Time Series Analysis:Complete

Guide from Statistics to

Deep Learning

A comprehensive exploration of techniques, models, and

applications for analyzing temporal data patterns and making

accurate forecasts

Presenter: Data Science Expert

August 2025

Made with

Genspark

2.

Table of Contents

Thispresentation provides a comprehensive overview of

time series analysis from fundamental statistical methods

to cutting- edge deep learning techniques. Progression of techniques from statistical methods to advanced deep

learning

In This Presentation

Introduction to Time Series Analysis - definitions,

importance, and applications

Time Series Components - trend, seasonality, cycle, and

noise

Statistical Techniques - stationarity, transformations,

and decomposition

Classical Models - ARIMA, SARIMA, and exponential

smoothing Advanced Models - VAR, GARCH, and state

space models

Machine Learning and Deep Learning Approaches - RNN,

LSTM, and transformers

Made with Genspark

3.

What is TimeSeries Analysis?

A time series decomposed into its components: trend, seasonality, and

random variations

Definition & Importance

Time series analysis is the study of data points collected

over time at regular intervals, with the goal of

identifying patterns, trends, and making predictions

about future values.

Key Characteristics

Temporal Ordering: Data points have a chronological

sequence that matters

Autocorrelation: Observations are not independent; they

relate to previous values

Multiple Components: Often contains trend, seasonality,

cyclical patterns, and random noise

Specialized Methods: Requires dedicated statistical and

machine learning techniques

Domain-Specific: Analysis approaches vary based on the

field (finance, economics, healthcare, etc.)

4.

Why Analyze TimeSeries Data?

Organizations that effectively analyze time series data gain

35% better forecast accuracy and reduce operational costs

by up to 25% through improved resource allocation and

risk management.

Business value of time series analysis across

industries

Key Goals and Business Value

Forecasting: Predict future values to support proactive

decision- making and resource planning

Pattern Recognition: Identify hidden patterns,

seasonality, and anomalies in historical data

Causal Analysis: Understand what factors influence changes

over time

Risk Management: Quantify uncertainty and prepare for

potential volatility

Performance Monitoring: Track KPIs over time and

detect deviations from expected behavior

5.

How Time SeriesAnalysis Differs from Other Analyses

These unique properties of time series data

necessitate specialized analytical approaches that

account for temporal dependencies and patterns.

Key differences between time series analysis and standard statistical

analysis

Unique Characteristics

Temporal Ordering: The sequence of observations

matters fundamentally, unlike cross-sectional data

where ordering is arbitrary

Dependence Structure: Observations are not

independent; current values depend on past values

Autocorrelation: Values are correlated with their own

previous values at various lags

Non-stationarity: Statistical properties (mean, variance)

often change over time

Specialized Methods: Requires specific techniques like

ARIMA, decomposition, and spectral analysis

6.

1

Section 1: TimeSeries

Fundamentals

Understanding the

basics

An introduction to core concepts,

components, and properties of time series

data that form the foundation for all

analysis techniques.

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

7.

What is aTime Series? (Detailed)

Practical Example

Consider daily stock prices for Company XYZ over one year:

import pandas as pd

import matplotlib.pyplot as plt

# Load stock price data

stock_data = pd.read_csv('xyz_stock.csv') stock_data['Date'] =

pd.to_datetime(stock_data['Date']) stock_data.set_index('Date',

inplace=True)

# Plot the time series plt.figure(figsize=(10, 6))

plt.plot(stock_data['Close']) plt.title('XYZ Stock Price

(2023-2024)') plt.ylabel('Price ($)')

plt.grid(True)

plt.show()

Definition & Concepts

A time series is a sequence of data points collected or recorded at

specific time intervals. Unlike regular data, the temporal ordering is

crucial as it captures how values change over time.

Understanding the temporal dependencies between

observations is what makes time series analysis unique

compared to other statistical methods.

Values are ordered chronologically

Intervals are typically uniform (hourly, daily,

monthly) Observations are dependent on

previous values

Used for forecasting future values based on

historical patterns

8.

Core Properties ofTime Series

Understanding these core properties is essential for

choosing appropriate preprocessing techniques,

selecting the right models, and accurately interpreting

results in time series analysis.

Illustration of temporal ordering and lag relationships in a time

series

Key Characteristics

Temporal Ordering: Data points are sequentially

ordered by timestamps, creating a natural progression

that cannot be randomly shuffled like other data types

Temporal Dependence: Future values typically depend

on past observations, creating autocorrelation patterns

that are crucial for forecasting

Lag Relationships: The influence of past values (lags) on

current values, where observations at t-1, t-2, etc., impact

the value at time t

Granularity: The time interval between observations

(hourly, daily, monthly) that affects data patterns and

modeling approaches

9.

Components of TimeSeries: Level, T

rend, Seasonality

Key Components of Time Series

Data

Level

The baseline value or the average value around which the

time series fluctuates. Represents the underlying value of

the series when other components are removed.

Trend

Long-term upward or downward movement in the data.

Shows the general direction in which the time series is

moving over an extended period.

Seasonality

Regular and predictable patterns that repeat over fixed

periods (daily, weekly, monthly, quarterly). Caused by

seasonal factors like weather

, holidays, or business cycles.

Understanding these components is crucial for effective

time series modeling and forecasting. Models can be

designed to capture each component specifically. Decomposition of a time series into its basic

components

10.

Cyclical Patterns andNoise

WHY it matters: Distinguishing between cyclical patterns

and noise is crucial for accurate forecasting. Cycles

represent real patterns that can be modeled, while noise

must be filtered out.

Cyclical pattern in economic data (business

cycle)

Random noise component in time

series

Understanding Time Series Components

Cyclical Patterns: Fluctuations that occur without

fixed frequencies, unlike seasonal patterns

Key Characteristics: Non-fixed periodicity, often spans

multiple years (business cycles, economic fluctuations)

Example: Economic expansions and contractions,

financial market cycles

Noise Component: Random, irregular fluctuations in time

series data

Importance of Noise: Represents unexplained variation

that can't be attributed to trend, seasonality, or cycles

11.

Types of TimeSeries Data

Univariate vs Multivariate

Time series data can be categorized based on the number of

variables measured at each time point. Understanding these

types is critical for selecting appropriate analysis methods.

The complexity and richness of insights increases with the

number of variables tracked over time.

Univariate Multivariate

Single variable

tracked over time

Multiple variables tracked simultaneously

Examples: Daily

temperature, stock

price

Examples: Weather data (temp,

humidity, pressure), financial

indicators

Simpler

analysis

techniques

Captures relationships between variables

Practical Examples

Consider these two approaches to analyzing retail data:

import pandas as pd

import matplotlib.pyplot as plt

# Load retail dataset

retail_data = pd.read_csv('retail_sales.csv') retail_data['Date'] =

pd.to_datetime(retail_data['Date'])

# Univariate approach - just sales univariate_series =

retail_data.set_index('Date') ['Sales']

# Multivariate approach - sales, customer count, and promotions

multivariate_series = retail_data.set_index('Date') [['Sales',

'CustomerCount', 'PromotionExpense']]

# Correlation analysis (only possible with multivariate)

correlation_matrix = multivariate_series.corr() print(correlation_matrix)

Univariate models focus on patterns within a single sequence

Multivariate analysis reveals relationships and

12.

Stationarity in TimeSeries

What is

Stationarity?

When your time series isn't stationary, transformations

like differencing, logarithmic transformation, or Box-Cox

Comparison of stationary vs. non-stationary time series. The stationary series

(blue) maintains consistent statistical properties over time, while the non-

A time series is stationary when its statistical properties do not

change over time. Specifically, this means:

Constant mean (no trend)

Constant variance (homoscedasticity)

Constant autocorrelation structure (pattern of

dependence doesn't change)

Why is Stationarity Important?

