submitted to the SEBI at least one month before opening of the issue for subscription. • 3. The merchant banker will have to undertake a minimum underwriting obligation of 5% of total underwriting commitment or 25 lakh; whichever is less, on his own or through its associate. • 4. The merchant banker cannot carry on any business other than that of the securities market.

- 37. • 5. The merchant banker is required to submit to the SEBI 'Due Diligence Certificate’ (Due diligence is a process of research and analysis that involves checking and analysing a company or organization before a business transaction) at least two weeks before the opening of the issue for subscription. • 6. The merchant banker is under obligation to submit to the SEBI various documents relating to the issue, draft prospectus/letter of offer and other literature to be circulated to the investors/shareholders, etc., at least two weeks before the date of filing them with the Registrar of Companies and regional stock exchanges.

- 38. • 7. The merchant banker shall keep and maintain a copy of balance sheet at the end of each accounting period, profit and loss account for that period, a copy of the auditor's report on the accounts for that period and a statement of financial position. • 8. The merchant banker is required to make disclosure of the following to the SEBI: • - Its responsibilities regarding the management of the issue. • - Any change in the information/particulars previously furnished with the SEBI having bearing on certificate of registration granted to it. • - Names and addresses of the companies whose issues it has managed or has been associated with. • - Information pertaining to its activities as manager, underwriter, consultant or advisor to the issue.

- 39. • III. SEBI Guidelines to Underwriters: SEBI (Underwriters) Rules and Regulation Act, 1993 • Underwriters are intermediaries who undertake to subscribe the unsubscribed portion of issued capital. Condition for grant or renewal of certificate. • In case of any change in the constitution, underwriter shall obtain prior permission of the Board to continue to act as underwriter. • The underwriter should enter into valid agreement with body corporate on whose behalf he is acting as underwriter. • He shall pay the amount of fees of registration in the manner • An underwriter may, if so desired makes an application in FORM A for renewal of certificate before 3 months of the expiry of period of certificate. Which is Rs 2 lakh for 1st, 2nd year and Rs 20,000 for 3rd year. Registration is granted for 3 years. • Has the necessary infrastructure like adequate office space, equipment manpower to effectively discharge his activities. • Has any past experience in underwriting or has in his employment minimum 2 persons who had the experience in underwriting.

- 40. • IV. SEBI Guidelines to Stock Brokers and Sub-brokers (Rules 1992) • Stock broker means a member of stock exchange. • Sub-broker means any person not being a member of stock exchange who acts on behalf of a stock broker as an agent or otherwise for assisting the investors in buying, selling or dealing in securities through stock broker. • No stock broker or sub broker shall buy, sell or deal in securities unless he holds a certificate granted by board under the regulation, provided that such person may continue to buy, sell or deal in securities if he has made an application for such registration.

- 41. Thank you!