Most statistical forecasting methods assume stationarity

Makes forecasting more reliable as patterns remain

consistent Simplifies mathematical models and improves

interpretability Easier to detect genuine patterns vs

random fluctuations

13.

Examples of Stationaryvs. Non-Stationary Series

Real-World Examples

Example 1: Stock Prices (Non-

Stationary)

Google stock price - exhibits clear upward trend (non-

stationary)

After Differencing

Example 2: Stock Returns (Stationary)

Understanding Stationarity

A stationary time series has statistical properties that do not

change over time - specifically constant mean, variance, and

autocorrelation structure.

Most statistical time series models (like ARIMA)

require stationarity to make valid predictions!

Stationary series: White noise, differenced stock returns,

residuals after removing trend/seasonality

Non-stationary series: Stock prices, GDP

, temperature

readings with seasonal patterns

We can transform non-stationary series to

stationary using differencing, detrending, or seasonal

adjustment

Statistical tests like ADF, KPSS, and Phillips-Perron help

determine stationarity

14.

Applications & UseCases

Time series analysis provides valuable insights across Relative adoption of time series analysis techniques by

industry

Time Series Analysis Across Industries

Finance: Stock price prediction, portfolio optimization, risk

management, algorithmic trading, and market volatility

analysis

Retail & E-commerce: Demand forecasting, inventory

management, sales prediction, seasonal pattern

identification, and pricing optimization

Healthcare: Patient monitoring, disease progression

tracking, epidemic outbreak prediction, and hospital

resource planning

Energy & Utilities: Load forecasting, renewable energy

production prediction, consumption pattern analysis, and

smart grid optimization

Manufacturing: Predictive maintenance, production

planning, supply chain optimization, and quality control

Environment & Climate: Weather forecasting, climate

change analysis, natural disaster prediction, and

ecological monitoring

15.

2

Section 2: Data

Preprocessing

&

Exploration

Preparingand understanding

your

dat

a

Essential techniques for cleaning,

transforming, and exploring time series

data to ensure accurate analysis and

modeling results.

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

16.

Checking Stationarity: How& Why

Statistical Tests for Stationarity

Stationarity is critical for time series modeling because many

techniques assume statistical properties remain constant over time.

Rather than relying on visual inspection alone, we use formal

statistical tests to confirm stationarity.

Why test for stationarity? Non-stationary data can lead to

spurious regressions and unreliable forecasts in traditional time

series models.

Tes

t

Null

Hypothesi

s

Interpretati

on

AD

F

(Augmented

Dickey- Fuller)

Series has

a unit root

(non-

stationary)

p-value < 0.05: Reject

null hypothesis

(stationary)

KPSS

(Kwiatkowski-

Phillips- Schmidt-

Shin)

Series is

stationar

y

p-value < 0.05: Reject null

hypothesis (non-

stationary)

PP

Series has

a unit root p-value < 0.05: Reject

Practical Implementation

Using Python's statsmodels to test for stationarity:

import pandas as pd

import numpy as np

from statsmodels.tsa.stattools import adfuller, kpss import

matplotlib.pyplot as plt

# Example time series (non-stationary with trend)

np.random.seed(42)

ts = pd.Series(np.cumsum(np.random.normal(0.1, 1, 100)))

# Run ADF test adf_result =

adfuller(ts)

print(f'ADF Statistic: {adf_result[0]:.4f}') print(f'p-value:

{adf_result[1]:.4f}') print('Critical Values:')

for key, value in adf_result[4].items():

print(f' {key}: {value:.4f}')

# Run KPSS test kpss_result

= kpss(ts)

print(f'KPSS Statistic: {kpss_result[0]:.4f}') print(f'p-value:

{kpss_result[1]:.4f}')

17.

Transformations for Time

Series

Transformatio

n

Whento Use Why It Works

Log Transform

Data with

exponential

growth or

multiplicative

patterns

Reduces exponential trends

to linear; stabilizes variance

when SD proportional to

mean

Box-Cox

When simple

log transform

isn't optimal

Family of power

transformations that

finds optimal parameter

(λ) to normalize data

Series with trend

Removes trend (1st diff)

and seasonality (seasonal

Why Transform Time Series Data?

Stabilize variance - Make data more consistent across

time Achieve stationarity - Essential for many

forecasting models Normalize distribution - Make data

more symmetrical Remove trend & seasonality -

Isolate the underlying patterns

18.

Handling Missing Values& Outliers

Practical Example

Let's examine how to handle missing values and outliers in monthly

sales data:

import pandas as pd

import numpy as np

import matplotlib.pyplot

as plt

# Load time series with missing values and outliers sales =

pd.read_csv('monthly_sales.csv', parse_dates= ['date'])

# 1. Handle missing values with interpolation sales_clean =

sales.copy() sales_clean['value'] =

sales_clean['value'].interpolate(method='time')

# 2. Detect and handle outliers with IQR method Q1 =

sales_clean['value'].quantile(0.25)

Q3 = sales_clean['value'].quantile(0.75)

IQR = Q3 - Q1

lower_bound = Q1 - 1.5 * IQR

upper_bound = Q3 + 1.5 * IQR

# Replace outliers with median of neighboring points mask =

Why It Matters

Time series data often contains missing values and outliers that

can significantly distort analysis and forecasting models. Properly

handling these anomalies is crucial for accurate modeling.

Ignoring missing values or outliers can lead to biased

parameter estimates, unreliable forecasts, and misleading

insights about the underlying patterns.

Missing Value Techniques

Forward/Backward Fill - Propagate last known value

forward or first known value backward

Interpolation - Linear

, spline, or time-weighted methods

to estimate missing points

Statistical Imputation - Replace with mean, median, or

model-based estimates

Outlier Detection & Treatment

IQR Method - Identify points beyond 1.5×IQR from

19.

Resampling and FrequencyAdjustment

In Python: df.resample('M').mean() - Resample to

Visual comparison of original daily data vs. weekly and monthly

resampling

Why Resample Time Series Data?

Change analysis granularity - Aggregate daily

data to weekly/monthly for high-level trends

Reduce noise - Lower frequencies often smooth out

short-term fluctuations

Match different data sources - Align data collected at

different frequencies

Computational efficiency - Reduce dataset size for

faster processing

How to Resample?

Upsampling - Increase frequency (e.g., monthly → daily);

requires interpolation

Downsampling - Decrease frequency (e.g., daily →

monthly); requires aggregation

20.

Visualizing Time Series

Choosingthe right visualization depends on what aspect

of the time series you want to analyze. Combining

Different visualization methods applied to the same time series

data

Common Visualization Methods

Line plots: Most basic visualization showing evolution over

time; reveals overall trends, patterns, and outliers

Seasonal plots: Overlays same seasons from different

cycles; highlights seasonal patterns and variations

between cycles

Lag plots: Shows relationship between an observation and

its lagged value; useful for identifying autocorrelation and

non-linear patterns

ACF/PACF plots: Displays correlations between the series

and its lags; reveals dependencies and helps with model

selection

Heatmaps: Color-coded grid visualization; effective for

multiple time series or displaying cyclical patterns by

hour/day/month

Decomposition plots: Breaks down series into trend,

seasonal, and residual components; helps understand

underlying patterns

21.

Seasonal Decomposition (STL,Classical)

STL Decomposition

Example

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.seasonal import seasonal_decompose

# Monthly airline passenger data

airline = pd.read_csv('airline_passengers.csv') airline['Month'] =

pd.to_datetime(airline['Month']) airline.set_index('Month',

inplace=True)

# Apply STL decomposition

decomposition = seasonal_decompose(airline['Passengers'],

model='multiplicative',

period=12)

# Plot the decomposed components fig

= decomposition.plot() plt.tight_layout()

plt.show()

What is Seasonal Decomposition?

Seasonal decomposition is a technique that breaks down a time

series into its constituent components: trend, seasonality, and

residuals. This helps in better understanding the underlying patterns

and improving forecasting accuracy.

Decomposition reveals hidden patterns that might not be

visible in the original series, making it easier to model each

component separately.

Two Main Approaches:

Classical Decomposition: Simple approach that assumes

constant seasonal component; can be additive or

multiplicative

STL (Seasonal-Trend decomposition using LOESS):

More robust method that handles changing seasonality

and outliers

Additive Model: Y = Trend + Seasonality + Residual (for

constant seasonal amplitude)

Multiplicative Model: Y = Trend × Seasonality × Residual (for

22.

3

Section 3:

Statistica

l

T

echniques

Essential analytical

tools

Examiningcore statistical methods that

help identify patterns, relationships, and

structures within time series data to

support robust forecasting and analysis.

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

23.

Autocorrelation Function (ACF)

ExampleACF Plot with

Interpretations

Significant autocorrelation- Values above/below blue

dashed lines

Seasonal pattern- Regular spikes at fixed intervals (e.g., 12 for

monthly)

Exponential decay- Suggests AR

process

What is Autocorrelation?

Definition: Autocorrelation measures the correlation

between a time series and its lagged values (correlation

with itself)

Mathematical expression: Correlation between Yt and

Yt-k for different lag values k

Scale: Ranges from -1 (perfect negative correlation)

to +1 (perfect positive correlation)

Interpretation: Shows how current values relate to past

values at different time intervals

Practical Use Cases

Model identification: Helps determine

appropriate ARIMA/SARIMA model

parameters

Seasonality detection: Regular spikes at fixed intervals

indicate seasonality

Stationarity assessment: Slow decay in ACF suggests

non- stationarity

24.

Partial Autocorrelation Function(PACF)

Shows total correlation (direct

+ indirect)

Shows only direct

correlation

Helpful for identifying

MA(q) models

Helpful for identifying AR(p)

models

Comparison of ACF and PACF patterns for different time series

models

Common PACF Patterns:

AR(p) process: PACF cuts off after lag

p

What is PACF?

Definition: Measures the direct correlation between

observations at different lags after removing the influence

of intermediate observations

Purpose: Isolates the "pure" relationship between

observations at specific lags

Interpretation: Shows significant spikes at lags that have

direct influence on the current value

Model Identification: Used to determine the order

(p) of an autoregressive (AR) model

PACF vs ACF

ACF PACF

25.

Using ACF/PACF forModel Selection

Interpreting Autocorrelation

Plots

Look for the cutoff point where values fall within

significance bands (dashed lines). This helps determine the

appropriate order for model parameters.

Key

Guidelines

Examine ACF & PACF

plots

ACF: Cuts off

PACF: Tails off

ACF: Tails off

PACF: Cuts off

Suggests MA(q)

q = lag where ACF cuts

off

Suggests AR(p)

p = lag where PACF cuts

off

Both ACF &

PACF tail off

gradually

Both ACF &

PACF show no

pattern

ACF plot: Shows correlation between a series and its lags;

helps identify MA(q) order

PACF plot: Shows direct correlation between a series and

lags

after removing intermediate effects; helps identify AR(p)

order

Differencing: Apply until ACF/PACF show stationarity

(quick decay) to determine d

ARIMA(p,d,q): Model parameters can be derived directly

from pattern recognition in ACF/PACF plots

AR process: PACF cuts off after lag p, ACF decays

gradually

26.

Decomposition: Additive vsMultiplicative

Feature Additive Multiplicative

Interpretation Absolute changes Percentage changes

Two Approaches to Time Series

Decomposition

Additive Decomposition: Y = Trend + Seasonality + Residual

Multiplicative Decomposition: Y = Trend × Seasonality ×

Residual

When to Use Each Model

Additive: When seasonal variations are relatively constant

over time, regardless of the level of the series

Multiplicative: When seasonal variations increase with the

level of the series (amplitude of seasonality grows with

trend)

Model selection is critical: Using an additive model for

multiplicative data (or vice versa) leads to poor

decomposition and affects forecasting accuracy.

27.

Unit Root Tests:ADF, KPSS, Phillips-Perron

Testing for Stationarity

Unit root tests are statistical methods used to determine whether

a time series is stationary or not. They're crucial because most

time series models require stationarity.

Unit root tests should be the first step in your time series

modeling workflow to ensure you're working with stationary

data.

Test

Null

Hypothesi

s

When to

Use

ADF

(Augmented

Dickey- Fuller)

Series has

a unit root

(non-

stationary)

Most common test; use as

your first check

KPSS

(Kwiatkowski-

Phillips- Schmidt-

Shin)

Series is

stationar

y

Complements ADF; use both

to confirm results

Phillips-Perron

(PP)

Series has

a unit root

(non-

When data has

heteroskedasticity or

Practical Implementation

Let's test a financial time series (stock prices) for stationarity

using all three methods:

import pandas as pd

from statsmodels.tsa.stattools import adfuller, kpss from

arch.unitroot import PhillipsPerron

# Test function

def test_stationarity(timeseries):

# ADF Test

adf_result = adfuller(timeseries, autolag='AIC') adf_pvalue =

adf_result[1]

# KPSS Test

kpss_result = kpss(timeseries, regression='c') kpss_pvalue =

kpss_result[1]

# Phillips-Perron Test

pp = PhillipsPerron(timeseries)

pp_pvalue = pp.pvalue

return adf_pvalue, kpss_pvalue,

pp_pvalue

29.

Lag, Differencing, andMemory

Understanding these concepts is crucial for model

selection: AR models depend on lags, differencing creates

stationary series, and memory characteristics determine

appropriate forecasting techniques.

Visualization of original series, lagged series, and differenced

series

Key Concepts for Time Series Analysis

Lag: Shifted version of a time series; Lag-1 refers to

observations shifted by one time period (Yt-1). Critical for

autocorrelation and model building.

Differencing: Subtracting lagged values from current

values to stabilize mean and remove trends. First-order: Yt

- Yt-1, Second- order: (Yt - Yt-1) - (Yt-1 - Yt-2).

Memory: How past values influence current observations.

Short memory (decay quickly) vs. Long memory (persist for

many periods).

Partial Redundancy: After accounting for intermediate

lags, how much unique information exists between current

and earlier observations.

30.

Practical Example: Decompositionand ACF/PACF

Analysis

Implementation &

Results

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.seasonal import seasonal_decompose from

statsmodels.graphics.tsaplots import plot_acf, plot_pacf

# Load airline passenger data

airline = pd.read_csv('AirPassengers.csv') airline['Month'] =

pd.to_datetime(airline['Month']) airline.set_index('Month',

inplace=True)

# Decompose the time series

decomposition = seasonal_decompose(airline['Passengers'],

model='multiplicative')

# Plot ACF and PACF plot_acf(airline['Passengers'],

lags=36) plot_pacf(airline['Passengers'], lags=36)

Airline Passengers Dataset (1949-1960)

The classic airline passengers dataset shows monthly totals of

international airline passengers over 12 years, exhibiting both

trend and seasonality.

This dataset is ideal for demonstrating decomposition and

autocorrelation analysis as it contains clear patterns that are

easily identifiable.

Clear upward trend showing increasing passenger numbers

over time Strong seasonal pattern with peaks in summer

months

Multiplicative seasonality (seasonal variations increase with

the trend) ACF shows strong seasonality with peaks at lags 12,

24, 36

PACF cuts off after lag 1 and shows significant spike at lag 12

These patterns suggest a seasonal ARIMA model with

parameters related to 12-month seasonality would be appropriate.

31.

4

Section 4:

Classical

Models

ARIMA, SARIMA,and

Exponential

Smoothin

g

Exploring traditional statistical approaches

that form the backbone of time series

forecasting, their mathematical foundations,

implementation, and practical applications.

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

32.

Naive and SimpleForecasting

Methods

Simple Methods as Benchmarks

Simple forecasting methods provide baselines against which more

complex models are compared. A sophisticated model should at

minimum outperform these basic methods to justify its complexity.

Always compare advanced models against naive

benchmarks to ensure additional complexity is justified by

improved performance.

Metho

d

Descriptio

n

Mea

n

Uses the average of all historical observations as

the forecast for all future values

Naiv

e

Uses the last observed value as the forecast for all

future periods

Seasona

l

Naiv

e

Uses the value from the same season (e.g., same

month last year) as the forecast

Drif

t

Extends the line between the first and last

observations to forecast future values

Benchmark Examples

Comparing simple methods on quarterly retail sales data:

import pandas as pd

import numpy as np

from statsmodels.tsa.api

import

SimpleExpSmoothing

# Forecast methods

def mean_forecast(data,

h):

return

np.array([data.mean()] *

h)

def naive_forecast(data,

h):

return

np.array([data.iloc[-1]] *

h)

def seasonal_naive(data,

h, m):

return np.array([data.iloc[-(m + i % m)] for i in range(h)])

33.

Introduction to ARIMA

What,How, and Why of ARIMA

Models

AR(p)

AutoRegressiv

e

Uses

past

values

I(d)

Integrate

d

Differencin

g

MA(q

)

Movin

g

Averag

e

Past

errors

What: ARIMA (AutoRegressive Integrated Moving Average)

is a classical statistical model that combines three

techniques for time series forecasting

How: ARIMA(p,d,q) model parameters:

p - AR order: Number of lag

observations

d - Integration order: Differencing needed for

stationarity

q - MA order: Size of the moving average window

Why: ARIMA models excel at capturing complex

temporal dynamics in time series data with trend

patterns

When to use: Best for stationary (or can be made

stationary) series with linear relationships between

current and past values

ARIMA combines the strengths of autoregression (AR),

34.

Autoregressive Model (AR)

Whento use AR models: When current values have

direct dependencies on past values and PACF shows

clear cutoff pattern. Excellent for capturing

PACF plot for an AR(2) process showing significant spikes at lags 1

and 2

The Building Block of ARIMA

Definition: Autoregressive models predict future values

based on a linear combination of past observations (lags)

AR(p) Model: Uses p previous time steps as

predictors Mathematical Formulation:

Yt = c + φ1Yt-1 + φ2Yt-2 + ... + φpYt-p + εt

Parameters: φ1, φ2, ..., φp are coefficients that

indicate the strength and direction of the

relationship

Identification: PACF shows significant spikes at lags 1 to p,

then cuts off

Stationarity Requirement: Data must be stationary

(constant mean, variance)

Y_

t

Y_t-1

Y_t-2

φ₁

φ₂

35.

Moving Average Model(MA)

Visualization of Moving Average Effect on Time

Series

MA(2): yt = μ + εt + θ1εt-1 + θ2εt-2

What is a Moving Average Model?

A Moving Average (MA) model predicts the current value

based on past forecast errors (not past values)

MA(q) model of order q uses q previous error terms: yt = μ

+ εt + θ1εt-1 + θ2εt-2 + ... + θqεt-q

Unlike AR, MA models use unobservable errors rather

than observable past values

MA models are essentially weighted averages of

random shocks

Comparison with AR Models

AR uses past values; MA uses past

errors

MA models have finite memory, AR models have infinite

memory

In ARIMA, both components (AR and MA) work

together to capture different aspects of time

dependence

36.

Integrated (Differencing) inARIMA

Practical Example

Let's see the effect of differencing on Google stock prices:

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.stattools import adfuller

# Original series

print('ADF Test on original series:') result =

adfuller(goog_prices)

print(f'p-value: {result[1]:.4f}') # Large p-value -> non-stationary

# First differencing

diff1 = goog_prices.diff().dropna() print('ADF Test after

first differencing:') result = adfuller(diff1)

print(f'p-value: {result[1]:.4f}') # Small p-value ->

stationary

What is Differencing?

Differencing is the "I" (Integrated) component in ARIMA. It

transforms a non-stationary time series into a stationary one by

computing the difference between consecutive observations.

The "d" parameter in ARIMA(p,d,q) represents how many

times differencing is applied to achieve stationarity.

First differencing: y't = yt - yt-1 (removes trends)

Second differencing: y''t = y't - y't-1 = yt - 2yt-1 + yt-2 (for

quadratic trends) Seasonal differencing: y't = yt - yt-s (removes

seasonality of period s) Differencing reduces the data length by 1

for each application

Stationarity after differencing means the resulting series has

constant mean, variance, and autocorrelation structure over

time, which is a requirement for ARIMA modeling.

37.

Model Order Selection(p,d,q) for ARIMA

Pattern in ACF Pattern in PACF Suggested Model

Determining ARIMA Parameters

p (AR order): Number of autoregressive terms - Check

PACF for significant lags

Rule of thumb: Start with small values (p ≤ 2, d ≤ 2, q ≤ 2)

and use Grid Search or Auto ARIMA to find optimal

parameters if manual selection is difficult.

d (differencing): Order of differencing needed to

achieve stationarity - Use ADF/KPSS tests

q (MA order): Number of moving average terms - Check

ACF for significant lags

Information criteria: Compare AIC (Akaike) and BIC

(Bayesian) values - lower is better

Residual analysis: Check residuals for white noise (no

pattern) to validate model adequacy

Check for

Stationarity

(ADF/KPSS Tests)

If not stationary:

Apply differencing

(d=1,2...)

Examine ACF & PACF plots

of stationary series

PACF cuts

off

→

Estim

ate p

ACF cuts

off

→ Estimate

q

38.

Seasonal ARIMA (SARIMA)

ARIMAvs. SARIMA forecast on seasonal

data

Feature ARIMA SARIMA

Handles trends

Handles seasonality

Parameter count 3 (p,d,q) 7 (p,d,q,P,D,Q,s)

Extending ARIMA to Handle Seasonality

SARIMA Definition: Extends ARIMA to incorporate

seasonal patterns in time series data

Notation: SARIMA(p,d,q)(P,D,Q,s) where lowercase

letters represent non-seasonal components and

uppercase letters represent seasonal components

Seasonal Orders:

P = Seasonal autoregressive order

D = Seasonal differencing order

Q = Seasonal moving average

order

s = Seasonal period (e.g., 12 for monthly data with

yearly seasonality)

When to Use: When data exhibits clear seasonal patterns at

fixed intervals (daily, weekly, monthly, quarterly)

SARIMA is particularly effective for forecasting seasonal

data like retail sales, tourism, and utility consumption

39.

Exponential Smoothing &ETS

WHY: Exponential smoothing methods are popular due to

their simplicity, computational efficiency, and ability to

handle a wide range of time series patterns with minimal

Evolution of exponential smoothing methods and their capabilities for

handling different time series components

Family of Powerful Forecasting Methods

Simple Exponential Smoothing (SES)

For time series with no clear trend or

seasonality Formula: ŷt+1 = αyt + (1-α)ŷt

Holt's Method (Double Exponential

Smoothing)

Extends SES to capture trend

Uses level and trend smoothing equations

Holt-Winters (Triple Exponential

Smoothing)

Captures level, trend, and seasonality

Can handle additive or multiplicative

seasonality

ETS Framework (Error, Trend, Seasonal)

Unified statistical framework for all exponential smoothing

methods Notation: ETS(Error

, Trend, Seasonal) e.g., ETS(A,A,M)

40.

Practical Example: ARIMAon Catfish Sales

Step-by-Step Implementation

Using catfish sales data (thousands of pounds sold monthly from

1996 to 2008), we'll implement an ARIMA model to capture the

trend and patterns in the data.

1 Data Exploration

Load the data and examine trends, seasonality, and

stationarity properties

2 Checking Stationarity

Apply ADF test and differencing if needed to achieve

stationarity

3 Determine ARIMA Parameters

Use ACF/PACF plots to identify p, d, q values

(order=12,1,1)

4 Model Fitting

Fit the ARIMA model using statsmodels and generate

predictions

5 Evaluation & Interpretation

Compare predictions with actual values and assess model

fit

ARIMA

Implementation

import pandas as pd

import numpy as np

import matplotlib.pyplot

as plt

from statsmodels.tsa.arima.model import ARIMA from

statsmodels.tsa.stattools import adfuller

# Load and prepare catfish sales data catfish_sales =

pd.read_csv('catfish.csv',

parse_dates=[0], index_col=0)

# Check stationarity with ADF test

result = adfuller(catfish_sales['Total'].diff().dropna()) print(f'ADF p-value:

{result[1]}')

# Fit ARIMA model (p=12, d=1, q=1)

arima = ARIMA(catfish_sales['Total'], order=(12,1,1)) arima_fit =

arima.fit()

# Generate predictions predictions =

arima_fit.predict()

# Plot actual vs predictions plt.figure(figsize=(12, 6))

41.

Practical Example: SARIMAwith Seasonality

ARIM

A

8.92

RMSE

SARIMA

3.41

RMSE

Implementation Example

Monthly temperature data with clear seasonal patterns:

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.statespace.sarimax import SARIMAX from

statsmodels.tsa.arima.model import ARIMA

# Split into train/test train =

temp_data[:'2020'] test =

temp_data['2021':]

# ARIMA model (1,1,1)

arima_model = ARIMA(train, order=(1,1,1))

arima_results = arima_model.fit()

arima_pred = arima_results.forecast(steps=12)

# SARIMA model (1,1,1)×(1,1,1,12)

sarima_model = SARIMAX(train,

order=(1,1,1), seasonal_order=(1,1,1,12))

sarima_results = sarima_model.fit()

sarima_pred =

sarima_results.forecast(steps=12)

SARIMA vs ARIMA

While ARIMA models can handle trends effectively, they struggle

with seasonal patterns. SARIMA (Seasonal ARIMA) extends ARIMA by

incorporating seasonal components, making it ideal for data with

recurring patterns.

SARIMA captures both the non-seasonal components

(p,d,q) and seasonal components (P,D,Q,m) where m represents

the seasonal period.

Significantly improves forecast accuracy for

seasonal data Reduces residual seasonality in the

model

Better captures monthly, quarterly, or yearly

patterns More accurate prediction intervals

42.

5

Section 5:

Advanced

Statistica

l

Model

s

Beyond traditional

approaches

Exploringsophisticated statistical

techniques for complex time series data,

including multivariate models, volatility

modeling, and state space approaches for

enhanced forecasting accuracy.

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

43.

Vector Autoregression (VAR)

HistoricalMultivariate Time

Series

GDP

Inflation

Unemployment

VAR

Model

Captures interdependencies

between time series

Forecas

t Future

Values

Feedback Effects

Yt

= c + A1

Yt-1

+ A2

Yt-2

+ ... + Ap

Yt-p

+ εt

VAR model captures interdependencies among multiple time series

variables, with each variable potentially influencing all others in

the system.

Multivariate Time Series Modeling

What is VAR? A statistical model that captures linear

interdependencies among multiple time series, where

each variable is influenced by its own past values AND

past values of other variables

Why use VAR? It extends univariate autoregressive

models to capture relationships between multiple

related time series simultaneously

Key characteristics: Treats all variables as

endogenous (internally determined), accounts for

feedback effects, and captures complex dynamics

Key applications: Macroeconomics (GDP

, inflation,

unemployment), financial markets (stock returns,

volatility), forecasting interconnected metrics

VAR models are particularly valuable when you need to

understand how multiple time series variables influence

each other

, making them ideal for studying cause-and-

effect relationships and systemic behavior.

44.

GARCH for VolatilityModeling

WHY IT MATTERS: Unlike constant volatility models,

GARCH dynamically responds to market conditions,

providing more accurate risk assessments during

financial crises and market turbulence. Volatility clustering in S&P 500 returns - GARCH models excel at capturing

these patterns

Understanding GARCH Models

Generalized AutoRegressive Conditional

Heteroskedasticity captures time-varying volatility in

financial data

Extends ARCH models by including past conditional

variances in addition to past squared errors

Effectively models volatility clustering - periods where

high volatility tends to be followed by high volatility

Essential for risk management, option pricing, and

portfolio optimization

σ 2 = ω + Σα ε 2 + Σβ σ 2

t i t-i j

t-j

45.

State Space Models& Kalman Filter

Applications in Time

Kalman Filter Estimation

Process

Kalman Filter Algorithm

1. Predict: x̂t|t-1 = Fx̂t-1|t-1

Understanding Dynamic Systems

State Space Models: Framework representing a time series

as the output of a dynamic system driven by unobserved

states and observed measurements

Two Key Equations:

State equation: xt = Fxt-1 + wt

Observation equation: yt = Hxt + vt

Kalman Filter: Recursive algorithm that optimally

estimates the hidden states of a system based on noisy

measurements

Why it works: Combines predictions from the model

with new measurements, weighting each by their

uncertainty

The Kalman filter is the optimal estimator for linear systems

with Gaussian noise, making it powerful for many time

series applications including tracking, smoothing, and

46.

Combining Classical andAdvanced Models

Practical Implementation

This example combines SARIMA (for seasonality) with GARCH

(for volatility) to forecast electricity demand:

import pandas as pd

import numpy as np

from statsmodels.tsa.statespace.sarimax import SARIMAX from arch

import arch_model

# Step 1: Fit SARIMA model for mean forecast

sarima_model = SARIMAX(ts_data, order=(2,1,2),

seasonal_order=(1,1,1,12)) sarima_results =

sarima_model.fit()

sarima_forecast =

sarima_results.forecast(steps=24)

# Step 2: Model residuals with GARCH for volatility residuals =

sarima_results.resid[1:]

garch_model = arch_model(residuals, vol='GARCH', p=1, q=1)

garch_results = garch_model.fit(disp='off') garch_forecast =

garch_results.forecast(horizon=24)

# Step 3: Combine forecasts for final prediction

combined_forecast = {

Why Combine Models?

Different time series models excel at capturing different aspects

of the data. By combining models, we can leverage their

complementary strengths to achieve more robust and accurate

forecasts.

Model combination often outperforms individual models

by reducing overfitting and increasing forecast stability,

particularly in volatile or complex time series.

ARIMA models capture linear dependencies

efficiently State space models handle hidden

components well Machine learning models capture

non-linear relationships Ensemble methods reduce

forecast variance

Hybrid approaches integrate statistical rigor with

ML flexibility

Common Combination Approaches

47.

Limitations of Classicaland Advanced Models

Understanding model limitations is critical for selecting the

right approach. No single model works for all time series

problems - ensemble methods often provide more robust

Severity of limitations across different time series

models

Common Pitfalls to Consider

Stationarity Assumption: Many classical models

require stationarity, which may require extensive

transformations

Linear Relationships: ARIMA and VAR assume

linear relationships, failing with complex nonlinear

patterns

Volatility Handling: Most models (except GARCH) struggle

with heteroskedastic data showing varying volatility

Complex Seasonality: Multiple seasonal patterns or

irregular cycles challenge traditional approaches

Structural Breaks: Sudden changes in time series behavior

can lead to poor forecasting performance

Parameter Sensitivity: Results heavily depend on

proper parameter selection (p,d,q in ARIMA)

48.

Practical Example: GARCHfor Volatility Modeling

Multivariate Stock Example

Implementing GARCH(1,1) on S&P 500 daily returns:

import pandas as pd

import numpy as np

from arch import

arch_model

# Load daily S&P 500

returns

returns = pd.read_csv('sp500_returns.csv') returns['Date'] =

pd.to_datetime(returns['Date']) returns.set_index('Date',

inplace=True)

# Fit GARCH(1,1) model

model = arch_model(returns['sp500'], vol='GARCH', p=1, q=1)

results = model.fit(disp='off')

# Get conditional volatility forecast forecasts =

results.forecast(horizon=5)

conditional_vol =

np.sqrt(results.conditional_volatility)

GARCH in Financial Markets

GARCH (Generalized Autoregressive Conditional

Heteroskedasticity) models are essential tools for financial

analysts to capture and forecast volatility clustering in asset

returns.

Volatility clustering refers to the observation that large

changes in asset prices tend to be followed by more large

changes, and small changes tend to be followed by more small

changes.

Why GARCH? Captures time-varying volatility that simple

models miss

Common applications: Risk management, option pricing,

portfolio optimization

Key insight: Today's volatility depends on yesterday's

volatility and returns

Forecasting: Can predict future volatility levels, crucial

for VaR calculations

GARCH(1,1) is the most common specification, where today's

49.

Section

6:

Machine

Learning

Approa

6ches

Beyond traditional statistics

Exploringhow modern machine learning

techniques can be applied to time series

forecasting, offering new perspectives and

capabilities beyond classical statistical

models.

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

50.

Regression for TimeSeries Forecasting

WHY: Regression models handle multiple inputs, capture

non- linear relationships, and incorporate external

factors that traditional time series models cannot.

Lagged features approach for regression-based time series

forecasting

Using Regression in Time Series

Feature Engineering: Transform time series data into

supervised learning problem by creating features from

timestamps, lagged values, and external variables

Lagged Predictors: Use past values (t-1, t-2, ..., t-n) as

input features to predict future values at time t

Rolling Window Approach: Train model on fixed-size

window of historical data, then shift window forward for

prediction

Model Types: Linear regression, ridge/lasso regression,

elastic net for simpler interpretable models

Multi-step Forecasting: Direct (separate model per

horizon) vs. recursive (iterative prediction) approaches

51.

Tree-Based Models (RandomForest, XGBoost)

Capturing Non-Linearity in Time

Series

WHY: Traditional time series models (ARIMA, ETS) struggle

with non-linear patterns and complex interactions between

variables. Tree-based models excel at modeling these

relationships automatically.

Visual representation of a decision tree for time series forecasting, splitting

on lag features to capture non-linear patterns

Beyond Linear Models: Tree-based models can capture

complex non-linear relationships without explicit

specification

Random Forest: Ensemble of decision trees that

reduces overfitting through aggregating multiple

trees' predictions

XGBoost: Gradient boosting implementation that

sequentially builds trees to correct previous models'

errors

Feature Engineering: Uses lagged values, rolling

statistics, and date-based features as inputs

Automatic Feature Selection: Inherently identifies

important predictors without manual specification

Is Lag1 >

10?

Is Lag3 <

5?

Is Lag2 >

15?

Predict:

7.2

Predict:

12.5

Is Lag7 >

8?

Predict:

18.3

Predict:P1r4e.d1ic

t: 16.8

52.

Facebook Prophet

Prophet decomposesa time series into its key components, making it

Additive Model Approach & Business

Features

What: An open-source forecasting tool developed by

Facebook that decomposes time series into trend,

seasonality, and holiday effects

Additive Model: y(t) = trend(t) + seasonality(t) +

holiday(t) + error(t)

Business-Friendly Features:

Intuitive parameters that are easy for non-

experts to understand

Automatic detection of seasonality (daily, weekly,

yearly) Built-in handling of holidays and special

events

Robust to missing data and outliers

When to Use: Ideal for time series with strong seasonal

effects, multiple seasons, and when domain expertise

53.

Model Selection inML for Time

Series

Critical Considerations for Time Series ML

Temporal Validation: Traditional k-fold cross-validation

breaks temporal order and leads to data leakage; use

time-based validation instead

Walk-Forward Validation: Train on historical data, test on

future periods; incrementally move forward in time

Expanding Window: Start with minimal training data and

expand window as you move forward

Sliding Window: Fixed-size training window that shifts

forward, useful for capturing recent patterns

Preventing Data Leakage: Never use future

information for feature engineering or preprocessing

WARNING: Standard ML validation techniques can lead to

overly optimistic performance estimates in time series

forecasting due to temporal data leakage. Always maintain

strict temporal ordering!

Training Data Testing Data Unused Data

Time-based validation methods preserve temporal ordering to prevent data

leakage

Standar

d

CV

Expandin

g

Windo

w

Slidin

g

54.

Practical Prophet ForecastingExample

)

Retail Sales Forecasting

Implementation with a retail sales dataset:

import pandas as pd

from prophet import Prophet

# Load retail sales data

df = pd.read_csv('retail_sales.csv')

# Prophet requires columns named 'ds' and 'y'

df = df.rename(columns={'date': 'ds', 'sales': 'y'})

# Initialize and fit the model model =

Prophet( yearly_seasonality=True,

weekly_seasonality=True,

daily_seasonality=False,

holidays=holidays_df # Custom

holiday events

# Add country-specific holidays

model.add_country_holidays(country_name='US')

# Fit the model

Business-Friendly Forecasting

Prophet is designed to be accessible to business users without

specialized time series expertise, making it easy to generate reliable

forecasts for business planning.

Prophet automatically handles missing values, outliers,

and seasonal effects with minimal parameter tuning

needed.

Simple API with intuitive parameters for non-

experts Built-in handling of holidays and special

events Robust to missing data and outliers

Automatically detects yearly, weekly, and daily

seasonality Provides uncertainty intervals for business

risk assessment Easily interpretable components (trend,

seasonality, holidays)

Unlike complex ARIMA models, Prophet's approach makes it ideal

for retail, demand planning, and business operations forecasting.

55.

Pros and Consof ML VS Statistical Models

Machine Learning

Models

Best for: Complex patterns, large datasets, when

explanatory power is less critical than predictive

performance

Statistical

Models

Best for: When interpretability matters, smaller datasets,

when assumptions about data distribution hold

Excellent at capturing complex non-linear

relationships

Can handle large volumes of data

efficiently Automatically identifies

important features

Captures intricate patterns without

explicit programming

Often work as "black boxes" with limited

interpretability Require substantial training data

May be computationally intensive

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

Highly interpretable with clear statistical significance

Work well with smaller datasets

Strong theoretical foundation and established

methodology Simple to implement and explain to

stakeholders

May miss complex non-linear relationships

Often require stationarity and other

assumptions Feature engineering usually

needed manually

56.

7

Section 7:

Deep Learning

Method

s

Modernneural networks for

time

serie

s

Exploring advanced neural network

architectures for time series forecasting,

including RNNs, LSTMs, CNNs, and

Transformer models that excel at capturing

complex temporal patterns.

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

57.

Neural Networks andTime Series

Neural network architecture for time series: Input layer processes

sequential time sFteinpsa,nhcidiadlefnolraeycearsstcianpgture

Why Neural Networks for Time Series?

Non-linear patterns: Capture complex

relationships not detectable by linear models

Automatic feature extraction: Learn relevant features

directly from raw data

Scalability: Handle large volumes of multivariate time

series data

Long-term dependencies: Specialized architectures (LSTM,

GRU) can remember patterns over extended periods

Key Considerations

Data hungry: Require substantial historical data for

training

Black box nature: Limited interpretability compared to

statistical models

Overfitting risk: Need proper regularization and

validation strategies

Computational resources: Training can be time and

58.

Recurrent Neural Networks(RNN)

How RNNs Process Sequential Data

Temporal Connections: RNNs maintain internal memory

by feeding outputs back into the network, creating a

feedback loop

RNNs are foundational for time series analysis but struggle

with long sequences. This limitation led to the

development of LSTM and GRU networks which better

preserve information over time.

Unfolded RNN architecture showing temporal connections and vanishing

gradient problem over time steps

Hidden States: Information persists through time

steps via hidden state vectors, making RNNs ideal for

sequential data

Shared Parameters: Same weights applied at each time

step, reducing parameters while capturing sequential

patterns A A A A

Vanishing Gradient Problem: Gradients diminish exponentially

during backpropagation through time, making it

difficult to capture long-range dependencies

Strong

signal

Weakenin

g

Almost

gone

Information Loss: Early inputs lose influence on

predictions as sequence length increases due to gradient

decay

t=1

x₁

t=2

x₂

t=3

x₃ x₄

t=4

y₁ y₂ y₃ y₄

59.

LSTM Networks

σ

Forget

Gate

σ

Input

Gate

tan

h

σ

Output

Gate

Cell

State

New

State

Inpu

t

Outpu

t

Problem StandardRNN LSTM Solution

Long-term

Dependencie

s

Vanishing

gradients prevent

learning

Memory cells

maintain

information flow

Informatio

n Control

Cannot

selectively

remember/forg

et

Gates control

information

retention

Training Stability

Unstable for

long

More stable

gradient flow

LSTM cell architecture with gates controlling information

Solving the Limitations of RNNs

Long Short-Term Memory networks are specialized

RNNs designed to overcome the vanishing gradient

problem

Memory Cell Architecture: Contains specialized gates

(input, forget, output) that control information flow

Long-term Dependencies: Can capture patterns and

relationships over extended time periods

Selective Memory: Can learn which information to store,

forget, or update

Bidirectional Capability: Can process time series data in

both forward and backward directions

Time Series Use Cases: Financial forecasting, energy

load prediction, weather forecasting, anomaly detection,

and multivariate time series with complex patterns and

long-term dependencies

60.

CNNs for TimeSeries

Key insight: While RNNs process data sequentially, CNNs

detect patterns in parallel across different time windows,

making them computationally efficient for long sequences

while effectively capturing local temporal dependencies.

1D CNN architecture: Convolutional filters slide across time, extracting

features

1D Convolution Filter Example

Pattern Detector Trend Detector

0.2 0.5 0.3 -0.1 0.8 -

0.1

1

D Convolutions for Temporal

Pattern Extraction

What: Convolutional Neural Networks adapted for

sequential data using 1D convolutions rather than 2D (used

for images)

How: 1D convolutional filters slide across the time axis to

extract local patterns and features from temporal data

Why: Effectively capture local patterns in time series

without requiring recurrent connections

Advantages: More efficient than RNNs (parallel

processing), capture multi-scale temporal patterns,

fewer parameters

Implementation: Stacked 1D convolutional layers

followed by pooling layers and dense layers for

prediction

61.

Transformer Models forTime

Series

Self-Attention Revolution

"Transformers have revolutionized time series forecasting

by removing the sequential bottleneck of traditional RNNs

while enhancing the ability to model complex temporal

relationships."

Financial

Forecastin

g

Outperforms

LSTM in stock

Energy

Demand

State-of-the-art

results in

electricity load

forecasting

Healthcar

e

Improved

clinical time

series

predictions

Beyond Sequential Processing: Unlike RNNs/LSTMs,

transformers process all time steps simultaneously through

self- attention mechanisms

Self-Attention Mechanism: Captures relationships between

every time point and all other time points regardless of

distance

Positional Encoding: Preserves temporal order without

sequential processing constraints

Parallel Computation: Significantly faster training than

recurrent architectures

Long-Range Dependencies: Superior at capturing

long-term patterns in time series

Multi-Head Self-

Attention

Time Series Input + Positional

Encoding

Feed Forward

Network

Output

Projection

62.

Hybrid & EnsembleDeep Learning Models

Error Diversity: Different models make different errors,

improving overall robustness

Real-world applications often benefit most from hybrid

approaches. A CNN-LSTM model might extract local

patterns (CNN) and capture long-term dependencies

(LSTM), while adding attention mechanisms further

improves focus on relevant time points.

Ensemble model stacking architecture for time series

forecasting

Combining Models for Better Performance

Ensemble Methods: Combining multiple models to

improve accuracy and reduce variance in predictions

Model Stacking: Training a meta-model on the predictions

of base models, capturing different aspects of time series

patterns

Hybrid Architectures: Combining different neural network

types (CNN+LSTM, LSTM+Transformer) to leverage

strengths of each

Performance Benefits: Typically 10-15% improvement over

single models for complex time series

63.

Choosing Deep Learningfor Time Series

Consideration

When to Choose

Deep Learning

When to Avoid

Data Size

Large datasets

(10,000+

observations)

Small datasets

(few hundred

points)

Pattern

Complexit

y

Highly non-linear,

complex

relationships

Simple,

linear

relationship

s

Forecastin

g Horizon

Multi-step,

complex

predictions

Single-step,

simple forecasts

Interpretabil

ity Needs

Accuracy

prioritized over

explanation

Stakeholders

require model

transparency

Comput GPU/TPU Limited hardware,

Key Considerations

Data Volume: Deep learning typically requires large

datasets (thousands of observations) to perform well

Computational Resources: Training requires

significant computational power and memory

compared to statistical models

Non-linear Patterns: Best when complex non-linear

relationships exist that simpler models can't capture

Feature Engineering: Can automatically learn features,

reducing need for manual engineering

Interpretability: Trade-off between performance

and explainability; deep learning models are

"black boxes"

Deployment Complexity: More complex to deploy and

maintain in production environments

Deep learning is not always necessary for time series

64.

Practical LSTM ForecastingWalkthrough

Python

Implementation

import numpy as np

import pandas as pd

from sklearn.preprocessing import MinMaxScaler from

tensorflow.keras.models import Sequential

from tensorflow.keras.layers import LSTM, Dense, Dropout

# 1. Load and preprocess data

df = pd.read_csv('energy_consumption.csv') data =

df['consumption'].values.reshape(-1, 1)

# 2. Scale the data

scaler = MinMaxScaler(feature_range=(0, 1)) scaled_data

= scaler.fit_transform(data)

# 3. Create sequences

def create_sequences(data, seq_length): X, y = [],

[]

for i in range(len(data) - seq_length):

X.append(data[i:i+seq_length])

y.append(data[i+seq_length])

return np.array(X), np.array(y)

seq_length = 24 # 24 hours lookback

Implementation Steps

LSTM networks excel at learning long-term dependencies in time

series data. Below is a step-by-step process for implementing LSTM

forecasting:

Key insight: Proper data preprocessing (scaling,

sequencing) is critical for LSTM performance on time series

data.

Normalize your data (typically using

MinMaxScaler) Create sequences with

appropriate lookback periods

Structure data as 3D tensors (samples, time

steps, features)

Design LSTM architecture with appropriate layer

sizes Monitor training with validation data to

prevent overfitting Inverse transform predictions for

interpretable results

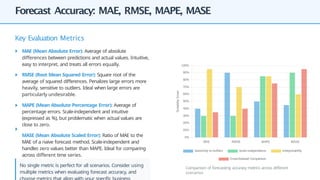

Forecast Accuracy: MAE,RMSE, MAPE, MASE

No single metric is perfect for all scenarios. Consider using

multiple metrics when evaluating forecast accuracy, and

Comparison of forecasting accuracy metrics across different

scenarios

Key Evaluation Metrics

MAE (Mean Absolute Error): Average of absolute

differences between predictions and actual values. Intuitive,

easy to interpret, and treats all errors equally.

RMSE (Root Mean Squared Error): Square root of the

average of squared differences. Penalizes large errors more

heavily, sensitive to outliers. Ideal when large errors are

particularly undesirable.

MAPE (Mean Absolute Percentage Error): Average of

percentage errors. Scale-independent and intuitive

(expressed as %), but problematic when actual values are

close to zero.

MASE (Mean Absolute Scaled Error): Ratio of MAE to the

MAE of a naive forecast method. Scale-independent and

handles zero values better than MAPE. Ideal for comparing

across different time series.

67.

Cross-Validation in Time

Series

KeyPrinciple: Always ensure that training data precedes

validation data chronologically to maintain realistic

forecasting conditions and prevent temporal leakage. Comparison of Walk-Forward (fixed window) vs. Expanding Window cross-

validation methods

Time-Aware Validation Approaches

Why traditional CV fails for time series: Random splitting

violates temporal dependence and introduces data leakage

Walk-Forward Validation: Train on fixed window, predict

one step ahead, slide window forward, repeat

Expanding Window: Start with initial training set,

progressively add observations while maintaining

temporal order

Rolling Origin: Multiple forecast origins to evaluate

model stability across different starting points

Nested Cross-Validation: Outer loop for model selection,

inner loop for hyperparameter tuning

68.

Model Selection andOverfitting Prevention

AIC BIC AICc

Training error decreases with model complexity while test error follows a U-

Choosing the Right Model

Information Criteria: AIC (Akaike Information Criterion) and

BIC (Bayesian Information Criterion) balance model fit and

complexity

Cross-Validation: Time series-specific methods like

expanding window and rolling validation prevent data

leakage

Parsimony Principle: Prefer simpler models when

performance is similar to avoid overfitting

Residual Analysis: Check for white noise residuals

with no remaining patterns

Regularization: Apply techniques like LASSO or Ridge to

penalize complex models

Remember: The goal is to find models that generalize

well to unseen data, not just fit historical patterns

perfectly.

69.

Interpreting and PresentingModel Results

Executive Dashboard Example

A retail demand forecasting model has predicted sales for the next

quarter. Here's how the results might be presented to executives:

Quarterly Sales Forecast

Dashboard

Seasonal Demand Pattern

Our model detected a 22% increase in demand for

Category A products starting in week 3 of Q2.

Action: Increase Category A inventory by 25% by May

15th.

From Analysis to Action

Even the most accurate time series models are only valuable when

their results can be translated into actionable business

recommendations. The final step in any analysis is effectively

communicating insights.

Business stakeholders care about outcomes, not

models. Focus on explaining what the forecasts mean rather

than how they were generated.

Translate technical metrics (MAPE, RMSE) into business

terms (% accuracy, dollar values)

Visualize forecasts with prediction intervals to

communicate uncertainty

Connect forecasts to specific business KPIs and

decisions Provide scenario analysis when possible

(best/worst case)

Offer specific, time-bound recommendations based

on predictions

70.

9

Section 9: Real-

World

Application

s

Fromtheory to

practice

Exploring how time series analysis

techniques are applied across various

industries to solve real business problems

and drive data-informed decision making.

Made with Genspark

Time Series Analysis: Complete Guide from Statistics to Deep

Learning

71.

Finance & StockMarket Forecasting

ARIMA for Stock Price Forecasting

This example demonstrates using ARIMA to forecast stock prices for

a 10- day horizon:

import pandas as pd

import numpy as np

from statsmodels.tsa.arima.model import ARIMA import

matplotlib.pyplot as plt

# Load historical stock data

df = pd.read_csv('tech_stock.csv') df['Date'] =

pd.to_datetime(df['Date']) df = df.set_index('Date')

# Fit ARIMA model (order=3,1,2)

model = ARIMA(df['Close'], order=(3,1,2)) results =

model.fit()

# Generate forecast

forecast = results.forecast(steps=10) forecast_index =

pd.date_range( start=df.index[-1] + pd.Timedelta('1

day'), periods=10, freq='B')

forecast_series = pd.Series(forecast,

index=forecast_index)

Time Series in Financial Markets

Financial markets generate vast amounts of time-ordered data that

make them ideal candidates for time series analysis. Stock prices,

exchange rates, and trading volumes all follow temporal patterns

that can be modeled and forecasted.

Financial time series often exhibit unique

characteristics like volatility clustering and leverage effects

that require specialized models.

Market Efficiency: Markets react quickly to new

information, making prediction challenging but possible in

certain timeframes

Volatility Modeling: GARCH models capture changing

variance in financial returns

Technical Analysis: Using historical price patterns to

predict future movements

Risk Management: Value-at-Risk (VaR) calculations rely on

time series forecasting

Algorithmic Trading: Automated strategies often use

time series signals

72.

Economics and MacroeconomicForecasting

Practical Example: GDP Forecasting

Using ARIMA to forecast quarterly GDP growth and inform

policy decisions:

import pandas as pd

import statsmodels.api as sm

# Load quarterly GDP data

gdp_data = pd.read_csv('quarterly_gdp.csv', parse_dates= ['date'])

gdp_data = gdp_data.set_index('date')

# Fit SARIMA model (accounts for seasonality in economic data)

model = sm.tsa.SARIMAX(gdp_data['gdp_growth'],

order=(2,1,2), # ARIMA parameters

seasonal_order=(1,1,1,4)) # Seasonal component results =

model.fit()

# Generate forecast for next 8 quarters (2 years) forecast =

results.get_forecast(steps=8) conf_int = forecast.conf_int()

Macroeconomic Time Series & Policy

Macroeconomic forecasting uses time series models to predict

future values of key economic indicators, providing critical

information for central banks, governments, and businesses to make

informed decisions.

Time series forecasts directly influence monetary policy,

fiscal planning, and regulatory frameworks that affect

entire economies.

GDP growth prediction influences government spending and

taxation policies

Inflation forecasting guides central bank interest rate

decisions

Unemployment rate projections impact labor market

policies Foreign exchange predictions affect international

trade strategies

Consumer confidence index forecasts influence retail

sector planning

73.

Business Operations &Demand Forecasting

Retail Inventory Optimization

A national retailer implemented time series forecasting to

optimize inventory across 500 stores:

import pandas as pd

from statsmodels.tsa.holtwinters import

ExponentialSmoothing

# Load historical sales data

sales_data = pd.read_csv('store_sales.csv') sales_data['Date'] =

pd.to_datetime(sales_data['Date']) sales_data =

sales_data.set_index('Date')

sales_data = sales_data.asfreq('D')

# Apply Holt-Winters method with weekly seasonality model =

ExponentialSmoothing(

sales_data['Units'],

seasonal='multiplicative',

seasonal_periods=7

).fit()

# Generate 30-day forecast forecast

= model.forecast(30)

Critical for Business Success

Demand forecasting is the process of predicting future customer

demand for products or services, enabling businesses to make

informed decisions about inventory management, staffing, and

resource allocation.

Companies that effectively implement demand forecasting

can reduce costs by 10-20% while improving customer

satisfaction through optimal inventory levels.

Enables optimal inventory levels, reducing carrying costs and

stockouts Supports efficient staffing and resource planning

Improves cash flow management and financial planning

Enhances supplier relationships through consistent ordering

patterns

Supports strategic decision-making for product

development and marketing

Common forecasting methods include time series approaches

(ARIMA, exponential smoothing), machine learning models, and

causal models that incorporate external factors like promotions,

74.

Healthcare and LifeSciences Applications

ECG Anomaly Detection Example

ECG monitoring generates time series data that can be analyzed to

detect abnormal heart rhythms. Below is an approach using LSTM

networks:

import pandas as pd

import numpy as np